Today’s Spot Markets live session is with Dario Garcia Giner, assistant editor of the Blind Spot

Izabella Kaminska 10:59

Izabella Kaminska 10:59HELLO!

Welcome to a front seat to the Fall of Rome. Part Deux.

Exciting isn’t it?

Who knew my Ancient History degree would come in so useful?

Dario Garcia Giner 11:00

Dario Garcia Giner 11:00These days it sounds like a history degree is more like a degree in current affairs

Izabella Kaminska 11:00haha

This is Spot Markets Live, the real-time markets chat that takes you on a whirlwind tour of the markets.

But which currently emulates a not very committed Catholic’s approach to attending a weekly Sunday mass.

This will change though. We have plans, even as Rome crumbles.

We are sticking to the one-hour Monday session, but as markets go mental this September and October we will be firing up these sessions sporadically to help members navigate their way around unexpected goings on.

Consider it a sort of safe space interactive meeting zone for assessing crazed market events.

Despite not having any live sessions the last two weeks we’ve still been growing the member count – so that’s good news.

But before we crack on…and in the style of a Sunday Mass, I guess, I will now be asking forgiveness for overpromising and under-delivering.

Anjuli Davies will now be joining us next Monday.

The delay is due to the fact that we both overlooked that today was the start of school.

But it’s great to have her onboard. She was formerly a Reuters finance/M&A correspondent as well as a senior finance journalist at the Telegraph.

Today I’m joined by Dario Garcia Giner – the Blind Spot’s trusty second in command, with a penchant for meme stocks.

BUT ALSO – importantly — another HISTORY STUDENT

Dario Garcia Giner 11:03Hi Izzy, hi all!

Izabella Kaminska 11:03We know our fall of Rome narrative here at the Blind Spot.

Before we crack on with markets, we should commemorate the truly big news of the week with a special tribute.

RIP Gorbachev

Dario Garcia Giner 11:04

Dario Garcia Giner 11:04Press F to pay respects

Izabella Kaminska 11:04This is from my collection of emergency birthday cards which I inherited from my mother, who collected them in case she ever needed one in a hurry. They date back to the 80s and were never used.

Hello to the rabble! Good to have you back. Please pipe up and chip in as much as possible.

We all learn from each other.

Dario is burning to get you news about BBBY. But first markets.

Quick overview of the market situation over August and today.

We know markets got spooked after Jackson Hole, but it’s not exactly been a boom of a summer either:

Why anyone was surprised by Powell’s hawky tones surprised me. But clearly, I’m in some sort of bubble.

And it may just be the case that the West’s losses are Russia’s gains:

Dario Garcia Giner 11:06

Dario Garcia Giner 11:06The rouble’s still staying supported.

Izabella Kaminska 11:07

Izabella Kaminska 11:07Meanwhile, it’s a 20-year low for the euro!

Congratulations all around for achieving a great benchmark.

Over on the FTSE today Glencore is the top gainer up 3.18% followed by BAE, BP, Antofagsata, Rio Tinto, Shell – what I would call the “we’re not officially in a resource-focused World War 3 situation (but we are really) Stock Complex Squad” – better known as the War Complex Trade.

Though I’m in the market for better acronyms/identifiers. (You know, like Stay At Home stocks)

WARCOM stocks?

If anyone has any better ideas… shout

Dario Garcia Giner 11:08Staying Alive (STAV) stocks?

Izabella Kaminska 11:08The top losers today are 3i, Coca Cola and Hargreaves Lansdown.

But since it’s the WARCOM trade that’s the mover today, let’s check in on the energy chaos in Europe.

Dario Garcia Giner 11:09A lot of flurry in diplomatic channels and markets as a result of news coming through this weekend that Russia is set to cut gas exports to Europe via Nord Stream indefinitely citing vague regulatory and bureaucratic impediments:

Izabella Kaminska 11:09The other big news over the weekend is also the G7’s ingenious solution to curbing inflation – a price cap on Russian energy.

Yep, they’ve gone full Diocletian. Because every fall of an empire must have its mandatory maximum price edit.

(See when you subscribe to the Blind Spot, you get all this ancient historical context that you just won’t get anywhere else)

Dario Garcia Giner 11:10Good thing we’ve learned a bit or two from History. Hold up…

DIRECTED AT RABBLE: I like NUCOW!

Izabella Kaminska 11:10@John Courable – not bad

I like COW too tho

Dario Garcia Giner 11:10Sounds like an acronym we can milk

Izabella Kaminska 11:11As you may have noticed from my rantings on Twitter I think this cap is all a big joke. I’m also surprised that people like Janet Yellen, who should know better, are pushing the line that this might be effective.

As one commodity trader told me:

G7 excludes China, India etc…who are all increasing their intake of Russian oil…inability to access insurance/shipping markets have not deterred them much like Iranian oil exports to China haven’t been deterred. China is willing and capable to self insure.

Thus, doesn’t a price cap open up the number of potential countries not participating in sanctions to purchase Russian oil (by accessing services and not having to self insure)…doesn’t this create greater competition for Russian bbls and raise their price?

Dario Garcia Giner 11:11Sounds about right

I’ve been keeping up with the increased intake of Russian oil particularly by India thanks to our Discord, which you can join here https://discord.gg/mqJDz2pe

Izabella Kaminska 11:12

Izabella Kaminska 11:12Yeah, it’s all very short-sighted. If you haven’t read Craig Pirrong’s piece on the price caps, you should.

Here’s his great piece on the folly of price controls

(Btw Craig, who is the top expert on energy markets and regulation/manipulation, has also agreed to do a podcast with me this week, so look forward to some more analysis from him later on).

Izabella Kaminska 11:14And actually, UK natty prices are going berserk again. They’re up 33% this morning on the back of the Nordstream pipeline closure news.

They were punctured pretty heavily last week on nearly full storage so that’s a big multiple based on a previous big low. But the Nordstream news is definitely feeding in again.

Dario Garcia Giner 11:14This is positioning us for an Energy Lehman moment, no?

Izabella Kaminska 11:15Looks like it

Bloomberg reports that the governments of Sweden and Finland have decided to create emergency backstops to help utilities struggling to trade in power markets gripped by unprecedented turbulence. :

This bit is the key bit

They’re setting up liquidity facilities made up of loans and credit guarantees, worth $33 billion in total, to avoid some power companies going into technical defaults as soon as Monday over surging collateral requirements. The aim is to prevent Russia’s energy curbs from sparking a financial crisis.

“This has, in a way, the ingredients for an energy-industry Lehman Brothers” moment, Finnish Economy Minister Mika Lintila said at a news conference in Helsinki, referring to the US investment bank whose name has become synonymous with systemic risk after its collapse set off the global financial crisis in 2008.

Dario Garcia Giner 11:16🙄

Izabella Kaminska 11:16Well, Truss is also going about saying we won’t need rationing.

I find that improbable.

The UK is definitely better positioned, we still have about 80% I think self-reliance, but the marginal differential is what sets the price.

There’s some speculation on the Blind Spot discord about the anti-NATO protests in Europe over the weekend and whether they were authentic or not.

The Prague ones were dismissed as having been organised by Russian sympathisers or even by Mr P himself.

And the same goes for the German ones.

Dario Garcia Giner 11:18Indeed, lots of things going on in Europe and in Prague – or as I like to call it, Neu-Sudetenland

A recent poll in Italy showed for the first time a 51 per cent majority of Italians did not support sanctions on Russia.

Izabella Kaminska 11:19Again, lots of speculation that this isn’t authentic.

but here at the Blind Spot, we try to look at the signal objectively without necessarily defaulting to the idea that everyone who says something we don’t like must be the enemy.

They could be the enemy. But it’s worth keeping an eye on sentiment. I would be very surprised if the popular will is maintained for the support of Ukraine as these energy shortages increasingly bite.

Dario Garcia Giner 11:21Considering the insane rise in energy prices, and the mainstream media & politics framing of this price rise as correlated to the Russian invasion, it would make sense that people tie the cost of living crisis to their countries’ allegiance to NATO objectives.

Not to say there are no Russian spooks in the mix, but the anger makes sense!

Izabella Kaminska 11:21Two things can be true at the same time. Also it’s not entirely Russia related – the energy shortages are also the product of major under investment due to ESG and net zero policy.

The sundays are full of news about police fearing surging crime and civil unrest. I find this exceptionally annoying.

But who knows, I’ve been wrong about stuff like this before. I expected mass civil unrest before covid lockdowns. It never happened.

Nonetheless, I feel signalling this “civil collapse” stuff is a very self-fulfilling prophecy.

I prefer the Edward Heath messaging

as wonderfully highlighted in Adam Curtis’ Mayfair set

Anyway, lockdown unrest didn’t really happen – probably because the world was pacified with furlough money. That sort of financial support is less likely this time round.

(For those keen on keeping a close eye on signs of civil collapse check out our Mad Max channel in the discord.)

Meanwhile, Zelensky is on the front page of the Sunday Times and quoted as saying the “energy crisis is the price to avoid a world war.” – but surely he has it backwards?

This seems very bold from Zelensky, but I’m not a political analyst so I will leave it there.

What do you think Dario?

(or anyone else)

Dario Garcia Giner 11:25Zelensky is currently the effective warlord of a country struggling to survive a brute force invasion by its neighbour.

I expect him to play whatever cards he can in an attempt to win.

However! This does not mean he is correct in a European context, or that he will maintain the will of the European people.

As an example, Baerbock, Germany’s Foreign Minister, has recently triggered many by saying:

“If I promise the people of Ukraine: ‘We will be by your side as long as you need us’, then I will keep this promise. No matter what my German voters think. But I will support the people of Ukraine as promised.”

Izabella Kaminska 11:26Yeah, I can imagine that triggered a lot of people

Dario Garcia Giner 11:26Indeed

That being said, I think we should all take heed of the context within which Germany’s Foreign Policy operates

Though the German foreign ministry has claimed criticism of Baerbock online is ‘pro-Russian disinformation’, it makes logical sense for the German foreign minister to give emphatic public declarations in favour of Ukraine.

We should not forget that arguably Germany’s defining geo-political trait in Europe is its Ostpolitik, east-facing, Russia-friendly politics, traditionally defined by German energy needs.

I wouldn’t be surprised if we see Germany back itself out of the corner they are currently in by emphasising their lack of options before an energy crisis as they quietly loosen their sanctions this winter.

To do that, Germany first needs to harden its public image so it can eventually loosen its hands privately for greater freedom of movement.

But that’s just my speculation

Izabella Kaminska 11:27Okay… let’s move on

Before we move onto stock and macros news though, just a little reference to spark spreads.

I’ve already mentioned him once but he really is very good at all this

Craig’s Pirrong has another piece on what the dark and spark spread market is indicating. A spark spread, btw, is jargon for the difference between the price of electricity and the cost of natural gas. A dark spread (while it sounds like a forecast of blackouts) is the difference between the price of power and coal.

As Craig notes German Dark spreads are currently HUGE.

Dario Garcia Giner 11:29Interesting concepts!

Izabella Kaminska 11:29“The German dark spark for 2 quarters ahead (Jan-Mar) is over €1000, and the UK dark spread is over €600. In other words, it’s good to own a coal plant! By the way, these are clean darks, so they take into account the cost of carbon. Meaning that the market is sending a signal that the value of coal generation–even taking into account carbon–is very high. This no doubt explains why despite massive green and renewable rhetoric in China, the Chinese are building coal capacity hand over fist. It also points out the insanity of European policies to eliminate coal generation. Even if you believe in the dangers of carbon, the way to deal with that is to price it, rather than to dictate generation technology.

But do read the full piece

Dario Garcia Giner 11:30That’s interesting. I have some experience looking at the coal industry in EE from the lens of APAC-based clients, to put it that way?

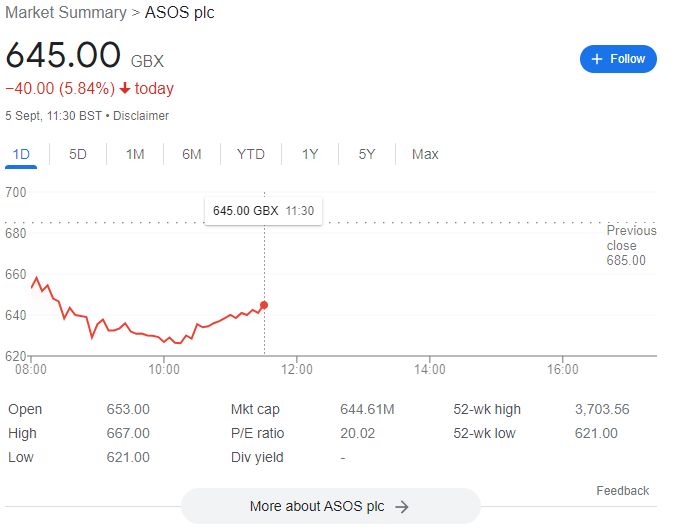

Izabella Kaminska 11:30ok now for our weekly commemoration of “Those who have fallen to inflation”

Think of this like the Oscars “in Memoriam” section

In this week’s commendation we have Matalan, Asos and Joules (Not quite fallen yet but definitely succumbing)

The Sunday Times/City Am report that Matalan’s founding family is seeking a buyer ahead of a critical refinancing, as inflation and weak demand wreaks havoc on fashion retailers Asos and Joules.

Though you would think there would be demand for woolly jumpers! Matalan is privately held, but the others’ stock is not faring too well.

Dario Garcia Giner 11:31

😂john…

Izabella Kaminska 11:32(@JC – if you haven’t checked out Dario’s shitflation post, take a look)

Dario has a theory that because he had an unexpectedly bad hangover after a pub crawl a few weeks ago, this must be indicative of a pub landlord conspiracy to boost profits by watering down the nation’s kegs, probably by using cheaper non compliant and health compromising mixing agents.

Dario Garcia Giner 11:33https://the-blindspot.com/hi-shrinkflation-meet-your-cousin-shitflation/

More or less

Izabella Kaminska 11:33I mean, it’s not irrational.

And desperate times do call for desperate measures.

And it is definitely true that on the SME side of things, the energy bills situation is really getting to a head.

Unlike in France, there is no price cap for SMEs in the UK.

So small businesses like cafes etc are finding that their bills are in some cases going up as much as 4x (depending on the previous deals they had).

The question at this point is, what proportion of these small businesses are currently trading knowingly insolvent.

I don’t blame them if they are, because clearly they are anticipating or hoping for some sort of government intervention – but if that doesn’t happen, then technically if they are found to be trading knowingly insolvent, they risk losing limited liability protection.

That means these guys’ homes might be on the line.

Dario Garcia Giner 11:35The head of the Association of Convenience Stores has recently asked for just that sort of support, writing to the Chancellor that the sector needs a £575mn support package to stay afloat.

Izabella Kaminska 11:36@JC – talking to pub landlords is always interesting.

Izabella Kaminska 11:36Right. It’s grim out there. And yet the banks aren’t all that fussed. Weird.

Moral hazard I suspect

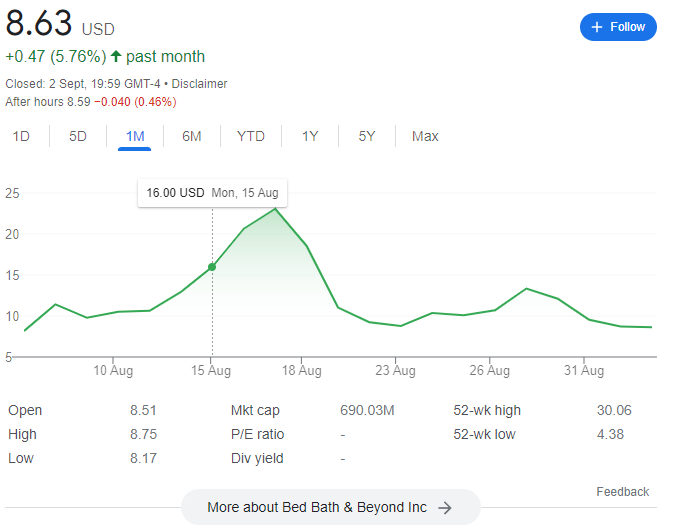

In equally grim news, let’s go to dario for the BBBY news.

What’s up in memestock land?

Dario Garcia Giner 11:37Well, things are getting even crazier Izzy

It was reported yesterday that BBBY CFO, Gustavo Arnal, had fallen to his death from an apartment in Tribeca.

Izabella Kaminska 11:38

Lots of people falling from windows generally.

Dario Garcia Giner 11:38I’m glad our forefathers blessed us with such an appropriate term. DEFENESTRATION.

Izabella Kaminska 11:38But I had no idea BBBY was part of the Russian destabilisation plan

Dario Garcia Giner 11:38Arnal, the CFO, had just been named in a lawsuit brought on Aug 18 in Virginia, where he was accused alongside Cohen of participating in a pump n dump scheme on BBBY.

The suit claims, on behalf of investors who bought into BBBY just prior to and during the meme stock frenzy, that Cohen approached Arnal with offers to control the company stock.

Here are the two accusees in question.

Left, Arnal, and right, Cohen.

The accusation states Cohen would drive up interest while Arnal ensured insiders wouldn’t flood the market with stock.

Which I find fascinating!

Izabella Kaminska 11:40Yes, this speaks to your ongoing hunch that there is more to Memestock pumping than just organic internet campaign by nostalgic internet nerds.

Dario Garcia Giner 11:40100%

The BBBY disclosures are worth a closer look.

They suggest the company was on an upward trajectory until August 31 when BBBY forecasted a larger than expected slump in sales and announced it was cutting 20% of its corporate and supply chain employees, among other bad news.

Izabella Kaminska11:41Dario Garcia Giner 11:41Until then it had been a very secondary meme stock player. The initial rally that earned it true ‘meme stock’ status was on Friday, August 5. But this proved short-lived.

By August 18, news that Ryan Cohen had dumped all of his stock sent the stock spiralling down, wiping out most of its meme-related gains.

But things got weirder from there.

The FT then did an article on a mysterious 20-year-old called Jake Freeman who had received a small loan of 25mn from friends and family and made 110mn when the trade went viral.

It noted the Freemans were involved in trading in MindMedical, Freeman’s uncle being the company’s co-founder and former Chief Medical Officer (though these last two facts were not reported in the FT article)

The key date to bring to your attention dear rabble is August 16.

Izabella Kaminska 11:43Is this the day the stock popped?

Dario Garcia Giner 11:43And more!

On that day, Cohen publicly submitted a document showing he had a large number of shares in the company, which prompted a rise in the stock price of over 75%.

HOWEVER

On that same day (!!) it turns out Cohen actually began selling all of his shares in BBBY. This wasn’t disclosed until August 18.

Freeman, as shown in the FT article, sold his shares at near-highs of 27 a share on August 16 too.

And, most fascinatingly of all, the news we learn today is that Arnal also sold a chunk of stock on August 16 at 29.95 a share – except, as we learned today was, this was a long pre-planned trade for the CFO since April 2022.

This clearly indicates some type of shenaniganery, in my eyes

Izabella Kaminska 11:45Yeah, I’d be very surprised if the SEC isn’t looking at this closely

Dario Garcia Giner 11:45The latest update we can provide on the story is a follow-up on Mind Medical Stock

Since the first FT article that incorrectly distanced the Freeman family from the stock(by failing to note that Freeman’s uncle was a co-founder and former CMO of the company) the stock has achieved a 1,769% rise.

Recently, MindMed has been dropping on negative financial forecasts

I’ve been browsing the comments from investors in the company’s subreddit this morning. They are NOT happy with Freeman’s conduct and are suspicious of any attempts by the young ‘investor’ to dump his own shares in MindMed.

A new press release from the company is expected to be shared Tuesday morning.

In case any of you guys want Freeman’s professional Reddit account, by the way, here it is

Izabella Kaminska 11:47* Just a note – this account is already in the public domain.

Dario Garcia Giner 11:47And the absolute latest on the topic is something entirely speculative and bordering on the morbid.

There were reports of a second person also being hospitalised in the CFO incident with minor injuries.

If the report of this injury is not directly connected to the fall of BBBY CFO (as in, he landed on top of him or something like that) questions regarding his death may continue to spiral in the fake-news-o-sphere.

Izabella Kaminska 11:49Hang on I’m confused.

Dario Garcia Giner 11:49Let me quote you from the reporting.

The source is apparently the New York City Fire Department (FDNY) from the site of the CFO’s landing on the ground.

“A second person, also unidentified, was hospitalized with minor injuries, according to a spokesperson for the FDNY.”

██████████████████████. This was before ██████and █████████

██████████████████████. But what nobody expected was ███████████████

████████████████ and ██████████████████████████████

██████████████████ which would be crazy right? ██████████████████████████████.

Izabella Kaminska 11:51Very intriguing. We will keep an eye on it.

MEANWHILE

In the fall of free markets:

This is out just now:

They want to halt power derivatives markets!

European ministers will discuss special measures to rein in soaring energy costs, from natural gas price caps to a suspension of power derivatives trading, as the bloc races to respond to the deepening crisis.

Dario Garcia Giner11:52They wanted to get Gorbachev out of the way…. 😂

Izabella Kaminska11:52UNPRECEDENTED

(Well, apart from Ancient Rome)

I mean they are basically nationalising the power market.

Shame Gorby isn’t around to warn them how that might go a bit wrong.

All the more reason to watch my podcast with Craig Pirrong.

So we’ve got another 7 mins or so — before we pack up, perhaps a quick ref to two other stories that caught my eye.

Turkish inflation is now at 80%

that’s a 24-year high

(And it was below expectations – lol)

Dario Garcia Giner 11:55Woah!

Izabella Kaminska 11:56I’m not an expert on Turkey, but Dario’s been keeping an eye on the geopolitical side of that story.

what’s the latest?

Dario Garcia Giner 11:56I wonder if Turkey’s grim economic news has affected its attempted push into Northern Syria.

Erdogan has seemed extremely keen to push into Northern Syria since at least the Spring of 2022. Everything seemed to be leading up to that during this summer.

However, in early August, Erdogan came out with very conciliatory comments towards the Assad Regime – which had just aligned itself with the Kurdish YPG-led SDF units in Eastern Syria (the units that would have been in Erdogan’s line of sight)

Turkey’s operation in Northern Syria appears to be continuing mostly through the use of artillery, aerial attacks, and assassinations, rather than a full-on mobilisation as in the previous Turkish operations

Izabella Kaminska 11:58Right – I need to read up on that

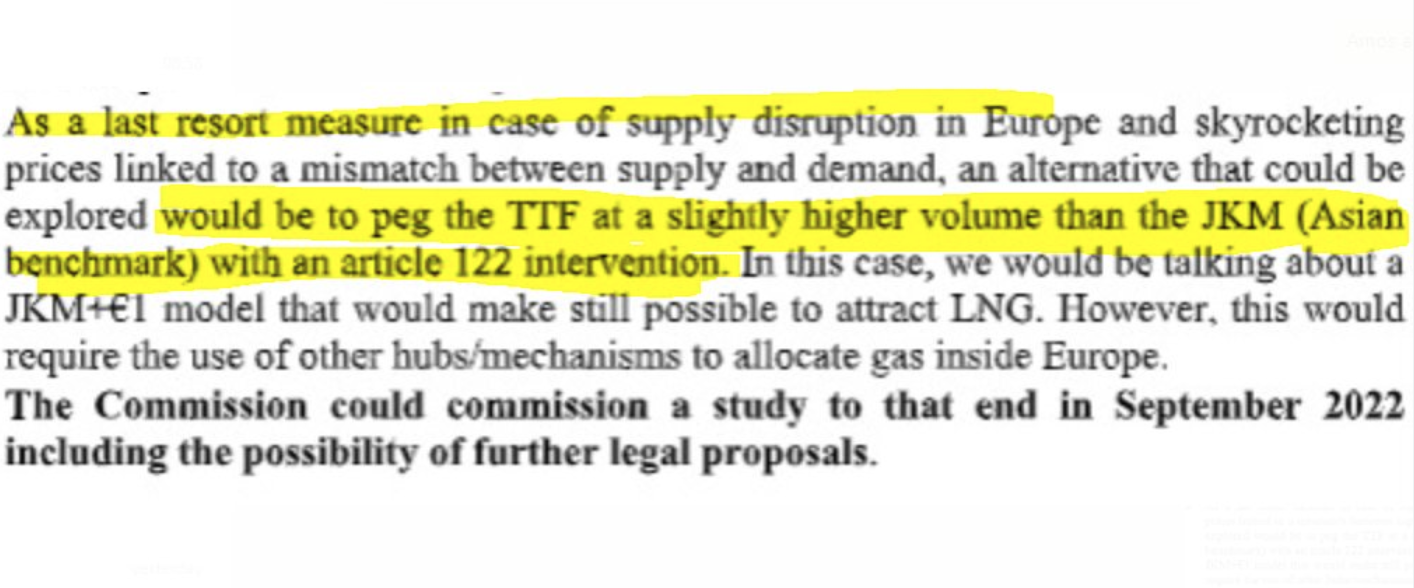

FYI on the nationalisation of European Power grids – my former colleague Javier Blas has a good take

As he notes;

“Among the “there’s-not-such-a-thing-as-a-dumb-idea” brainstorming, the below is among the most radical that I have seen emerging from the European Commission: scrapping TTF and replacing it with JKM+€1. Emphasis the below is an “idea”, rather than a policy “proposal”.”

I mean it really is hilarious that they waited till Gorby was dead to bring back gosplan.

You can just imagine the strategy meeting?

“Yeah, like … what if we just nationalise everything? That will make the problem go away right?”

Speaking of which…

Stuart Kirk, the man who got cancelled for putting levity into an ESG presentation, is back with an oped in the FT

He is calling on ESG to be split into two. Worth a read. I think he makes a lot of sense. And I certainly I myself have noticed the conflict between the Es and the Gs, in ESG.

Here’s the key part:

The flaw is that ESG has carried two meanings from birth. Regulators have never bothered disentangling them, so the whole industry speaks and behaves at cross purposes. One meaning is how portfolio managers, analysts and data companies have understood ESG investing for years. That is: “taking environmental, social and governance issues into account when trying to assess the potential risk-adjusted returns of an asset.” Most funds are ESG on this basis. Weather, corporate culture or poor governance always influence valuations to some degree.

….this approach is very different to investing in “ethical” or “green” or “sustainable” assets. And this second meaning is how most people think of ESG — trying to do the right thing with their money. They prefer a company that doesn’t burn coal, eschews nepotism and has diverse senior executives. Two completely different meanings then. One considers E, S and G as inputs into an investment process, the other as outputs — or goals — to maximise. This conflict leads to myriad misunderstandings. In an ESG-input world, for example, it is OK to own a polluting Japanese manufacturer with terrible governance if these risks are considered less material than other drivers of returns. Ditto if they are already discounted in the share price.

Of course, if you had read my “Holier than Dow” pieces from before 2020 on FT Alphaville none of this confusion will be news to you.

Dario Garcia Giner 12:04We get it, you’re a Cassandra

Izabella Kaminska 12:04Yeah, Sorry. Even I’m bored of saying I told you so. Though to be fair Kirk’s point is actually much deeper than the one i was making.

I think on that note we call it a day. We will be back next with Anjuli. If you want to sign up to the unredacted Live Discord details for a Coodash login can be found here.

Meanwhile, I am taking part in the first-ever Nocoiner event today.

The Crypto Policy Symposium – as it’s also called.

It starts at 3 pm UK time.

I was supposed to be compering it today, but got the last minute, “we don’t need you after all” message last night.

The symposium is an entirely amateur and self-funded effort, so it could still end up being the Fyre Festival of digital conferences.

Especially now I’m not the compere. But do check it out. They’ve got some great names.

😜

Here’s the link.

Alright then, let’s leave it there.

Dario Garcia Giner 12:07Thanks all!

Izabella Kaminska 12:08Remember feedback is always welcome! And watch out for spot markets live impromptu sessions – we will advertise them on Twitter, Discord and by email.

Take care!