Good morning and welcome to Spot Markets Live, the weekly round-robin of stocks and markets news.

Today I’m excited to be joined by Neil Collins. He’s a veteran in the world of finance having “done” 19 years at The Daily Telegraph as City Editor.

Welcome Neil and thanks for joining us.

Would you like to tell us a bit more about your background before we kick off?

Neil Collins11:00

Neil Collins11:00Hello. I’m blogging at WordPress

alongtimeinfinance.wordpress.com

Anjuli Davies11:00

Anjuli Davies11:00And you do a podcast?

Neil Collins11:01as well as podding with Jonathan Ford

Anjuli Davies11:01Looked like you just did a fun one on Barclays recently?

Neil Collins11:01Yes. It’s called A Long Time In Finance, available on Spotify, Apple

Anjuli Davies11:02Cue a rush of subscribers I hope…

Neil Collins11:02I feel rather sorry for Barclays. They just don’t seem to be able to do anything right

For the full gruesome story, read The Bank That Lived A Little by Philip Augur

Anjuli Davies11:03

five year view

Neil Collins11:03It is brilliant, and beautifully written

Anjuli Davies11:03Will put that on my list

Neil Collins11:03In the last 20 years they have had over 60 directors (including non-execs)

Anjuli Davies11:04That’s a remarkable stat

It’s a bit quiet out there this morning. It’s a holiday in the US. Biden has made a surprise visit to Kyiv.

Not much corporate news but HSBC results are out tomorrow, Walmart in the US and Lloyds Banking on Wednesday. HSBC should be interesting to see what their outlook is now that China is reopening again.

Neil Collins11:05They are the lowest-rated major bank in the west! Perhaps Credit Suisse is even worse!

Anjuli Davies11:06They aren’t covering themselves in glory

What’s caught my eye this morning is Darktrace Neil

What do you make of them appointing Ernst and Young ?

Neil Collins11:06I really can’t work out what they actually do

Anjuli Davies11:07

Neil Collins11:07

Neil Collins11:07However, EY can’t claim to be short of relevant experience when it comes to checking out complex businesses

They were auditors to Wirecard and NMC Health

Anjuli Davies11:08It’s been a rollercoaster ride for the share price in recent months – bid speculation, bid, no bid, short seller report and now, it has commissioned a review of its finances by EY.

Here’s the Quintessential report with the punchy headline “the dark side of darktrace”

Quintessential Capital Management

We welcome Darktrace’s decision to initiate an independent review of its finances. We hope that such review will be of sufficient granularity, skepticism and impartiality to provide insights about the dubious transactions we flagged in our report.

Neil Collins11:10That doesn’t encourage confidence in the flotation document

Anjuli Davies11:10A lot of the Quintessential report details links to management and personnel from Autonomy who moved over to Darktrace

(and seemed not to put Autonomy on their public CVs for whatever reason)

Neil Collins11:11That was careless

Anjuli Davies11:11There were also some issues alleged around revenue recognition which was also an issue in the Autonomy saga

AS the FT notes

Of the 11 brokers that have published on Darktrace this year, nine retain buy ratings and only one, Stifel, has downgraded.

Neil Collins11:13It’s odd how some people find it so difficult to explain the business in words the rest of us can understand

Neil Collins11:14First question for any business: does your product or service actually work?

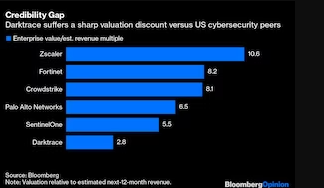

Anjuli Davies11:14It does seem to be underperforming its American peers. Bloomberg have this handy table

It’s made for a great headline in City AM

“A REIT mess”

Neil Collins11:16If Home Reit had done what they said they were doing, and nothing else, they would have survived. It was good idea

Anjuli Davies11:17Neil, what’s going at Morrisons?

Neil Collins11:17I’m not sure. The debt issued for the takeover is said to be trading at 85 cents in the euro

There are grumblings about how much faster their shop prices have risen compared to the others

Morrisons hiked prices by almost a fifth in the past year – more than any other major grocer and double the rise at Sainsbury’s

Neil Collins11:19They have fallen to 5th in the supermarket league table

The Daily Mail says they have been “private-equityised”

Anjuli Davies11:20That’s a new coining of a word

Neil Collins11:20The owners, as I’m sure you recall, are Clayton Dubilier & Rice

Anjuli Davies11:20They have a track record here don’t Neil?

Neil Collins11:21There is plenty of talk of a supermarket price war, but most of these so-called price wars are just a few items for show and headline-grabbing

Anjuli Davies11:22So, is this going to play into the UK retail consolidation story?

Sainsburys is always a rumoured takeover target

Neil Collins11:22Morrisons used to be somehow differentiated from the others. Now they just look like an also-ran

Anjuli Davies11:24Meanwhile Aldi is recruiting 6,000 new staff across the UK

Neil Collins11:24Darren: I’m sure you’re right. Remember the Marmite wars…

Anjuli Davies11:24I must say I much prefer Morrisons to Aldi or Lidl but that may just be revealing how Middle Class I am

Neil Collins11:25What, not Waitrose?

Anjuli Davies11:25I am in the Waitrose belt out here

Neil Collins11:27I see NatWest is starting a buy-back

I find these things puzzling.

There never seems to be any mention of the price at which they are worth doing for the remaining shareholders

You could define them as Paying some shareholders to go away at the expense of those who remain

Anjuli Davies11:30HSBC and Lloyds report Tuesday and Wednesday respectively

Neil Collins11:30Simon Wolfson is the master of the buyback. Next buys in its own shares at prices below the return from investing in the business

Anjuli Davies11:31AJ Bell investment director Russ Mould and head of financial analysis Danni Hewson said: “Lloyds will be last of the big five FTSE 100 banks to report its results, but the figures should be no less informative for that, especially as the shares are on a good run – they are up by around 40% from the autumn lows, although that does mean they are still only broadly flat over the past year.

“Moreover, Lloyds is the UK’s largest mortgage lender, with a book of some £300bn, has a £14bn credit card book and has net exposure to UK commercial real estate of some £10bn.

“The headline figure to watch will be pre-tax profit. For the fourth quarter, analysts are looking for £1.9bn against £1bn a year ago, when £1.5bn in remediation and compensation costs, restructuring charges and asset write-downs weighed heavily. That means for the full year, the consensus forecast for 2022’s pre-tax profit is £7bn, against £6.9bn in 2021.”

Neil Collins11:31Are the banks’ declared profits informative?

This time round, they will all be setting aside as much in provisions as the auditors and HMRC will allow

So some of those provisions should come into profits in future years when they are released

It’s almost like the old days, when banks only indicated whether profits were up or down, and when interpretation relied on the dividend declaration!

Anjuli Davies11:34AS Roger said…

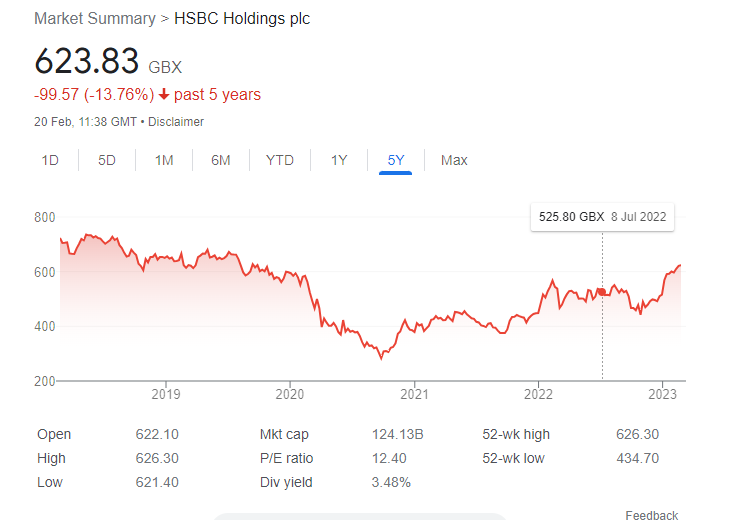

It feels like HSBC still isn’t where it should be

Neil Collins11:36Can HSBC hold together?

Anjuli Davies11:36Exactly

Where does the UK business fit in really

Neil Collins11:36In the end, I think it will split into a Chinese bank, perhaps based in Hong Kong, and a domestic bank in London, called Midland Bank

Anjuli Davies11:37What’s Ping An up to next ?

Neil Collins11:37I think it’s down to politics rather than shareholder activism

Anjuli Davies11:37The insurer has been pushing for more radical action

that’s a five year chart

Neil Collins11:39Cow-towing to the Chinese government is always a bad look. I’m amazed it has done more damage to the UK business

Anjuli Davies11:39Down nearly 14% but in the last year alone its up 14%

Neil Collins11:39John: most of them could do with one!

Anjuli Davies11:41Sticking with banks, just wanted to mention the continuing saga of Credit Suisse which has now been redubbed on financial twitter as Debit Suisse

Reuters actually had some interesting news last week about it’s spin off

They got hold of some internal documents which purported to forecast a revenue rebound in its Credit Suisse First Boston spinoff which is has described as a “super boutique”

Credit Suisse Group AG (CSGN.S) is marketing its First Boston investment banking unit to investors as a “super boutique” and sees revenue surging to as much as $3.5 billion, as the embattled lender seeks to raise funds for the revamped business, a company document seen by Reuters shows.

I struggle to do the maths here

a surge to $3.5 billion

Neil Collins11:43What’s a super boutique?

Anjuli Davies11:43Exactly Neil

at the same time details emerged about what Michael Klein was being remunerated for running the new business and selling his old one

Neil Collins11:44You surely don’t expect a banker to work for the shareholders?

Anjuli Davies11:45The bank, trying to recover from a series of scandals, said it had agreed to buy the investment banking business of M. Klein & Company LLC, for $175 million.

Questions remain if Credit Suisse has done enough restructuring

You should definitely do an ALTIF podcast on this Neil

@Helmholtz that’s interesting

Neil Collins11:47Darren: CS reminds me of the old adage. When a bank has money to spend, it’s not a question of whether it will spend it, but which tree it will choose to spray it up.

Anjuli Davies11:49Neil has told me he quite wants to have a kick at ESG and defence stocks

Neil Collins11:49I’m not a great fan of ESG.

Anjuli Davies11:49Who needs Izzy …

Neil Collins11:49The holier-than-thou crowd felt very virtuous in steering away from defence stocks.

Nasty businesses, making things that kill people, in the bracket as tobacco or (nowadays) Oil companies

The woke crew are having to think again as they watch what it happening in Ukraine

Defence turns out to be quite important after all

So, of course, does oil.

Anjuli Davies11:53Why do the real gains come to the fund managers Neil?

Neil Collins11:55Because they are rewarded by the size of the funds they manage. Performance is what matters to the investor, but is secondary to the manager – and much more difficult than attracting new funds

Anjuli Davies11:55

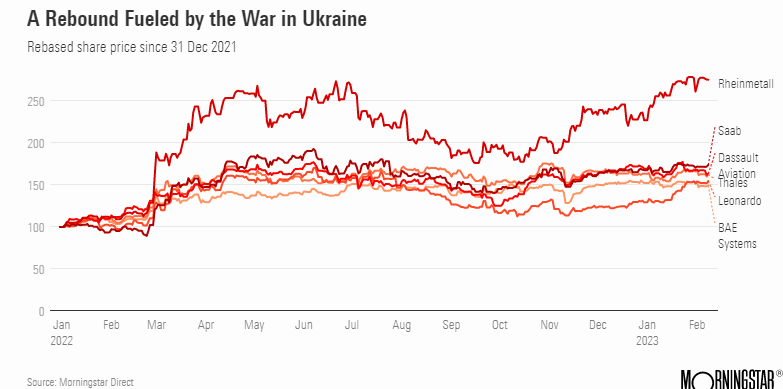

Morningstar have done some research on European Defence companies – are they now overvalued

Good point @Roger

this is an interesting stat

Before the war in Ukraine started, military spending was increasing around the world.

In 2021, it reached an all-time high of $2.1 trillion (£1.75 trillion), according to SIPRI, an independent institute based in Stockholm, Sweden.

At the time, while the US was slightly reducing its military spending to $801 billion, focusing its R&D on next-generation technologies, Russia and China were increasing their budget by 2.9% and 4.7% respectively.

Have you got an adage about war for us Neil

To see us out

Neil Collins11:58Now we need the UK to stop wasting defence billions on useless projects

Please don’t mention Gordon Brown’s aircraft carriers

Anjuli Davies11:59On that note…

Thank you so much Neil and please come back soon….we managed to make the most of a slow news day

Neil Collins12:00A pleasure