Anjuli Davies11:00

Anjuli Davies11:00Good morning SMLers

and good morning Frances

11:01Markets seem to be treading water this morning

in the build up to the debt ceiling deadline

FRANCES COPPOLA11:01

FRANCES COPPOLA11:01Morning everyone

Anjuli Davies11:01

Nervous

Anjuli Davies11:03All the investment banks have their “war rooms” up and running

But I don’t think anyone can really fully predict what might be…

Lots of chatter about what might happen

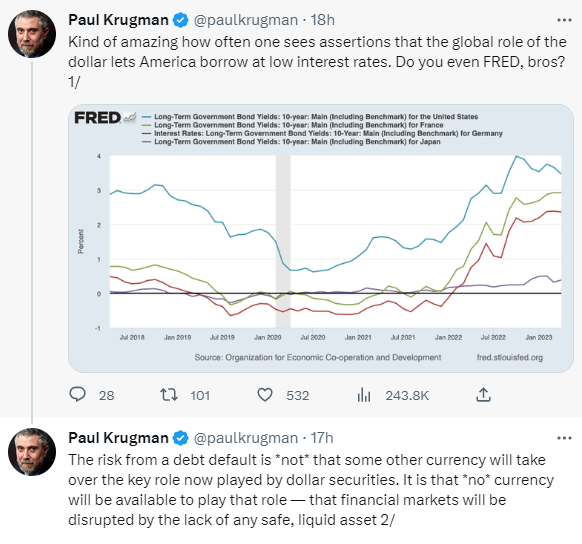

Krugman weighed in yesterday

Anjuli Davies11:03Are you optimistic Frances?

I think there will be a deal. But I’m not as confident as I was the last two times the GOP played debt ceiling roulette with a Democratic president. There are some very crazy elements in the GOP these days.

Anjuli Davies11:04

Krugman’s point here is key. A US debt default would be a systemic shock similar to Nixon’s suspension of gold convertibility in 1971.

Indeed US goldbugs see 1971 as a default. As do the French, I believe.

as I recall they were all for sending gunboats to retrieve the gold the US owed them

Anjuli Davies11:06WE should really bring back Kathleen Tyson to talk again about multipolarity…

Indeed, it is the subject du jour…

3-month USTs would no longer be “risk-free assets”. There wouldn’t be a risk-free asset in the system any more.

11:10That would do terrible things not only to the cost of market funding for banks and FIs (it would be a considerable monetary tightening) but also to benchmark rates more generally

Anjuli Davies11:10

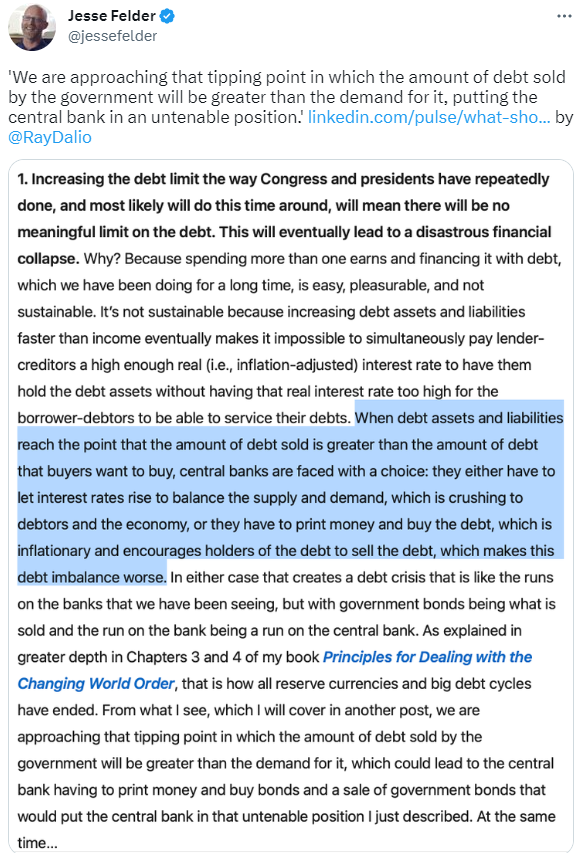

Ray Dalio has some opinions

He raises the issue of endlessly raising the ceiling until the ceiling becomes meaningless

The ceiling is already meaningless

Anjuli Davies11:11But i mean this is not a new discussion

What he really wants is fiscal austerity. Which maybe is something the US needs, but playing chicken with the debt ceiling really isn’t a good way of doing it.

We’ve played this game twice before, and each time the price eventually was a degree of fiscal austerity.

Anjuli Davies11:13What’s the carrot and stick this time?

Cut spending the GOP doesn’t like, and maybe reduce taxes for people the GOP does like. But the GOP is increasingly involved in culture wars, so I think there might be another price too – maybe federal restrictions on access to abortion.

11:16Even if there is no default, these repeated debt ceiling games weaken the credibility of the US government.

11:17US domestic politics is putting at risk the stability of the international financial system. Would hardly be surprising if people didn’t start looking for (and perhaps creating) alternative “safe assets”.

Anjuli Davies11:17But what is the alternative….?

that’s the million dollar question

@darren yes, and also via higher maternal morbidity. There’s already a spate of awful stories from states where abortion bans have been introduced – women being denied essential healthcare because of fears about litigation.

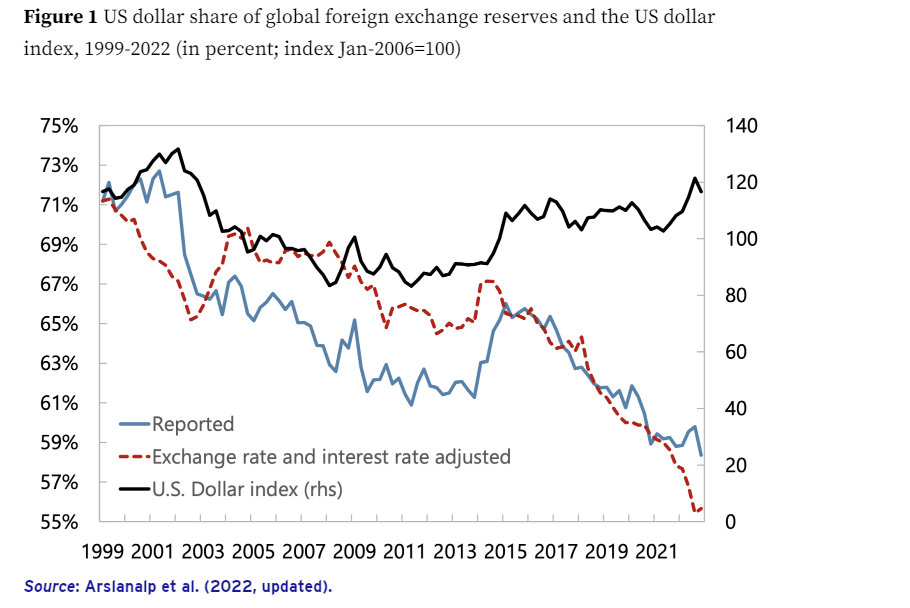

Anjuli Davies11:19Is de-dollarisation happening by Barry Eichengreen

he of course wrote some books on this

Are we in Zoltan territory? Pivot to commodity-based currencies in the East?

We are witnessing the birth of Bretton Woods III – a new world (monetary) order centered around commodity-based currencies in the East that will likely weaken the Eurodollar system and also contribute to inflationary forces in the West.

Anjuli Davies11:22

In a note published earlier, Zoltan wrote this crisis is not like anything we have seen since President Nixon took the U.S. dollar off gold in 1971 – the end of the era of commodity-based money. When this crisis is over, the U.S. dollar should be much weaker. From the Bretton Woods era backed by gold bullion, to Bretton Woods II backed by inside money (Treasuries with un-hedgeable confiscation risks), to Bretton Woods III backed by outside money (gold bullion and other commodities), Zoltan believes the global monetary system will never be the same post the crisis.

Anjuli Davies11:23We need Zoltan to come on here

That would be good!

@robert I believe it’s at the Fed’s discretion. But wouldn’t that just be another backdoor form of debt monetization?

Zoltan and Kathleen double act would be awesome

Anyway, moving on… if we can

Anjuli Davies11:26Yes, let’s

Robert and Darren, wouldn’t the Fed accepting defaulted debt be equivalent to the Fed accepting debt at face value instead of fair value – which it is already doing?

11:28So, Andy Verity’s book on Libor rigging is now out. It basically says central bankers and governments conspired to rig Libor during the GFC, starting with the ABCP market freeze in August 2007 after BNP Paribas closed its funds.

Anjuli Davies11:28links above – it’s being serialised in The Times

Libor rigging was later declared unlawful and some traders were sent to prison. But the senior bankers, central bankers and politicians got off scot free for doing essentially the same thing.

11:31The former Chair of the Treasury Select Committee, Andrew Tyrie, says that Parliament may have been misled, which is a serious matter. There will be questions in Parliament about this. But it’s not just the Bank of England involved.

@Graham it’s the same thing

Basically central banks were trying to stabilise a market panic by rigging benchmark rates across the board

Which is perhaps understandable but totally destroys the whole point of an independent benchmark

You may recall it wasn’t just Libor that was rigged.

Anjuli Davies11:34Some people (on twitter) are disputing if this is “new ” news – can you explain the difference between what we already knew and the latest revelations

@Helmholz I am no fan of the new indices. I would point out though that because bank funding has largely moved to the repo market, Libor had to be replaced anyway, not because it was open to rigging but because the unsecured interbank market is too thin to establish any sort of realistic rate

Izabella Kaminska11:36

Izabella Kaminska11:36Let me jump in to explain the dif

It’s a bit like Credit Suisse’s unsecured funding, Anjuli. It’s not news, but it is NEWS, if you see what I mean. And imo the real issue is the mammoth injustice of prosecuting junior traders when senior bankers, central bankers and governments were conspiring to do the exact same thing, even if for good reasons.

Anjuli Davies11:36

11:37Great miscarriage of justice

Izabella Kaminska11:38So, we’ve known the BoE was guiding the rates lower. The question is were they putting pressure in such a way that it was an order. The really shocking case is that of Peter Johnson, who was told from on high by Mark Dearlove (nephew of former MI6 boss Richard Dearlove) to lower the rates or else. He knew the rates were bullshit, so objected massively. He also whistleblew. Didn’t stop him going to jail. Albeit for commercial-interest related manipulation.

My view is that market rates were not credible at the time anyway, so central banks stepping in to set benchmark rates made sense. But they didn’t have the legal authority to do so. So they did it by the back door.

Anjuli Davies11:38Nineteen traders have been convicted and nine jailed because of court rulings that outlawed any influence on Libor apart from the interest rates on offer on the money markets at which a bank could borrow and lend cash

Izabella Kaminska11:38Verity got the full internal phone calls over a year ago, and published the Lowball tapes as a podcast in March 2022. Unfortunately the whole thing was drowned out by Putin.

he’s been investigating this for best part of a decade

Izabella Kaminska11:38But the new stuff this week is related to the testimonials PJ gave to the FBI and FSA.

And this allegedly shows global coordination by cbanks.

Anjuli Davies11:39I’ve been contacted by someone who worked with Peter Johnson at the time and he says he was a great guy, full of integrity and that he was massively scapegoated

@Graham yes, there were very good reasons for explicitly setting benchmark rates at that time. But because it was done by the back door, we still don’t have a mechanism for central banks to explicitly set benchmark rates in a market panic.

Izabella Kaminska11:40And btw, even Tom Hayes, when I”ve spoken to him, has expressed sympathy for the idea that cbanks had to act. And in dire circumstances they probably do have a mandate to lie. The issue is that rather than come clean and risk showing the rates markets wasn’t to be trusted (as it was being overly influenced by cbank intervention and control), they decided to deflect by scapegoating lower level traders.

That’s the issue.

Exactly this.

Izabella Kaminska11:41So for me the big question is at what point does the cbank’s license to lie kick in? It’s tricky.

Because if they are overt about having a mandate to lie, nobody will ever trust them.

it’s like with state disinformation more broadly

It’s “whatever it takes”, Izzy

Izabella Kaminska11:42Even Orwell says sometimes it’s justified, in war, to lie.

the issue is whether in a democracy and a supposed free market, the people have a right to know they are being lied to

Because it takes us into this territory:

“The rules are simple: they lie to us, we know they’re lying, they know we know they’re lying, but they keep lying to us, and we keep pretending to believe them.”

If people believe that central banks will do “whatever it takes” to maintain price and/or financial stability, and are happy for them to do so, central banks can lie.

Anjuli Davies11:43But they can’t scapegoat the people they use

Izabella Kaminska11:43exactly

But the risk is that at some point, people collectively decide they are no longer happy for central banks to do “whatever it takes”. That would spark the mother of all runs on the system.

I agree, Anjuli. Scapegoating the people they used is wrong.

11:45If you want to hear Tom Hayes’ side of the story, you can listen to my Leaked Lunch with him here: https://twitter.com/izakaminska/status/1660467963839774727

Izabella Kaminska11:45

Izabella Kaminska11:45Am interested what others think about the boundaries for central bank lies.

<On that note over and out>

Anjuli Davies11:46Aren’t we being lied to a lot of the time?

@Darren that’s brilliant

A bit like wouldn’t we all be vegetarians if we had to kill our own feed

11:47What else have we been looking at this morning ? I’d like to know a bit more about Antigua News

Say more?

Anjuli Davies11:48They’ve had some amazing scoops in the last few days on Credit Suisse

Aha

Anjuli Davies11:48They got hold of some documents

Credit Suisse privately challenged Finma’s AT1 writedown

It’s making waves this morning

and Reuters:

Along the lines of what we were talking about above – how far can central banks go

LONDON, May 18 (Reuters) – Credit Suisse (CSGN.S) came close to falling below minimum levels of cash held at the Swiss central bank days before its forced takeover by UBS (UBSG.S), a regulatory document shows.

As of mid-March 2023, Credit Suisse barely reached its internal cash limit at the Swiss National Bank. A breach indicates a risk that the bank will not be able to make payments properly, Swiss financial regulator FINMA wrote in the German-language decree, which has not previously been disclosed.

Credit Suisse employees are preparing to sue Finma because their bonuses were linked to At1 bonds. $400m at issue.

Both issues first reported in Antigua News

11:52

Credit Suisse directly disputed the Swiss financial regulator’s basis for writing down $17bn of its additional tier 1 bonds, in a private letter aimed at sparing staff bonuses that were tied to the debt. Investors representing at least $4.5bn of wiped-out Credit Suisse AT1 bonds filed a lawsuit against Finma last month, seeking to overturn the Swiss regulator’s cancellation of their holdings that was imposed as part of the bank’s shotgun marriage to UBS two months ago.

The aggrieved bondholders earlier this month forced Finma to hand over a decree it had issued to Credit Suisse on March 19 — the day the UBS merger was struck — ordering the bank to write down the AT1 bonds.

The second decree refers to a letter Credit Suisse sent to Finma on March 20 arguing that the contractual conditions had not been met for a writedown, stating: “[Credit Suisse Group] further argues that no contractual ‘viability event’ occurred because the state support did not have a capitalising effect.”

Also CHF 200bn of liquidity support from SNB, half of it unsecured and backed by a federal default guarantee (ie the Swiss taxpayer), flew under the radar. To be fair it was announced at the time, but I think everyone was too busy unpicking the deal to notice what the SNB was up to.

Both banks have unrestricted access to the SNB’s existing facilities, through which they can obtain liquidity from the SNB in accordance with the ‘Guidelines on monetary policy instruments’.

“In addition, and based on the Federal Council’s Emergency Ordinance, Credit Suisse and UBS can obtain a liquidity assistance loan with privileged creditor status in bankruptcy for a total amount of up to CHF 100 billion.

“Furthermore, and based on the Federal Council’s Emergency Ordinance, the SNB can grant Credit Suisse a liquidity assistance loan of up to CHF 100 billion backed by a federal default guarantee. The structure of the loan is based on the Public Liquidity Backstop (PLB), the key parameters of which were already decided by the Federal Council in 2022.”

Anjuli Davies11:58We are nearly out of time, anything else to add Frances?

Anat Admati, Martin Hellwig and Richard Portas are calling for higher capital requirements for banks – again.

11:59After the GFC, Admati and Hellwig wrote a book called “The Bankers’ New Clothes” in which they argued that banks should have similar capital levels to corporations – around 20-25%. They make the same argument now in a piece from CEPR.

Today, policymakers, lobbyists, and commentators seem to miss the obvious lesson: ignoring insolvencies while also insuring deposits can lead to disastrous outcomes. The Federal Reserve is now providing liquidity support without restoring solvency, prolonging the agony and encouraging some banks to start gambling for resurrection as the S&Ls did in the 1980s. Expanding deposit insurance without eliminating zombies is similarly problematic. If bailouts of uninsured depositors continue, the extra levies on the banking industry to cover losses to the insurance fund may harm the viability of remaining banks.”

Anjuli Davies12:00Do you have a link?

https://cepr.org/voxeu/columns/when-will-they-ever-learn-us-banking-crisis-2023

Anjuli Davies12:01Thanks Frances

Their proposals, which they say should have been done long ago:

· Apply mark-to-market or fair-value accounting to all assets; abandon the fiction that changes in fair values of HTM assets are irrelevant.

· Stop compartmentalising risks – recognise correlations among different risks that arise from common dependence on macro developments such as changes in interest rates affecting fair values of assets as well as the scope and conditions for rolling over short-term liabilities.

· Strengthen supervision under Pillar 2 of the Basel Accord, which asks supervisors to consider the professionalism of bankers. The extent of maturity transformation at SVB was unprofessional. Supervisors should have interfered much more actively early on.

· Raise equity requirements to enable banks to withstand fair-value losses on all assets when interest rates rise. If SVB had been subject to a 20% equity requirement, its losses would have been borne by shareholders rather than falling on the FDIC.

Groundhog day in banking. And that’s all from me for today!

Anjuli Davies12:02Indeed!

Thanks everyone, see you next week

Bye for now!