Izabella Kaminska 11:58

Izabella Kaminska 11:58

Greetings all …

(Just waiting for some rabble to show up.)

Hello and welcome to Spot Markets Live.

The whirlwind tour of the markets.

Maybe we should have a picture for the day?

Up 5.6 per cent today on the back of higher quarterly sales. From The Times:

Greggs, the high street bakery chain, has reported a robust third quarter as its sausage rolls, sandwiches, vegan snacks and sweet treats continued to attract cost-conscious customers.

Like-for-like sales at the company, considered a bellwether for the health of the retail sector, rose 9.7 per cent in the three months to October 1 compared with the same period last year. Sales were strong in July, slowed in August compared with last year when it was boosted by the rise in staycations, but momentum returned last month.

We were anticipating a bit of a crazy week this week, but actually, it’s not been too bad. But we’re sticking to our three sessions this week because there’s still plenty of news flow.

And we’re lucky to be joined today by a man who knows his OIS from his eurodollar 3-month rates, and can easily differentiate the F from the I in the FICC.

Hello Mr. Helmholtz

Helmholtz 12:03

Helmholtz 12:03Good morning and thank you for inviting me to chat with you

Izabella Kaminska 12:03Maybe give the readers as much background about yourself as you’re comfortable with?

Helmholtz 12:03Yes, of course.

I’ve been in the markets for nearly forty years, working in London, New York & Tokyo

Until 2008 I was on the sell side running rates desks and Treasury for various IBs.

Since then I’ve been on the buy side looking at the opportunities post-GFC, had various expert witness projects related to issues arising from the crisis, and been working with industry bodies to improve standards and market functioning.

Izabella Kaminska 12:04I can vouch for this. But more importantly, do you like a Greggs bake in the morning?

Or are you more of a Pret-a-manger man?

Helmholtz 12:05Greggs please – the sausage roll is a staple…

Izabella Kaminska12:05Lovely. I would like for the Greggs sausage roll to become the go-to alternative inflation/interest rate indicator for markets, please…

Could that work?

Helmholtz 12:06Yes – the UK equivalent to the Big Mac index.

Izabella Kaminska 12:06Exactly

Before we get to your area of expertise, Mr. H, just a quick wrap of the markets.

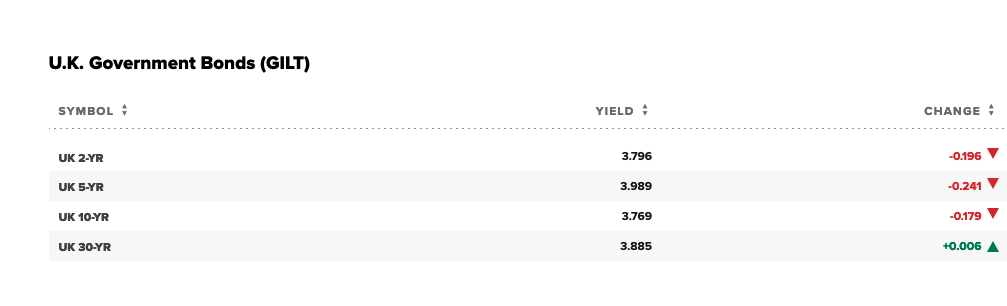

US Bond yields were down overnight/ today but markets seem pretty bullish. Europe is up in the 1.5-2% range overall.

(about 30 mins stale)

Bitcoin is also having a good day and was finally back over $20,000 (but is back below again)

It follows a rebound on wall street at the start of the new quarter.

But what everyone wants to know is how big a deal is what’s going on in rates markets?

Rabble – this is your moment to get your questions in for Helmholtz.

Helmholtz 12:08The move up in reference rates globally is a big deal – it’s the first real repricing of short-end risk that we have seen in over a decade; actually almost fifteen years now.

Izabella Kaminska 12:08is this important?

Helmholtz 12:08Yes, I think it is.

For several reasons:

1) the turmoil it’s caused in bond markets generally – with the LDI sell-off last week being an extreme example (although I note that there are stories appearing about issues with pension funds in the USA now as well).

2) the potential for related issues to develop – I’m particularly thinking about mortgages and the pressure on housing markets.

Izabella Kaminska 12:09I want to ask you more about what we should be looking at to help evaluate true stress in the liquidity markets. But before that, let’s revisit the LDI story with more detail…

I’ve seen two main evaluations of what’s gone on.

1) that we knew this was coming, and the powers did too, but failed to act properly.

2) that we knew this was coming and by and large it was dealt with ok?

Which do you side with, or is there a third option?

Helmholtz 12:10LDI was created as a solution to the mismatch between assets and liabilities in DB pension schemes.

Or more specifically, the duration mismatch between assets and liabilities.

The issues have always been known:

1. Convexity – using a leveraged LDI instrument always meant that the convexity of the asset pool in a pension scheme is much greater than the convexity of the liabilities.

And this is far more acute for index-linked exposure.

Note the huge moves in real yields (both in UK and US)

2. The ability to liquidate assets to meet margin calls is severely constrained when markets fall

But it’s not a solvency issue – at least for the underlying asset.

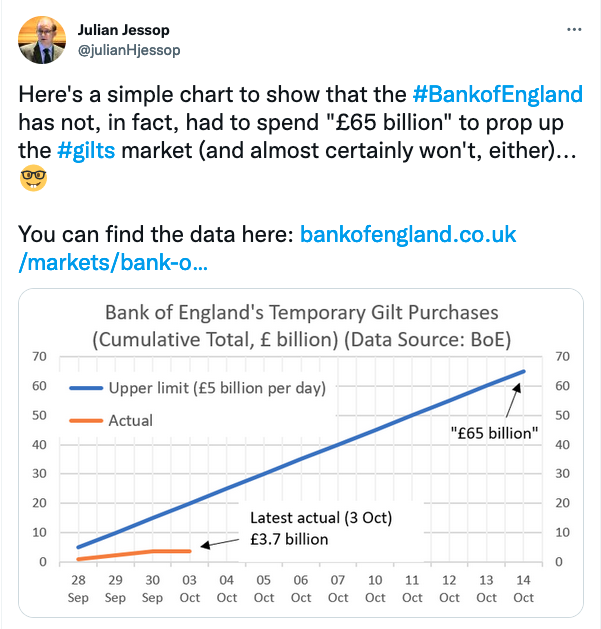

The integrity of the underlying assets were never in question, it was the failure in the market mechanism – in this case, the collateral calls against LDI structures – that was the problem, and I think the BoE may have solved the issue:

The latest temporary gilt purchases are on this link

The temporary purchases run out at the end of next week, but hopefully, the redistribution and rebalancing of risk will have taken place by then.

There is talk about reduced leverage in DB schemes but part of this must be from the move in rates – the leverage in LDI instruments will automatically reduce as rates rise.

And it makes sense for DB schemes to derisk at higher rate levels.

So I’m not convinced reports of deleveraging are anything more than normal behaviour at the higher rate levels.

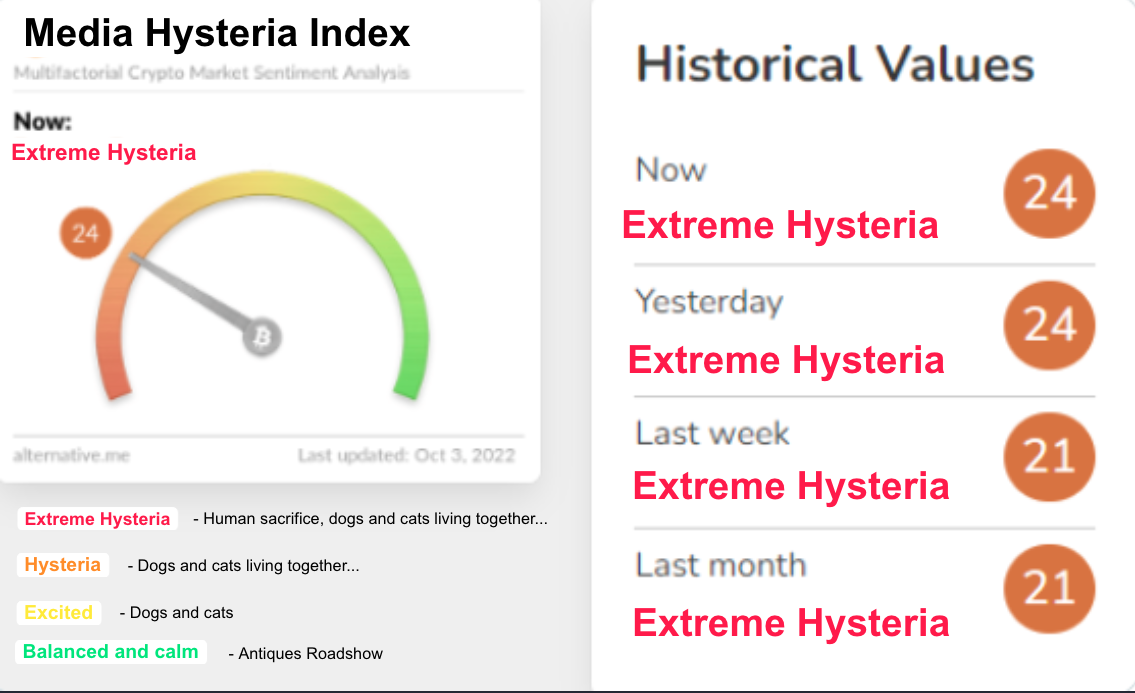

Izabella Kaminska 12:13

This seems like an important and missed point.

A good op to bring out my media hysteria meter.

Helmholtz 12:14

Helmholtz 12:14RF – yes those are numbers I have seen too. That was the problem – too many sellers trying to get through a shrinking door

The purchase of long-dated gilts by the BoE in response to the LDI problems is, I think, best described as an OMO

To provide enough liquidity to allow rebalancing and transfer of risk

Which is why the outright purchases are so small

Izabella Kaminska 12:16Albert Edwards made a point that really it wasn’t the underfunded bit of the budget that spooked the market but something else, do you agree?

Helmholtz 12:16Yes, that worry about the public finances gave the market the final push, but this was totally mechanistic and already a danger due to the construction of LDI.

Really a liquidity problem.

Izabella Kaminska 12:18You mentioned mortgages. So how does this whole repricing of mortgages work from a rates trading perspective?

We hear a lot about convexity. You’ve already mentioned it in fact. People will recall this term maybe from the bad old days of subprime, but I’m curious to know how it impacts us now and what we as market observers should be looking out for here?

Helmholtz 12:18Mortgages have higher convexity than similar maturity nominal coupon bonds primarily because of the optionality that the mortgagee has to refinance, but also because there is a solvency issue if the underlying property declines in value.

So in some ways a similar problem to LDI.

Izabella Kaminska 12:19@colin – that is the sort of market insight you just won’t get anywhere else 🙂

Helmholtz 12:19But TBH I am more concerned with the issue for mortgages of higher rates – so much of the economy (here and elsewhere) is related to property

Izabella Kaminska 12:20exactly. What do you think happens then if people can’t adjust in time. Also, aren’t the early redemptions an issue?

Because seems like so many of the packages my mates are on are geared around making sure whatever they do they don’t move out of fixed deals earlier than contracted to.

Helmholtz 12:21That’s true. But those deals eventually roll off and then the pain starts.

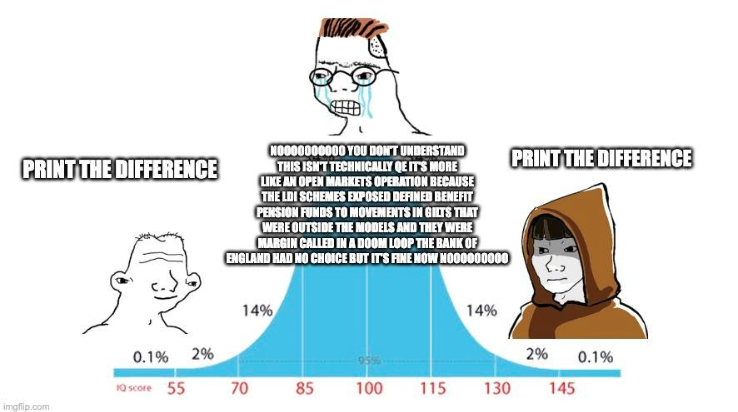

Izabella Kaminska 12:22Speaking of OMOs, I love that my bitcoin readers see it this way.

It’s an evolution of the midwit meme, which suggests the mainstream tends to overcomplicate stuff for the sake of pretending to look smart, and that actually the people who know what’s really going on are on the extremes of the IQ spectrum.

I did find it funny.

Is it money printing or not?

I’m being framed as the midwit here. Oh sigh.

Helmholtz 12:24@McC – yes, very true.

Izabella Kaminska 12:24Speaking of LDI, the FT had this story out overnight:

Three UK asset managers have said they are unable to handle heavy demand from investors seeking to withdraw from property funds, in a sign of how the fall in government bond prices is forcing pension funds to reallocate holdings. Schroders said it will make some redemptions originally due on Monday as late as July next year, while Columbia Threadneedle said volatile market conditions had forced it to switch from daily to monthly payouts. At the same time, BlackRock also imposed new restrictions on withdrawals.

How big a deal is this? I think a key discussion point yesterday was that in a banking resolution environment the pain is increasingly shifted to the asset managers. So, what are the risks we may or may not be seeing here?

Helmholtz 12:26I think that’s true – the risk has moved to the AMs. But inevitably that will be moved on to the investors.

As part of my market structure work, I was looking at what funds could do with sanctioned assets.

And here the problem is related.

Izabella Kaminska 12:27That’s an interesting connection actually. Had not thought of it in that way.

Helmholtz 12:28I think funds will increasingly have to contemplate suspensions/side pockets.

Izabella Kaminska 12:28But interestingly, a lot of people (bitcoiners and libertarians) bring up Cyprus as an example of how this is illustrative of a collapse of capitalism.

Helmholtz 12:28Yes – someone earlier made the connection between liquidity and the Gobi desert – so true

Thank you FC

Izabella Kaminska 12:30I’m interested in the relation to sanctions though, can you expand?

Helmholtz 12:30Yes I can

The FCA issued a consultation paper earlier this year to do with the issues that funds faced if they held Russian assets.

How should they handle those assets – particularly as they might breach sanctions regulations by trading them.

Izabella Kaminska 12:32I am presuming it’s this?

Helmholtz 12:32There is no perfect solution, but anything that prevents – or ameliorates – the bank run scenario must be of value.

Yes, that’s it.

Izabella Kaminska 12:32Side-pockets!

That’s a new term for me.

But feeds into segregated assets etc.

Here’s a short chunk from the consultation:

This Chapter sets out proposed new rules and guidance in Chapter 7 of our Collective

Investment Schemes sourcebook (COLL) for UK authorised retail funds that have

exposure to Russian, Belarusian and Ukrainian assets, permitting them to establish

‘side pockets’. Side pockets would enable a fund to issue separate units with exposure to those assets that cannot be traded because of sanctions, or are difficult to sell or hard to value, alongside units relating to the fund’s other liquid investments.

Side pockets are commonly used in non-retail funds, such as hedge funds or

institutional funds, either as a routine way of dealing with certain illiquid assets (e.g.

distressed debt securities) or in response to unforeseen circumstances. However, they are not normally available to retail funds, which are meant to hold liquid assets so that they can offer redemption on demand.

We propose that managers of UK authorised retail funds with exposure to affected

investments use their discretion to determine whether it is in unitholders’ best

interests to create a new class of unit relating only to the affected investments,

distinct from other classes of unit relating to all the unaffected liquid assets.

@frances this ironically feels a lot like the resolution structures the crypto world is coming up with quite organically too, don’t you think?

Anyway it’s a good op to segue to Credit Suisse

The stock was up about 5% last I looked

And I think this whole issue of side-pockets applies to the controlled implosion of banks in general. Right?

In the case of Credit Suisse, it’s going to essentially be guided into some sort of state-supported hybrid? And the real pain will be felt by those whose jobs are probably on the line now?

What’s your feeling on how markets ran with that story and what are we missing?

Helmholtz 12:37At these levels in CDS, both CS and DB, will be struggling with margin calls on collateralised exposure (more required as their credit deteriorates);

Izabella Kaminska 12:37Right. So it’s not a nothing burger. It’s just not 2008.

Helmholtz 12:37This is not necessarily terminal for either as they both have substantial liquidity buffers and I’m sure the relevant CBs are ready with the hose.

yes – not 2008, but probably terminal for the IB.

Izabella Kaminska 12:38Yeah, and I get the impression a lot of the employees are maybe looking around on Linkedin right now.

Helmholtz 12:39yes indeed; as FC says, it’ll probably be an orderly resolution, but not a going concern.

Izabella Kaminska 12:39The issue for them is their own deferred equity options.

It’s an amazingly complex situation I guess. You either jump and forgo your lifelong accumulations (especially if you’re a bit of a lifer at the org) — but get ahead of the curve on the jobs front. Or you wait it out till the bitter end.

Either way, you are basically screwed.

Helmholtz 12:41Yes – and sympathy for bankers is not widespread…

FC – yes, that’s my thought as well, but it’ll be to protect the domestic franchise

So RBS redux?

Izabella Kaminska 12:42What was the compensation norm there?

Helmholtz 12:42As I remember, RBS paid in cash so their employees were (comparatively) OK.

Izabella Kaminska 12:43Ah… Interesting.

But also has a downside, because those deferred options tend to stop employees from scarpering at the first sign of distress.

I remember a point in the 2008 madness, where a lot of the people I knew at Morgan Stanley and Goldman were intent on staying put until the last moment because of it.

@frances – but how does that not equate to a type of bail-in via employee?

Even if severance is honoured, if the pay packets are vapourised? They’re the ones holding the bag, as the crypto people would say.

Helmholtz 12:45GH – so true – long term very bad for economic growth.

Izabella Kaminska 12:46Robert – good question, and I plan to look at that. I’m interested in the mechanics of who dictates that a CoCo conversion event has occurred. It’s the BoE, right?

Or other respective central banks?

Helmholtz 12:46I think it’s very complex and different bonds have different provisions.

Izabella Kaminska 12:47Oh gawd. So we can’t assume anything then?

Sounds like a market opportunity for some sort of conversion monitoring site.

If I wasn’t already launching 1000 ships…

Helmholtz 12:48Bruce – sorry I don’t know.

Izabella Kaminska 12:49I think this is a good time to pivot… we’ve got 10 mins left. What does the rabble want to ask about? I’m personally quite interested in linkers.

Mainly because they make my head hurt.

But I’m hearing all over the place that now is finally a good time to go into them.

Would you agree?

Helmholtz 12:50IL bonds – positive real yields last week were (in 20/20 hindsight)) a superb purchase

particularly for individuals in the UK (no tax !!)

Izabella Kaminska 12:50Oh yeah, good point

(That and horse trading)

Helmholtz 12:51I’m not so sure about right now in UK, but US linkers are now +ve I believe

Izabella Kaminska 12:51On linkers, I think even for the average retail investor, they make a lot more sense now if you are happy to buy and hold.

Obviously not suitable for everyone. This is not investment advice, yadda yadda.

Helmholtz 12:53Robert – I’m not sure. Clearly, knock-ons apply, but each country has its own challenges.

Izabella Kaminska 12:53@peter it really is like the trenches

Yikes

Speaking of international linkages, there’s one man who has a very clear view of what’s going to happen next.

Have you seen Roubini’s latest?

He is not called Dr. Doom for nothing.

NEW YORK (Project Syndicate)—For a year now, I have argued that the increase in inflation would be persistent, that its causes include not only bad policies but also negative supply shocks, and that central banks’ attempt to fight it would cause a hard economic landing. When the recession comes, I warned, it will be severe and protracted, with widespread financial distress and debt crises. Notwithstanding their hawkish talk, central bankers, caught in a debt trap, may still wimp out and settle for above-target inflation. Any portfolio of risky equities and less risky fixed-income bonds will lose money on the bonds, owing to higher inflation and inflation expectations.

I’ll skip to the key points…

And the broader sanctions regime—not least the weaponization of the dollar BUXX, -0.60% DXY, -0.38% and other currencies—has further balkanized the global economy, with “friend-shoring” and trade and immigration restrictions accelerating the trend toward deglobalization. Everyone now recognizes that these persistent negative supply shocks have contributed to inflation, and the European Central Bank, the Bank of England, and the Federal Reserve have begun to acknowledge that a soft landing will be exceedingly difficult to pull off. Fed Chair Jerome Powell now speaks of a “softish landing” with at least “some pain.” Meanwhile, a hard-landing scenario is becoming the consensus among market analysts, economists, and investors.

It is much harder to achieve a soft landing under conditions of stagflationary negative supply shocks than it is when the economy is overheating because of excessive demand. Since World War II, there has never been a case where the Fed achieved a soft landing with inflation above 5% (it is currently above 8%) and unemployment below 5% (it is currently 3.7%). And if a hard landing is the baseline for the United States, it is even more likely in Europe, owing to the Russian energy shock, China’s slowdown, and the ECB falling even further behind the curve relative to the Fed. The recession will be severe and protracted.

Are we already in a recession? Not yet, but the U.S. did report negative growth in the first half of the year, and most forward-looking indicators of economic activity in advanced economies point to a sharp slowdown that will grow even worse with monetary-policy tightening. A hard landing by year’s end should be regarded as the baseline scenario….

I don’t necessarily disagree.

But, an interesting tidbit about Roubini is that he’s now the chief economist of this thing:

Yeah, so no prizes for guessing their worldview on things.

Looks like a stablecoin crossed with an apocalypse-mandated investment manager preparing to benefit from monetary chaos.

But details are light

I love the punchy marketing

WHY NOW?

The current socioeconomic environment is characterized by an unprecedented proliferation of risks.

We believe these risks threaten to undermine the foundations of stability in the United States of America and around the world.

OUR APPROACH

We are not your typical Investment Manager.

MISSION

Our mission is to mitigate the impacts of ensuing risks by supporting the development of climate resilient communities across North America, while also insulating against inflation and the potential decline in the real value of the US dollar.

Helmholtz 12:57Who is John Galt? I hear Colorado is nice this time of year.

Izabella Kaminska 12:57Exactly

Helmholtz 12:58Carlo – I think that’s the Tory conference in one

Izabella Kaminska 12:58I mean, can you actually profiteer from the apocalypse?

Not sure.

Helmholtz 12:59Linkers – not investment advice but yes, I’m inclined towards that in the low productivity environment.

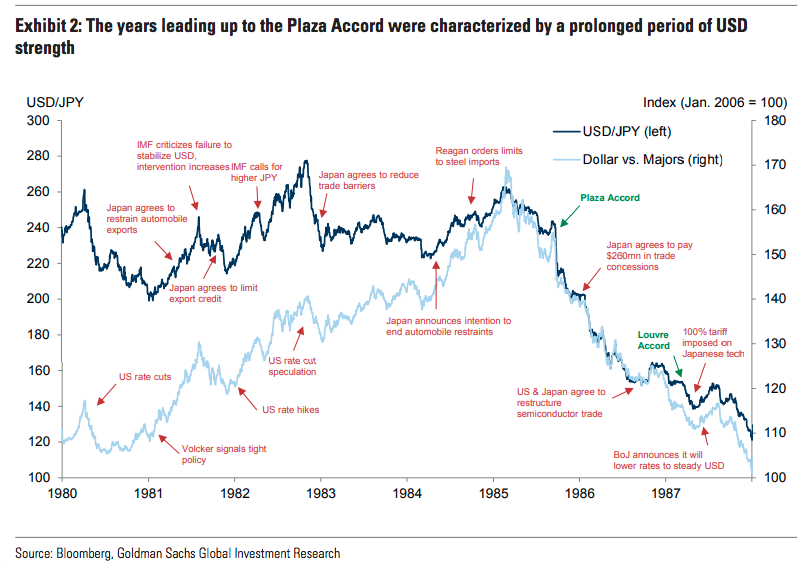

Izabella Kaminska 12:59I think that’s a good op to finish off with a reference to the Plaza Accord…

Basically back in play, all over the news.

Here’s a nice contextual chart from Goldman

Can the cbanks collaborate to that degree again?

Helmholtz 13:00And that bookends my career – my first job was on an FX desk in Feb 1985….

1.0360 was the low

FC – who knows?

Izabella Kaminska 13:01There you go. Rumours of the Plaza Accord’s return are greatly exaggerated.

You heard it here first.

I think that’s a wrap for today. Quite banking and rates intensive, but worth it given the news flow. Tomorrow we will be back again with Ben Harrington, of Betaville, for more corporate-themed coverage. And hopefully, we will have Helmholtz back again with us soon too. Hope the rabble weren’t too unruly for you 🙂

Helmholtz 13:03They are a gentle audience – thank you!

Izabella Kaminska 13:03And very well informed.

So thank you all for joining us, you make these sessions worthwhile and we all benefit from each other’s expertise.

It’s bye from me, I’m on my way to Birmingham now. Wish me luck.

Ciao…

One Response

Here we are told that there is discretion re: margin calls (bilateral?)

https://www.risk.net/derivatives/7954682/uk-pensions-hit-with-ps100m-margin-calls-as-gilts-and-sterling-slide

..but that centrally cleared might be less generous.

Given that some of the LDI runners.. https://group.legalandgeneral.com/en/newsroom/press-releases/legal-general-continued-positive-momentum-and-a-robust-balance-sheet-despite-market-volatility

..also run pension funds n such, how would one know that what went on was not a competitive strategy or one to benefit the other side of any trades?

Is it also not strange that those risk takers lobbying for lower taxes and larger GnTs are apparently unable to do so?

Finally as you mention above there are other markets that you have been tracking where liquidity has been seen to be lacking, energy, and crypto.

Are there lessons in the differences and or similarities in the causes, problems and solutions in each?