Julian Rimmer10:30

Julian Rimmer10:30Good morning, Aloha and greetings fellow market wizards

With open arms we welcome back to The Blind Spot, its founder Izzy Kaminska to the place I hope she thinks of as home.

Recall, that ‘Home is the place where, when you have to go there, they have to take you in’

(Robert Frost, not me)

As you know, because Izzy was very forthcoming in telling us, Izzy mingled with the glitterati and the nomenklatura at the Arc Forum this week and is now, therefore, an ‘ally of responsible citizenship’?

That right, Izzy?

And endowed with a community vision for a better world?

That’s your mission statement.

Does this approximate how you feel this morning, Izzy?

Izabella Kaminska10:32

Izabella Kaminska10:32I am now definitely a responsible citizen.

Actually, to be honest, I’m in recovery.

Julian Rimmer10:33They say half of life is spent going somewhere and the other half coming back, wondering why the hell you went in the first place? Is this how you feel about it now?

(That was john updike. Not me)

Izabella Kaminska10:33I don’t think it’s a coincidence the ARC forum was immediately followed by 40 days and 40 nights of flooding in certain parts of the UK (aka storm Ciaran).

Which does make me wonder if in reality, I had participated in some strange occult ceremony. Unwittingly I should add.

Though have to say, not too much flooding this morning in leafy West London.

Julian Rimmer10:34I saw ARc’s slogan is adopted from MLK

The moral arc of the universe is long but it bends towards justice?

About that MLK was dead wrong.

it’s asymptotic.

What learnings did you receive?

Izabella Kaminska10:35Look. I have a lot of sympathy for many of the points of view being expressed.

And don’t hate me but… I thought Paul Marshall’s address was actually really good, probably the best from the conf (mainly because he just repeated a lot of the points I’ve been making for about 10 years or more about capitalism, i.e. crony capitalism BAD, monopoly capitalism BAD, woke (aka ESG) capitalism BAD.)

If you want to see that address, it’s here. One of the few that made it online.

I’m also a big fan of Merryn Somerset Webb so her anti ESG panel was to my liking too.

And finally, I liked the emphasis on protecting kids from the ills of technology and social media.

And generally on empowering women who don’t want to be career ball busters.

(Seriously Julian, these days I dream about becoming a housewife. Something my 20-something self would be appalled by.)

Julian Rimmer10:36I dream of becoming a housewife too

Izabella Kaminska10:36But I just couldn’t get into the concept. Mainly because it wanted to emulate WEF too much.

(Badge hierarchy and everything. Tho top-tier VIPs, “the ARC-Angels” as I call them, were pink for example. I was a humble yellow).

Julian Rimmer10:36Arc-angels excellent

Izabella Kaminska10:36And in doing so it created another bubble where people mostly preach to the choir and persuade nobody new about their opinions. It was a giant safe space for anti-wokeism in that sense.

Yes yes, it was more down to earth. No private jets or Piano bars. But what I really want to see is a panel where Justin Trudeau and Klaus Schwab fight it out with John Anderson and Jordan Peterson.

Also, there was too much of a gung-ho attitude for my liking and no nuance about the Middle East.

Funnily enough, despite preaching about the importance of traditional families and not going overly woke, overall it achieved a higher DEI score than most openly woke events. Power women and diversity everywhere you looked. Much like the irony of the Tory party having had three female leaders and an Indian leader and the Labour party having had none.

Julian Rimmer10:38Any other interesting sightings? because not enough names have dropped on my feet yet.

Izabella Kaminska10:38A strange collection of people. So yeah, I think Dario shared the news about Erik Prince, Holly Vallance etc. But some other surprises included Eric Weinstein, Jimmy Carr and that Zuby dude who is always being retweeted by Elon Musk.

And the real piece de resistance was Jordan Peterson’s tearful closer speech which gave way to an operatic rendering of “DO YOU HEAR THE PEOPLE SING!”

Yes. Really.

BUT ENOUGH ABOUT ARC!

Julian Rimmer10:38OK, tempus loquendi

Izabella Kaminska10:39So before launching into some stuff about Australia.

Just wanted to flag that overall the BoE yesterday was super boring, with the big news being that the forecasts project almost no growth. Lovely.

Julian Rimmer10:401000 people on the call? It’s like the blind spot

Izabella Kaminska10:40haha

yes

Julian Rimmer10:40(except we have a better demographic)

Izabella Kaminska10:41Indeed, we have, I see, Robert McCauley in the house.

Julian Rimmer10:41Front row of the stalls

Izabella Kaminska10:41Which is great. Because he’s just posted a fab new paper about how to contain the problem of central bank losses.

It’s here.

I learned a lot from this.

The main thrust is that rather than have everyone worry about whether central bank losses really matter or not, why not nip them in the bud, specifically in the ECB, by engaging in a very elegant “Bond Swap”

It’s such an obvious solution, I can’t believe I didn’t think of it before.

Julian Rimmer10:43I hadn’t thought of it.

Izabella Kaminska10:43Here’s the preamble:

Euro area central banks are reporting losses as they pay banks 4% but collect only 1% on trillions of euros of bonds bought to spur growth with lower yields. Once central banks exhaust their capital, they may need to go cap in hand to their governments. Recently, the ECB ceased to pay interest on commercial banks’ 1% required reserve against deposits. Now some propose jacking this up tenfold to stanch central bank losses. With fat profits and rich, dividends, commercial banks can easily pay, it is said.

So Robert’s idea (and he’s in the rabble so do fling further questions his way) is basically one cbank’s loss is another respective government’s gain.

So why not crystalize that, by essentially allowing governments to book the hypothetical gains of being able to buy back their bonds at a discount, something that would reduce the overall debt burden, and curb further exposure to more losses if rates continue to rise.

The context of course is that this mostly applies to the ECB. Why? Because the BoE has already had its potential losses indemnified by the government.

While the Fed has engaged in some excellent accounting shenanigans to ensure it never appears to be in a loss.

Great footnote on that Robert, btw.

From his paper:

In a private communication, Peter Stella, former head of the Central Banking Division of the International Monetary Fund, terms this device unoriginal, disingenuous, and disgraceful accounting worthy of a Banana Republic.

Gotta love Peter Stella.

I actually reached out to Peter to get some thoughts, and as usual was bombarded with so much insight I felt fully ashamed of my ignorance.

For example, did you know Chile has the strictest central bank independence relationship in the world? Its mandate doesn’t even allow it to own government bonds.

Julian Rimmer10:47It’s common knowledge in our house

Izabella Kaminska10:48Peter’s other idea is that cbanks like the Czech Republic and Riksbank quite like losses because as long as they’re in negative equity they can’t be forced to join the euro.

It’s also a tidy way to get going with quantitative tightening without having to stress the market out in terms of processing large amounts of supply.

But for now, let’s quickly move on to some other news.

Julian, how’s the week been?

Julian Rimmer10:51Well, busier in markets than it has been in the wine shop. I was able to listen to three whole podcasts yesterday afternoon without a solitary interruption from these things they call customers elsewhere but blue moons in the Kew wine shop.

I have a busy week lined up next but it’s nowhere near as busy as the Australian PM’s.

Anthony Albanese, Aussie PM, is on his way to China for a prickly dialogue with President Xi. Xi will of course flash that beatific but wholly insincere smile when they meet during the visit scheduled 4-7 in Shanghai and Beijing.

Have you ever been to China, Izzy?

Izabella Kaminska10:52No I have not sadly. My parents went to see the Three Gorges Dam, but not me.

Their main feedback was that the food was nothing like you get in Soho.

Julian Rimmer10:52For many years, I took Larkin’s approach, ‘I’d like to go to China if I could come back the same day’

But I did visit in 2012 eventually, spent 48 hrs in the French quarter, ate tapas and listened to jazz and didn’t see anything of China

However

Albanese finds himself batting on a sticky wicket.

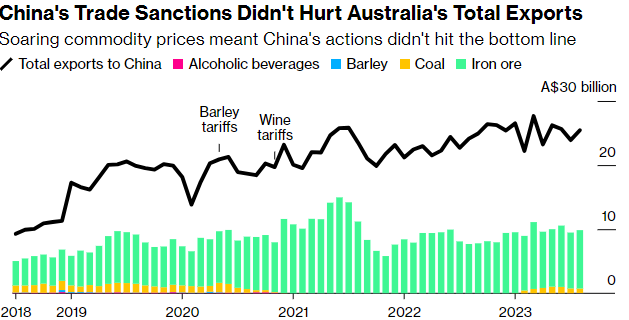

A quarter of Australia’s exports travel to China but cultural and political differences between the two countries are pronounced and likely only to be accentuated for all the faux bonhomie that will no doubt be on display for the cameras.

Reasons for disagreement are legion: Poor behaviour from the Chinese in the South China Sea, Chinese political interference in Aus, the imprisonment of an Aussie journalist in China, the Aussies’ demand for an investigation into the origin of Covid-19, which had nothing at all to do with people eating Wuhan batshit crazy soup or pangolin carpaccio, that problematic thing about freedom of speech etc etc

But there is always room for trade talks and even with all the argy-bargy of the last few years, Australian exports have barely been dented:

The ban on Aussie wine was a boon for Kiwi wine producers which is one of the reasons belly wash Kiwi sauvignon blanc became so expensive in the last few years.

But they (aussie exports) have become more complicated. Aussies will want the restrictions in wine exports lifted, the Chinese will demand access to investment in the other’s mineral industries.

The Aussie dollar, a pro-cyclical currency if ever there were, has been depreciating for a decade now but some favourable optics next week and the probability of a 25bp hike from the RBA next Tues, some of the pressures on AUD should start to alleviate.

CPI peaked ~6^ in 2Q23 and should halve by the end of 2024.

I like a trading long in AUD

Izabella Kaminska10:58I love Australia, but I feel having been privy to a private audience with XXXXXXXXX, there’s only so much more Australia I can take.

Julian Rimmer10:58That’s very ambiguous

That will leave the punters wondering

Moving onto terra cognita.

Izabella Kaminska10:59What’s the market situation today?

Julian Rimmer11:00@johnkingston – I love Antinori wines but they are priced accordingly. Izzy was drinking one on her holiday last week as I recall

mkts… 3Q earnings season threw up some strange performances. In the US they were generally stronger than analysts were expecting

But it appears margin resiliency was the key with many sectors struggling to generate top-line growth, as one might imagine given interest rates and inflation

Izabella Kaminska11:00What about actual markets?

Julian Rimmer11:00Revenue guidance for 2024 could still be characterised as conservative which is why equities struggled so much in the month of October.

The S&P, as of last Friday, had conceded 10% which qualifies as an authentic ‘correction’.

November, however, has been altogether a tiger of a different stripe with markets very keen to discount what is perceived as the end of the rates cycle for the biggest central banks.

UST10YR holding 5% was the Rorke’s Drift of bond market battles last week.

Albert Edwards makes a good point (a locution I’m not fond of) this week:

Izabella Kaminska11:02( Julian is not a fan)

Julian Rimmer11:02(i’m sure Albert would be thrilled to know I thought he made a good point)

‘from August onward US treasuries have faced increased competition from higher JGBs yields. That pressure intensified at exactly the same time as it became apparent just how gargantuan US Treasury issuance had become’.

Someone should tell Janet Yellen.

(or Anne Widdecombe. This image from yesterday still troubles me)

I saw that on my bedroom ceiling last night and it made for a difficult night. As ubs put it:

For equities lower yields reduce the headwind faced by longer-duration equities—whose valuations are more reliant on profits further out into the future.

I couldn’t have put it better myself.

That’s not a figure of speech. I really couldn’t have put it better myself.

Last week, we wrote about how positioning was favourable, US data were surprisingly encouraging, share buybacks were now a pillar of support with the reporting season ending and the seasonality effect of Nov and Dec tended to be helpful.

(I say we wrote, I mean I read and then set it down here).

Izabella Kaminska11:05Is that the guy from Goldman?

Julian Rimmer11:05Yes, Pasquariello

All this is playing out thus far but this embryonic rally is less than a high-conviction at this point and a bad data point or a scary inflation reading would reverse sentiment in short order.

Non-farm payrolls data comes an hour earlier than normal today which scuppered my client lunch plans at least once a year.

Izabella Kaminska11:06Did you only go for lunch once a year?

Julian Rimmer11:06I was three times a week regular as clockwork but this particular Friday’s lunch plans were always complicated by the clocks.

– when I was in the City

– and when I had clients

– and when entertainment on expenses was still yet to be considered a financial crime.

Consensus is around 180k and the markets’ interpretation of this will decide whether this nascent rally is nipped in the bud or develops the Big MoMo.

If the markets, like a Meta avatar this year, develop legs. Where should the punter be placing his chips?

The unloved number among them REITS, banks, retail, China, small cap.

It’s worth noting that while the S&P doesn’t look overly compelling at 17x PE 2024 (e) but if we strip out the Magnificent Seven it’s more like 15x for the remaining, erm 70% of the mkt.

Michael Hartnett’s asset return quilt, something I find strangely mesmeric, gives an excellent pictorial guide and to what’s been most out of favour:

You ever made a quilt, Izzy?

Izabella Kaminska11:10no

Julian Rimmer11:10Well, you have some work to do if you want to realize your dream of being a housewife

Izabella Kaminska11:10but I know some Americans who enjoy the pastime.

Julian Rimmer11:11Don’t worry – we aren’t going down another AI rabbit-hole this morning but UBS advise the following:

‘Within equities, given recent selling pressure on the tech sector, we think investors considering adding exposure can look to beaten-down AI beneficiaries, such as select global semiconductor stocks. Recent tech results confirmed robust AI infrastructure spending ahead and support our expectation for a sharp recovery in revenue next year. With AI demand broadening, we continue to like mid-cycle tech segments like software and internet: We anticipate new AI-enhanced productivity tools, such as co-pilots or generative design tools, will drive adoption in the coming quarters and boost direct AI revenue. ‘

UBS still see a ‘positive return outlook for stocks over the coming 6-12 months, supported by a softish landing for the US economy along with our forecast for a 9% rise in earnings per share for S&P 500 companies in 2024’

It sounds relatively pedestrian, doesnt it?

But I still see problems for companies growing sales.

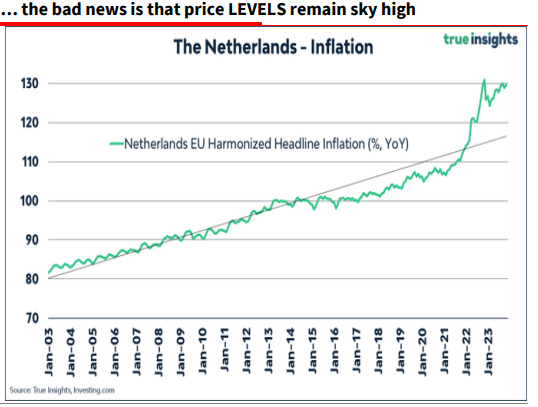

Albert Edwards’ weekly spotted that headline inflation in Belgium and the Netherlands (see chart below). Both saw headline CPI move into deflation (down to -1.7% and -1.0% yoy respectively) as high energy costs unwound. Although core CPI inflation remains sticky in both countries, it is notable that this pace of decline in the headline CPI has rarely ever been seen’

He notes while CPI is falling, price levels remain very high

This is something everyone intuitively understands when they go to a supermarket.

Of course, I understand most viewers here this morning never enter a supermarket and avail themselves of Ocado or Harrods home delivery – or if they do degrade themselves by entering a Waitrose they walk round with several trolleys and simply sweep whole shelves of luxury goods into their cargo with nary a thought for the prices or the offers in the shit bin at the end of the aisle.

Izabella Kaminska11:15***** BANK RESERVE NEWS FLASH*****

HAUSER HAS SPOKEN!

Julian Rimmer11:17

Julian Rimmer11:17‘calibrate boe liquidity toolkit’ jumps out at me

Izabella Kaminska11:18Ok sorry for all that FLASH on your eyes.

But this is important stuff!

Julian Rimmer11:18It’s like reading a tweet from donald trump

Izabella Kaminska11:18Not least because it emulates … sorry to be annoying… a lot of the stuff we’ve been focusing on.

Julian Rimmer11:18Of course, it does.

Izabella Kaminska11:18Anyway, haven’t read the full speech yet, but here it is:

Central banks today face many challenges – but three of the biggest are:

• First, how to judge where central bank balance sheets should settle in the medium

term as monetary policy makers return inflation – which remains far too high – to

target, through a combination of higher interest rates and unwinding Quantitative

Easing (QE) and other ‘unconventional’ policy interventions;• Second, on the micro-prudential side, how to ensure that banks’ liquidity

insurance remains appropriate as technological change increases the risk of larger

and faster deposit runs, of the kind seen this Spring in the US; and• Third, on the macro-prudential side, how to ensure the stability of the financial

system as a whole in the face of the growing incidence of systemic liquidity shocks,

not just in banks but increasingly in non-bank market finance too.

Julian Rimmer11:19My experience of daily, lived reality validates everything you say

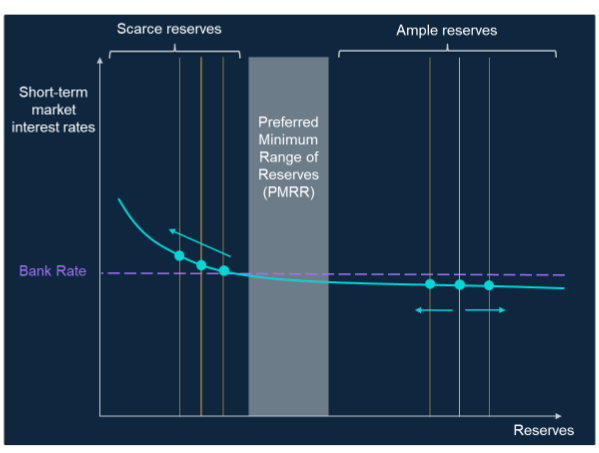

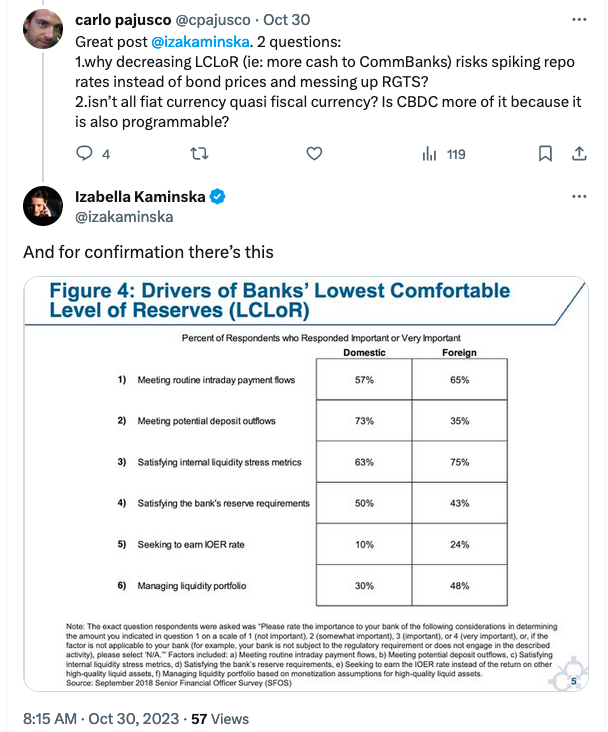

Izabella Kaminska11:19You will recall that we discussed the “lowest comfortable level of reserves” constraint last week. I hope.

That’s very much a Fed term. The BoE, via Hauser’s speech (at least this is the first time I’ve heard it referenced this way) has of course coined its own equivalent.

‘Preferred Minimum Range of Reserves’

Aka – yes another acronym – PMRR

Julian Rimmer11:20PMROR not catchy

Izabella Kaminska11:20

So, I don’t want to pre-empt as haven’t properly read, but based on those flashes and this bit that I CTRL F-ed it sounds like they are preparing the market for the realization that some extended balance sheet will be with us for longer.

Because the system (in a RTGS world) needs that extra liquidity

Not to accuse Hauser of plagiarism or anything.. but I can’t help notice this point is kinda similar to my lovely tweet thread from last week.

Julian Rimmer11:22I think you just did

Izabella Kaminska11:22More of a mind meld. But Here’s my Tweet thread FYI

11:22

11:22

Specifically this tweet:

11:23)Actually here’s the screenshot

And this is from Hauser’s speech. Different conclusions tho.

Julian Rimmer11:26Just while Izzy consults the Bodleian library to answer Robert’s question, I wanted to make one final point on equity markets and the likely direction of travel before we close.

Merrill’s proprietary trading Bull & Bear indicator gives a contrarian buy signal for the 3rd week running and it’s noteworthy that among BAML’s private clients, a pretty decent representation of retail trends generally, equity holdings at 58% of total assets are at their lowest since March 2020.

And back to banker talk

Izabella Kaminska11:27No I think that’s it from me. I have to actually read the paper before accusing people of plagiarism.

Julian Rimmer11:27one final Q, Izzy, did Elon make it into the Arc?

(I guess there’s only one of him)

Izabella Kaminska11:28No, he did not.

Sadly for us.

But he did make it to Bletchley. I hope you have fully digested his interview with Rishi?

Julian Rimmer11:29I will watch that in its entirety this afternoon when not selling wine to the good but impoverished burghers of Kew.

But i did see this one memorable quote and it’s my favourite of the week:

“The pair discussed the potential benefits of AI, with Mr Musk saying: “One of my sons has trouble making friends and an AI friend would be great for him.”

What about you, Elon? Do you struggle making friends?

Was the question Rishi didn’t ask.

Izabella Kaminska11:31Anyway, I think that’s us coming to an end now.

Julian Rimmer11:31yes, cleaning team: we have a spillage in aisle 7.

Izabella Kaminska11:31Thanks everyone for coming over. And just one operational note.

Next week Julian is indulging in off-site activities of a personal nature on Tuesday and Wednesday, so sadly, we will close the show for those two days. But fear not he will be back!

Julian Rimmer11:31Tempus tacendi.

Izabella Kaminska11:31Ciao everyone.

One Response