FRANCES COPPOLA10:58

FRANCES COPPOLA10:58..

11:00Hi everyone, welcome back. This is my first solo flight. Hope we don’t have a crash landing.

And no, I wasn’t up at dawn today!

Speaking of crash landings….

11:02ugh I was trying to post a meme pic but it didn’t work. Anyway. Let’s kick off with the fallout from UBS/CS.

There was a bit of a rout in bank stocks yesterday, but they seem to have recovered. AT1s of course underwent a vicious repricing as investors woke up to the fact that they might actually be wiped.

The AT1 problem caused a lot of consternation which basically boiled down to “we shouldn’t have been wiped because look shareholders weren’t”.

11:05There’s been a lot of chatter on twitter about whether the terms of CS AT1s allowed them to be treated as junior to equity, and whether this was unique to CS. The answer seems to be – sort of but the terms were ambiguous. Apparently it needed a new law to permit AT1s but not shareholders to be wiped.

11:07I suspect they thought it was easier to wipe AT1s, which are designed to be zeroed (even if not under these specific circumstances), than equity which arguably shouldn’t be zeroed in a going concern situation. In the 2008 bailouts, equity often wasn’t wiped.

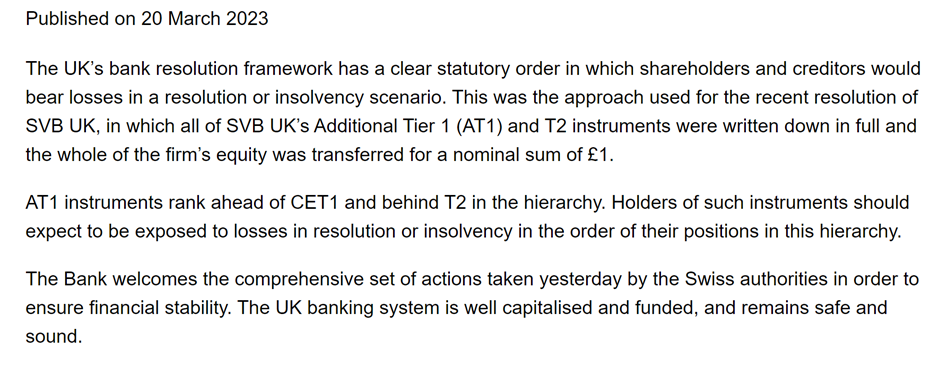

Anyway, wiping AT1s but not shareholders not only upset investors, it annoyed other regulators. The European regulators stuck the boot in:

And the Bank of England polished its halo – the holier-than-thou tone of their statement is quite something

So it seems AT1s elsewhere in Europe will now definitely be senior to equity in any future resolutions.

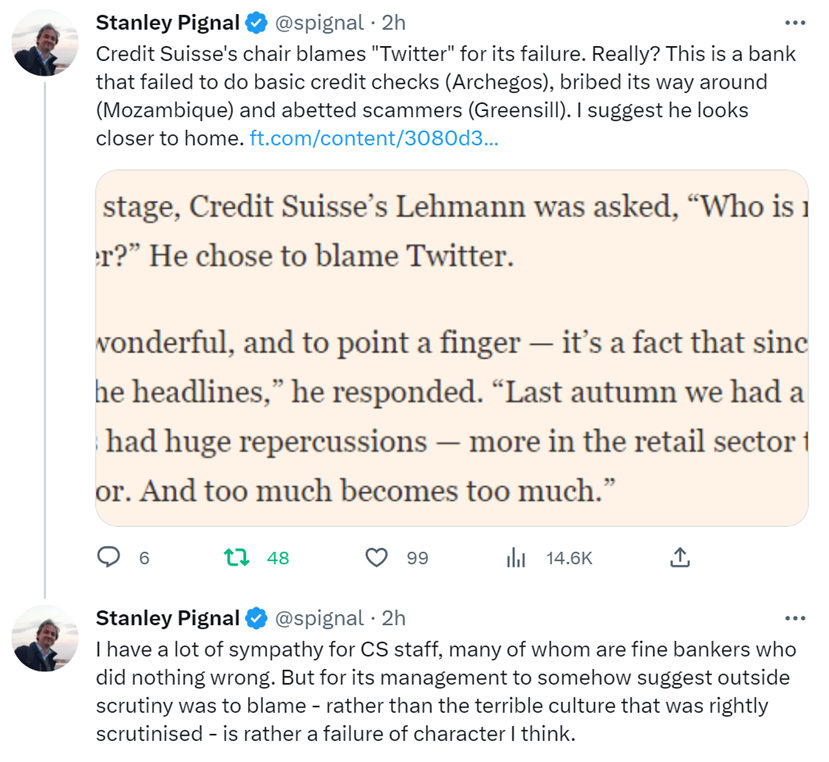

11:12Meanwhile, Axel Lehmann is trying to argue that CS’s failure was down to Twitter, because the bank run that crippled it in October was started by someone on twitter saying a GSIB was on the brink of failure.

The Brussels bureau chief of The Economist is nonplussed

11:14But there were a lot of components to CS’s failure, of which Twitter was only one. All the things that Stanley Pignal mentions, plus the SEC’s demand that it restate some of its accounts, and then the “unfortunate comments” from the Saudi National Bank, which as Izzy says, feels very set up.

11:15The final straw for me was the revelation that CS’s core Swiss bank was probably worth more as an asset than it was embedded in the CS empire. That’s an overwhelming argument for breakup and I would have thought that had there not been a potentially fatal bank run, the shareholders would have forced a breakup anyway.

11:17Twitter contributed not only to CS’s fall, but also to SVB’s. In SVB’s case there were active influencers encouraging a bank run. To what extent does Twitter’s ability to amplify bad news and create widespread panic threaten the stability of the financial system?

Izabella Kaminska11:18

Izabella Kaminska11:18There will be policy implications!

FRANCES COPPOLA11:18In theory any bank could be brought down by a prominent influencer spreading panic on twitter.

All banks have skeletons in their closets.

Izabella Kaminska11:18Indeed, and there was already talk on the Dem side about trying to censor this sort of speech on Twitter. And frankly, on this one point, I kind of agree about restrictions.

It’s like when Robert Peston accelerated the panic about Northern Rock

FRANCES COPPOLA11:19And there’s also the “FRACTIONAL RESERVE BANKS ARE INSOLVENT” crowd who pop up whenever there’s a banking crisis and are currently making waves on Twitter yet again.

Izabella Kaminska11:20And Balaji offering to buy a bitcoin for $1m

FRANCES COPPOLA11:20Yes it’s just like that Izzy – in fact I wrote about that the other day. The worst thing any bank exec can say is “our capital and liquidity are strong” lol

Izabella Kaminska11:20100%

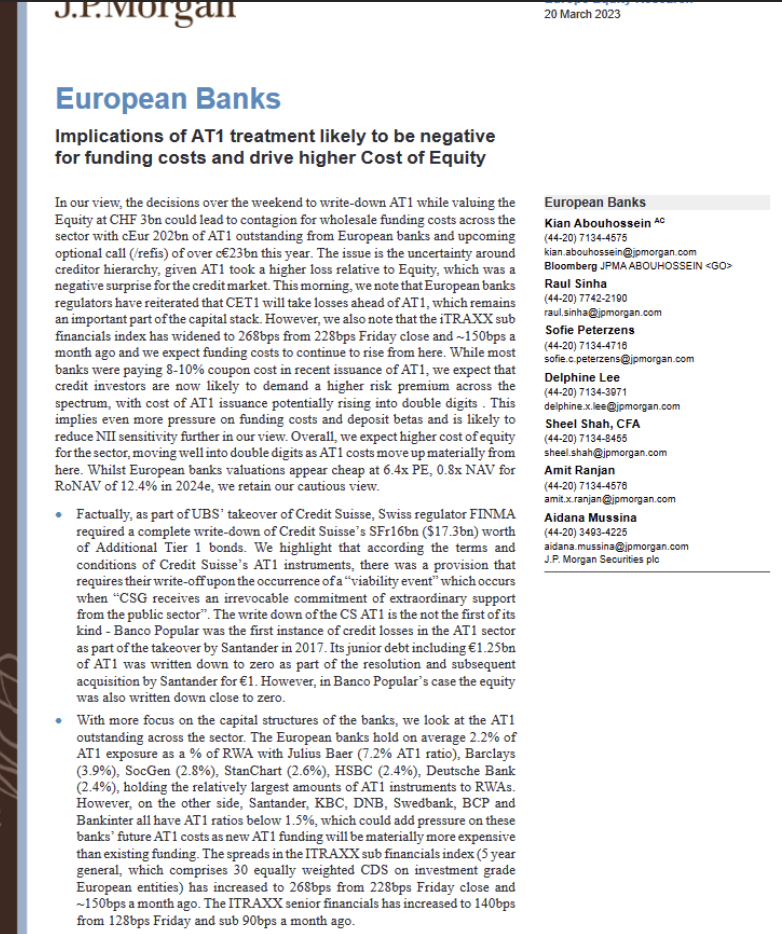

Btw in case of use here’s the JPM report on AT1

FRANCES COPPOLA11:22

FRANCES COPPOLA11:22Yes that’s what I was trying to say yesterday. Capital just got a whole lot more expensive for banks. That will feed through to higher costs for borrowers.

Izabella Kaminska11:22How will that play out with rate hiking ?

FRANCES COPPOLA11:22It implies a slower pace or even a pause.

Danny Blanchflower, ever the outlier, is calling for the Bank of England to cut rates.

Izabella Kaminska11:23Elon Musk is also calling for rate cuts

FRANCES COPPOLA11:23He’s got loads of floating rate debt, Izzy

11:24https://twitter.com/elonmusk/status/1637971685751025666

FRANCES COPPOLA11:24

FRANCES COPPOLA11:24I think the central banks will try to bluster their way through though. They’ll raise rates to prove they aren’t blown off course by a banking wobble.

And then have to cut them when they realise that they’ve over-tightened because they didn’t take account of passive tightening by nervous banks.

We’ve played this scene before, though not for a long time.

I still recall that the day after Lehman the Fed was discussing raising rates because of inflation fears.

11:28Inevitably now there are calls for tighter regulation of banks too. Or even complete redesign of the banking system. Martin Wolf in the FT wants CBDCs and a fully automated luxury payments system that completely disintermediates banks.

11:29Meanwhile in the US, there are more wobbly banks. First Republic Bank’s stock price crashed by 47% yesterday after S&P downgraded it. It was already junk, but it’s now even more so.

It has a large proportion of uninsured deposits, which have been running like a tap since SVB failed. It borrowed $30bn it borrowed from Wall Street banks, but it seems this isn’t enough to restore confidence. I’m not convinced that lifting the FDIC limit would solve its problems either. It needs more capital – or a fast resolution by FDIC.

11:31FRB isn’t the only one. Deposits have been running from mid-size US banks into the biggest banks, which are viewed as too-big-to-fail and therefore at no risk of a deposit haircut. Hmm. As Bank of Cyprus depositors know to their cost, haircuts can be a means of preventing the bank from failing. They suffered a 47% haircut as part of the bank’s bailout in 2013.

Anyway, there are now calls for the FDIC insurance limit to be raised to stop the bleeding. A consortium of mid-size banks wants the limit lifted for two years, paid for by an increase in the deposit insurance levy.

These are the very same banks that lobbied hard not to be subjected to the intensive regulation and supervision required of banks deemed “systemically important”. The 2019 reforms to Dodd-Frank downgraded the level of supervision. Personally I would suggest a temporary lifting of the FDIC limit should be accompanied by permanently tighter regulation and more supervision. Banks that require unlimited guarantees are systemically important.

Martin Wolf thinks so too

The US Treasury is said to be studying ways of temporarily lifting the FDIC insurance limit without involving Congress.

Republicans, of course:

I do like a good battle between Congress and the US Treasury. Mind you, we have the debt limit coming up…

11:37The problem with lifting the FDIC limit every time the banking system throws a tantrum is that it destroys the credibility of the limit. Some people want the FDIC limit lifted permanently, because it isn’t high enough to protect things like working capital for businesses. And it’s not just an issue for thhe US. When SVB UK failed, lots of UK tech companies worried about being unable to make payroll.

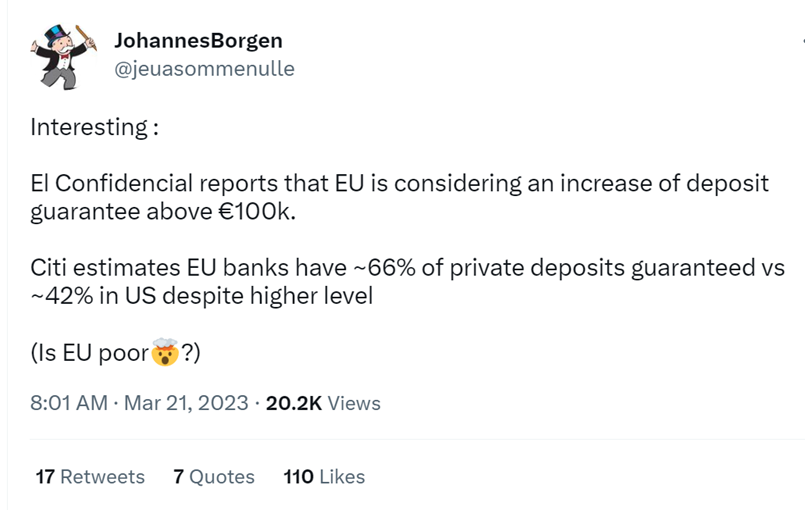

11:38So the ECB is apparently also considering raising the insurance limit.

Cypriot depositors will be spitting blood if they raise that limit. As will Irish taxpayer.

11:41On capital regulation – yes, Bruce, tier 1 is not all it is cracked up to be. The problem is that lots of the securities banks hold are zero-weighted. Silvergate had a CET1 ratio in excess of 50% when it failed, because it was losing money hand over fist through having to crystallise losses on HTM securities that were zero risk weighted.

Izabella Kaminska11:41This is all a big mess.

FRANCES COPPOLA11:42The leverage ratio is more useful, but even that can be gamed by banks classing securities as held-to-maturity. SVB and Silvergate both moved securities from available for sale to held to maturity to avoid having to take MTM losses through other comprehensive income. But of course in a bank run they have to sell or pledge securities, and they can only raise the market value of the bond, not the book value.

Izabella Kaminska11:43@bruce – that’s exactly right. And this is the fundamental issue about banks. Banking as a sector is not a going concern in the current regulatory climate. Echoes of what Anat Admati always said, about how banks only care about their return on equity.

FRANCES COPPOLA11:43I think the accounting standards regarding held-to-maturity securities need to be looked at again, and regulation around what qualifies as held-to-maturity needs to be tightened.

@bruce yes NIM is still too thin. Implies continuing financial repression for both depositors and borrowers.

And Anat Admati was right. Banks need much larger capital buffers. Also the risk weighting regime needs to be looked at again.

11:46The liquidity and capital regulation we have now was designed for the post-GFC environment. It’s not fit for purpose in a higher interest rate, tighter money environment (imho).

@Bruce, Izzy mentioned on Friday that the DMO was shortening the duration of new issue gilts.

11:48So thinking about risk weighting; Per Kurowski has argued for years (probably over a decade now) that weighting government securities at zero is mispricing risk. This was also the Eurozone crisis problem: government debt that should have been safe turned out not to be.

Once again, we have failure of safe assets – this time, falling market value on securities needed as collateral to raise cash to honour par deposit withdrawals.

@Graham no bank will hedge interest rate risk on held-to-maturity portfolios. Imho it is the qualification of held-to-maturity that needs to be looked at.

11:52In effect banks have used HTM securities as a kind of insurance for uninsured deposits. Hence the calls to lift the deposit insurance limit.

So, should the deposit insurance limit be lifted? What would the consequences of doing so be?

this was the meme pic I tried to post at the start!

the lesson from Cyprus and Ireland was that unlimited deposit insurance is eventually borne by the whole economy

in Cyprus even limited insurance was too much for the economy to bear – it went into a deep recession

11:57On the other hand, widespread losses for depositors can also crash the economy. It’s a difficult balance, I think.

Izabella Kaminska11:58This is a really important point, which is why if the US does go down the road it’s a defacto socialisation of banking and finance.

FRANCES COPPOLA11:58It would be the death of banks.

Izabella Kaminska11:58The panic may have abated for now, but there’s no changing the longer trajectory which in my opinion is entirely related to the lack of core productivity in the Western system.

FRANCES COPPOLA11:59and that really is what Martin Wolf proposes in the FT today. To be fair, he proposed this about 10 years ago too.

Izabella Kaminska11:59Yes, but it’s still a nightmare.

FRANCES COPPOLA11:59@Graham I think that is why Dimon is trying to organise private sector bailouts of US midsize banks.

Izabella Kaminska11:59Higher interest rates are needed to reallocate capital into cash flow positive and profitable enterprises.

The problem is, we don’t have enough productive capital to scale from left in the West

We outsourced too much of it to China. And even if reshoring brings some of that back, in a high interest rate enviroinment that’s going to come wiht a very high investment cost.

FRANCES COPPOLA12:01@david CBDC is like unlimited deposit insurance. Same risk for the sovereign and the whole economy.

Izabella Kaminska12:01So the system seems to be doubling down on tech instead. Which doesn’t solve the core problem, as most tech doesn’t actually increase productivity.

which seems paradoxical but it’s true

You can see the computer age everywhere but not in the productivity statistics

So, fundamentally we have no choice but to go full reserve. The system is organically calling out for it, as it’s the only way to restore confidence. But this will create credit contraction, and it will be a net negative wealfare effect

Btw Gold is at new highs

(I think in sterling terms)

FRANCES COPPOLA12:03And eventually the system will revert to fractional reserve – as the crypto system did (which is like a simulation of the real system on fast-forward)

Gold and Bitcoin both up, and for the same reasons.

Izabella Kaminska12:04100% frances. Full reserve can only work in a totalitarian system. Because markets want to liberate money supply. Money is organically endogenous

They’re trying to have their cake and eat it, but really this is a sort of fall of the USSR moment. Sorry to say. Question is will the unravelling be slow or fast.

FRANCES COPPOLA12:05And on that cheerful note, we need to wrap up.

Izabella Kaminska12:05Ineed! Thanks so much frances.

Frances is back tomor with a special guest

FRANCES COPPOLA12:05Thanks everyone. Tomorrow at the same time, and my co-pilot will be Kathleen Tyson.

Izabella Kaminska12:05Kathleen Tyson, Chief Executive, http://Pacemaker.Global, de-risking the transition to the Multipolar economic order.

Thank you everyone! And thank you frances 🙂

FRANCES COPPOLA12:06I think the discussion will be fascinating. See you all at 11 am GMT tomorrow.