Good morning, Aloha and greetings fellow market wizards

Nunc tempus loquendi

This morning, I am once again joined by our geopolitical Zoomer, Dario

The Zoomer types, writes and thinks quickly, deftly, lightly switching from one subject to another with no more forethought than a swallow taking off for the telegraph pole on the other side of the road.

Boomer meanwhile, sits here in Northern darkness, imagine Vulcan hammering away in his forge, bashing his keyboard, fury concentrated on the unmalleable reality around him

morning Dario

Morning Julian

Forethought? I hope to have no thoughts at all.

Seems like this is the safest place to be these days:

Two unfortunate incidents to relate from this weekend.

I shortchanged a woman who came into the shop to buy a bottle of bellywash sauvignon blanc.

I realised later and, knowing she worked in a cafe owned by her father a few doors away, I thought I’d do the right thing and keep the 40p for myself

I mean return it to her.

There were several women behind the counter and I asked if they knew the girl, ‘her dad owns this place, I think’. An older woman stepped forward…

‘That’s my daughter, very kind of you, so nice. Where are you from?’

As soon as I said the wine shop, the smiles stopped suddenly. Awkward silence. Big scowl. ‘She’s a recovering alcoholic. Don’t serve her again.’ The door slammed behind me.

That sounds like a very Julian incident to happen

And very briefly

The other one

I was invited to Christmas drinks by a friend’s wife.

I said I was so busy and I was most likely going to be in panto at Christmas

Cue several hours of silence – then a solitary ‘?’ from here.

I looked at the last message

The predictive text had inserted ‘panties’

instead of panto.

anyway…

Moving slowly along

Market miscellany!

Ok, we have US CPI due Tues 3.3% (e) vs 3.7% last time out

UK wage data Tuies and cpi weds a

and of course, Joe meets Xi on Weds in San Fran as we discussed in detail last week

And San Fran was predictably cleared of the homeless for the occasion

https://www.nbcbayarea.com/news/local/san-francisco/homeless-people-apec-summit-san-francisco/3363390/#:~:text=5%3A12%20pm-,Crews%20clear%20out%20homeless%20people%20ahead%20of%20APEC%20summit%20in,Damian%20Trujillo%20reports.

It turns out they’ve always been able to do

Reminds me of our old Marbella mayor who recently died after a long stint in prison’s solution for the homeless problem: buying them one-way tickets to the Canaries

(And it ‘worked’!)

Another miscellaneous item is that you should buy puts on airline companies (please don’t listen to my advice ever)

“”The head of the national police force (…) has declared a state of emergency for civil defence due to intense seismic activity in Sundhnjukagigar, north of Grindavik,” the civil defence authority said in a statement late Friday.

“The earthquakes may become more significant” and “this series of events could lead to an eruption”, the administration warned.”

Good question will:

The rating agency Moodys pointed to rising risks – rising fiscal deficits amidst higher interest rates without policy measures to reduce govt spending or increase revenues leading to the decision on lowering outlook for US economy

Some angered bulls have posted their annoyance that the new outlook came after the SPY’s consistent gains over the last two weeks

What do you think Julian?

Well, I find this to be a statement of the bleeding obvious

Ratings agencies, always, almost by their very definition, are behind the curve.

The reasons they cite are the very reasons why the UST10YR went to 5.2%

I don’t listen to ratings agencies since I watched The Big Short

But then, I don’t listen generally

The last time a major eruption occurred in Iceland in 2010 it caused widespread disruption to the entire airline industry

Speaking of things flying in the air

Yes, the Dubai Air Show this week: big order in the offing for Boeing from Emirates for 777X widebody. Turkish Airlines go even bigger with a deal to be signed for about 350 Airbus SE aircraft. China may suspend a freeze on Boeing 737 Max purchases when Joe and Xi meet this week

More concerning perhaps is the cosy consensus developing on inflation,

and the taming thereof.

We are about to enter that part of the year where all IBs produce their glossy 2024 outlooks

MS first off the cab rank

MS suggests inflation has peaked, ‘but the last mile to target will take a period of subpar growth’. Growth stepped down in 2023, and should be slower at just under 3% for 2024 and 2025. DM growth is broadly soft, while the picture in EM is mixed.’

the main risks cited are the US and China, funnily enough: stating the bleeding obvious

In our downside scenario, a more material slowdown in China leads to weaker growth and inflation in Europe. We think that ECB´s first cut will remain in June 2024 but cuts will be more rapid and more prolonged, reaching 1.25% by end-2025. In our upside scenario, more robust activity in the US and the Fed resuming its hiking cycle would have the ECB increasing rates in June and September 2024, to 4.5%.

on the UK

the view is summarised by the following chapter headings… Growth | The past is another country:/ Inflation | Now the hard part: / Monetary policy | The darling cuts of May /Fiscal policy | Reckoning nears.

Tells you pretty much what you need to know

And speaking of a reckoning…

Ah yes, Cruella

Sounds like she’s out

After her ill-advised op-ed in the Times which called pro-Palestine protesters “hate marchers.”

Her actions have been tied to recent far-right violence with these protesters and police.

If you listen carefully you can still hear the plaintive music of The Last Post being played for Cruella Braverman.

Another alumnus of my college, who, I assume, is mightily relieved to see her career might have peaked before any further unwelcome publicity is generated.

(she’s still doing better than this alumnus)

and of course, this has paved the way for the return of David Cameron, everyone’s favourite old Etonian except for all the other old Etonians.

It sounds like a policy of desperately fighting for voters by Sunak …

Don’t see how bringing ol’CamCam in will help any electoral prospects, but ho-hum.

@johnk – Punch & Judy is a demonstration of the cycle of domestic violence and abuse and of course, in our new puritanical era, it has no place in the entertainment of children.

Ahem.

That’s the way to do it.

Plaudits.

Back to MS for a moment… ‘The end of hikes and start of cuts mean high-grade bonds outperform, USD stays strong, and EM assets lag. US stocks see positive returns but risks are front-loaded. With markets pricing in a smooth macro transition, there`s little room for error.”

It’s that last part of the sentence that’s troubling.

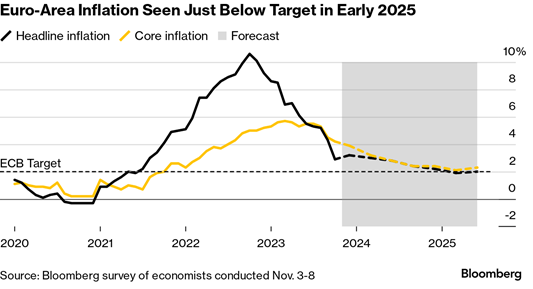

As consensus develops for tamed inflation beating a hasty retreat to central bank targets of ~2% – the risk is that inflation surprises to the upside.

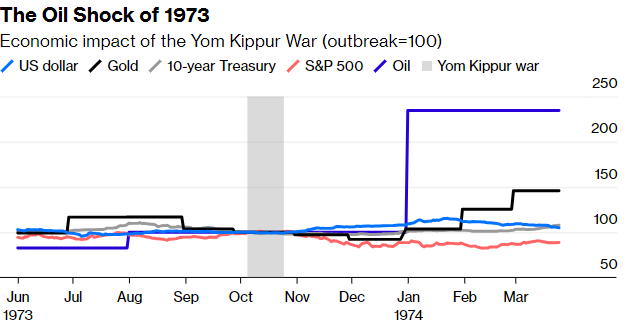

This was a central feature of Niall Ferguson’s latest oped for Bloomberg

In which he opines ‘This complacency is surely delusional… The economic consequences of wars are a topic I’ve devoted a significant part of my career to thinking about. Takeaway No. 1 is that big wars are inflationary. You don’t want to own bonds, especially not those issued by the losing side.’

He points out that the impact of wars in the ME has generally been modest,

Except, that is, for the big one after the Yom Kippur War of 1973, which was the biggest inflation shock of all.

Nonetheless, Bloomberg survey of economists believes inflation will be back at or below target by 2025:

But look at Ferguson’s chart on CPI shocks:

It’s all a question of whether Gaza is contained or escalates.

That’s still very much up in the air. But Narsallah’s comments over the last week suggested he won’t move a real finger for Gaza. Containment is more likely for now.

But the Israeli war cabinet seems on another wavelength. It turns out everyone but Netanyahu is in favour of opening a second front in Lebanon. What kind of barmy situation are we in where Netanyahu seems the moderate candidate?

So, as we head into the last 6 weeks of the year what direction do markets take?

Well, it depends on which one. US, as always, looks best

US mega-cap stocks are pushing up against resistance levels, at which they have tried and tilted on several occasions:

Given mkt dynamics are unlikely to change between here and year-end (the Fed is done, the US economy is chugging along easily enough), fund positioning and flows are positive, and seasonal factors weigh in favour… it would be radical to dismount from the mega-cap nag at this stage

Powell needs to talk down the mkts and inject some volatility into the long-end to prevent complacency setting in and FCI loosening too much, but generally, the direction of travel for the S&P looks higher overall

A breakout for the Big 7 around Black Friday would definitely provide the mkt with some oomph.

Don’t fight the trend just yet. technicals and positioning still on your side as FOMO grows.

The Barclay’s call on Europe is quite the opposite:

European Strategy: European Factor Insights – November -> Rates relief but angst about the strength of growth contribute to yet more rotation within the market. We are still Positive on Value given better-than- market earnings momentum but also higher-for-longer yields. We stay Negative on Momentum given ongoing rotations in the market are depriving it of a trend to follow.

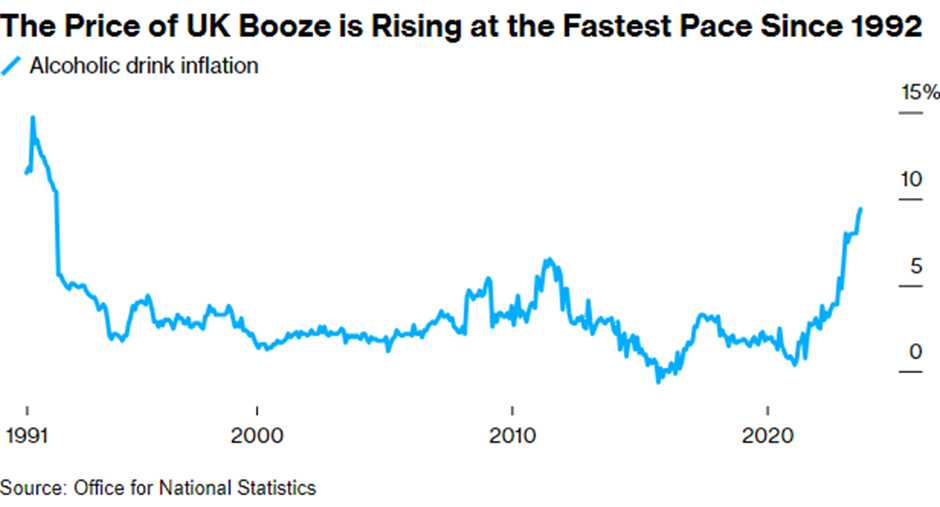

The UK’s cpi data is Weds and the BOE and Rishi will both be p[raying the number comes in below 5% – but one part of the equation which definitely isn’t – is booze inflation.

David: Not that I know much about AI, but it would make sense that the field is ultra-monopolistic. I see one company getting huge outsize gains at everyone else’s expense

Booze prices rise on higher energy costs, and higher labour costs but primarily duty.

David: I mean by the time the services actually become economically relevant, which they aren’t just yet bar a few OpenAI niggles (at least not at the level it will get to). Once AI is fully released, the push towards a general AI is by nature monopolistic because one will win out and become THE GAI, and the others won’t

@johnk – big supermarkets not included!

Speaking of inflation hitting ordinary people

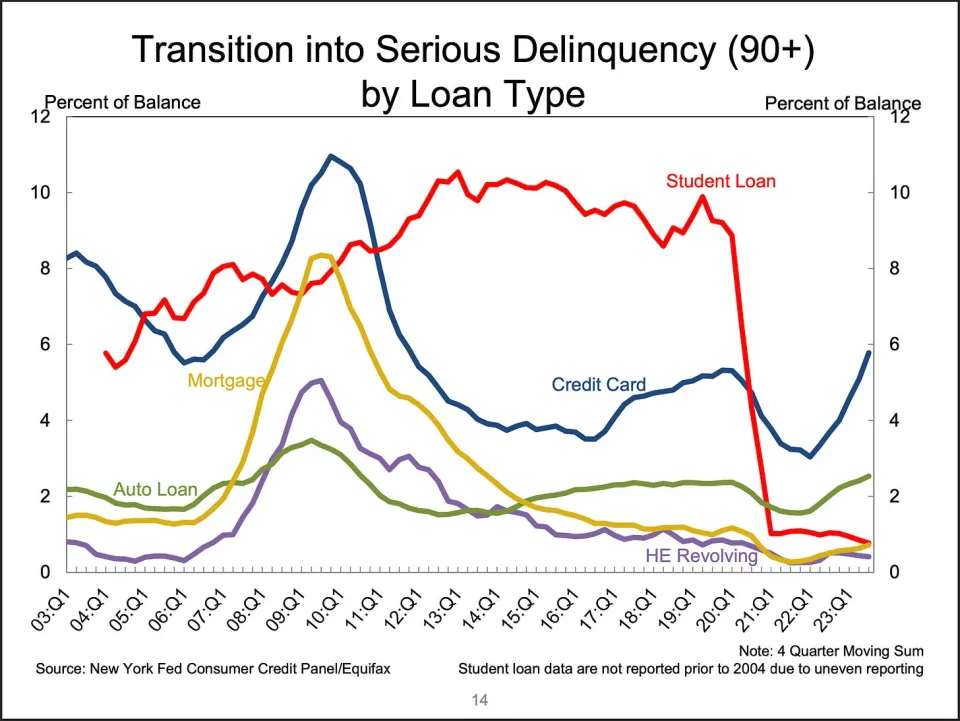

Last week we looked at the rise in CC delinquencies

Some new data is in: the share of debt newly transitioning into delinquencies are rising on mortgages, credit cards and auto loans

The source is the NY Fed Consumer Credit Panel/Equifax

But the actual “stock” of delinquencies has stayed below pre pandemic levels, despite the “flow” into new delinquencies picking up:

One thing that always gets me in these figures is the optimism that happens when the article writers can point to household wealth figures

Which (like 3.6 Roentgen) aren’t great, but they aren’t terrible either

Is that a chef?

It’s a radiologist from the show Chernobyl

Little niche joke for those of us who have watched a series in the 21st century

JR is clearly excluded from this category

Ah, I never watched it although I read the books by Nobel prize-winner Alexievitch (I might have mangled her name spelling)

I have a lot of scepticism whenever household wealth data is mentioned because it will be based on their largest asset class: property

(Now I must stress I am an economic ignoramus.)

But surely making out the health of household economies to be positive based on an asset class inflation that is largely understood to be dramatically overvalued isn’t great?

I can’t disagree with that

One related factoid worth keeping an eye on is the increasing number of cities worldwide banning short-term rentals, AirBNB style

One ‘factoid’ that won’t surprise you is that I’ve never made an AirBnB booking

The app defeated me

I phone hotels and ask for a rate!

Probably better this way Julian. AirBNBs used to be better than hotels price-wise, but now they’re just as expensive – and you need to clean up your mess yourself.

Now, the company has posted a nice operating profit this year but concerns continued growing at the viability of short-term rentals in dense cities since New York’s ban on rentals under 30 days

(I look back on some of the things I’ve done in hotels and they were simply not practicable in someone else’s apartment)

This could cause a perfect storm for housing

If Airbnb operators are forced to sell due to an inability to rent short-term amidst rising interest rates, mortgage rates and prices have priced out many would-be buyers – creating a situation with more supply and less demand, crushing prop prices.

Why are governments against AirBnB?

Same reason as me? They can’t work the app?

Um… I don’t think so

I think it is mostly about the political pain it’s causing pol parties because short-term rentals have crowded out the long-term rental market, being a significant factor in rent increases

Which are fucking gnarly

In dense cities is the key – this is where they’re getting banned

And cities which banned them immediately saw a drop in rental prices – which will pave the way for more bans

And this wouldn’t be a niche economic impact

Note that this is even close to happening yet – home prices are still rising in more than 80% of US markets.

Speaking of household economics, this week is huge for guesstimating the general health of consumers’ economic choices

We’re going to have Home Depot on Tuesday, Target on Wednesday, and Walmart on Thursday

The expectation is broadly that all three stocks are set to disappoint, as foot traffic fell in the third quarter for all three retailers. We’ll see.

Yes David, and running them badly also

Let’s have some geopolitics in an obscure part of the world, your forté, Dario

Well, Julian, I saw the spitting image of the angry old man I wish to soon become:

This American guy shot two environmentalists who were blocking a road in Panama. Funnily enough, all I saw were plaudits online

But tragically, these environmentalists were actually doing something noble and directly relevant – unlike the vast majority of asphalt-kissing bs’ers in Europe

They were protesting the loss of environmental controls for building projects near the Panama Canal

And this is something you told me Julian, it was about the lack of rainwater in the country – which is used to operate the canal

I did?

I forgot

And indeed – an unprecedented drought has been causing a buildup of traffic on the beleaguered Panama Canal

So much so that Japan’s Eneos Group made a payment of $4mn in the largest-ever bid to expedite their ship’s passage through

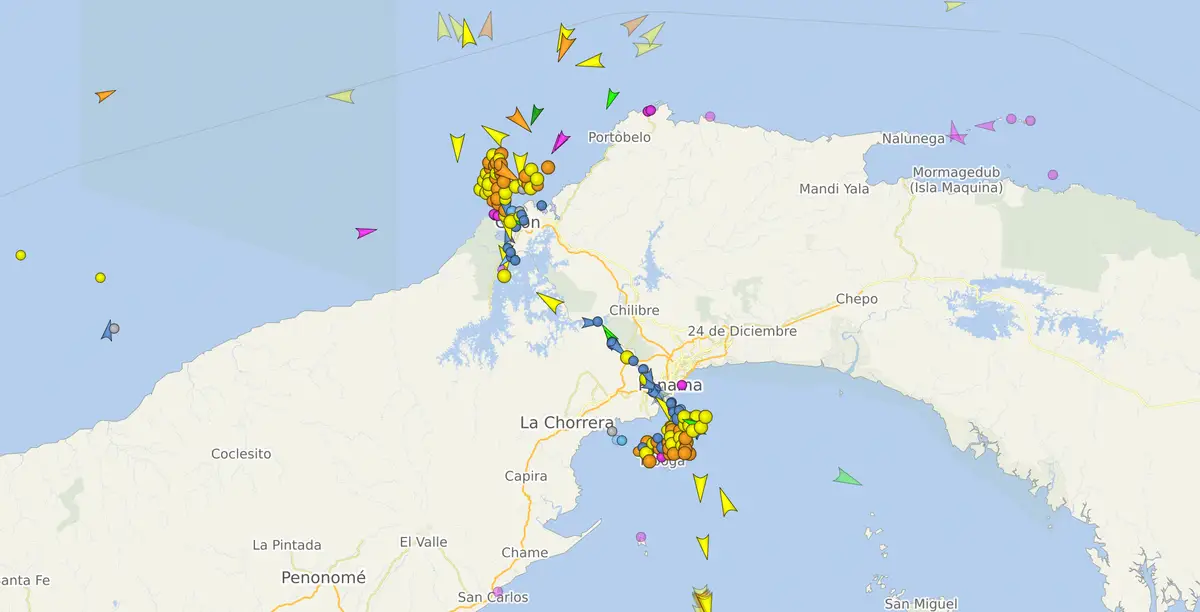

No surprises there. The canal is busy asf:

Here’s a recent traffic pic

The canal’s normal 36 daily transits for ships have been reduced to 25 a day

They will be decreased to 18 a day by Feb 2024

Why do they need fresh water? What’s wrong with seawater?

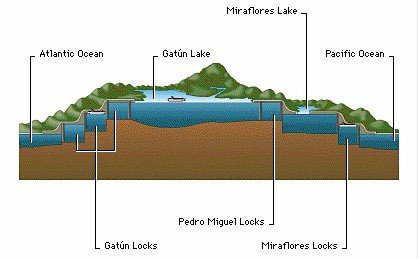

Well, that’s really interesting actually. The canal’s critical bit is the so-called Gatun Lake

The Gatun Lake is freshwater and the surrounding nature and lushness of the Panamanian jungle relies on it for nourishment

The three locks protect this freshwater from being contaminated by seawater

But freshwater itself is also used to power some of these locks – around 52 million gallons of it are required to lift a ship over Gatun Lake and back down again

A lot of these issues come since the passing of responsibility of the US on canal maintenance to Panama in 1999.

It’s a lot more complicated than digging a trench, as I thought previously.

The Panamanian’s expansion projects since then have been run on a shoe-string budget that wary locals point to as the culprit behind greater freshwater leakage and inefficiency

So complicated it bankrupted the French’s first attempt at it. But note the first attempt at the canal was by Scotsmen!

A lot of the problems are associated with the rush – fear that the Nicaraguans could beat them to the chase.

Panama is still a highly desirable destination for Brits. remember that guy who faked his own drowning while out canoeing up near Durham or somewhere?

He hid in a cupboard for two years, got the insurance payout through his wife

Then jetted off to live in Panama.

That’s amazing

So 10 years ago Nicaragua announced the megaproject – a competitor to Panama

After 10 years, dozens of environmental activist arrests and exiles, and loads of money, there’s nothing to show for it

A great saying my dad is fond of saying applies to both Spain and its former colonies. A German man tells a Spanish man – “You Spaniards, you’re so rich, you can afford to build things several times. We Germans are poor. We have to build things right the first time.”

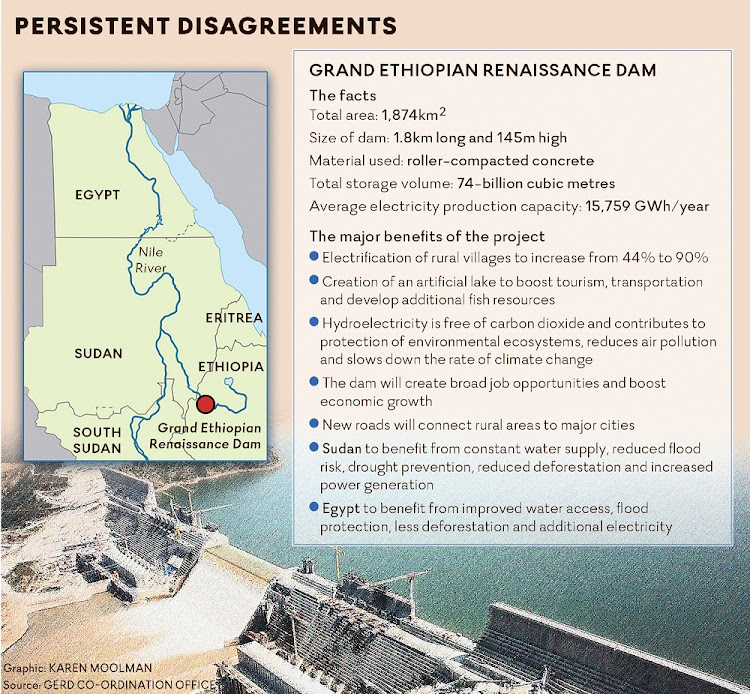

However some megaprojects do get proper funding towards completion. Unfortunately for Egypt.

The Grand Renaissance Dam of Ethiopia is inching closer to completion. The fourth filling just finished in September – to Egyptian dismay

Below is a bullish factsheet on the GERD

Is this the project that will stop all those luxury cruises down the Nile and Agatha Christie novels?

No Julian!! Read the sheet. “Egypt will benefit from improved water access,” it says. It can’t be lying can it

Never

Maybe they should get the Russians in to look after their dam…

The much-vaunted negotiations failed to reach an agreement this September.

Well funny you should say that…

No!

Not Russians invited?!?

Because they both now form a part of the BRICS.

Let’s see how they deal with that conundrum

but this ain’t the only bugbear in the Horn

Diplomatic experts have been pointing to increasing tensions with Ethiopia and Eritrea

Turns out Ethiopia wants access to the Red Sea again

On October 13, President Abiy Ahmed announced Ethiopia’s intention to create a naval base on the Red Sea – on currently Eritrean territory

This threat-laced speech brought calls by Antony Blinken who urged both countries to refrain from provocation

‘Increasing tensions between Ethiopia and Eritrea’ sounds like a tautology.

Never anything else.

I really don’t see what Blinken is getting so worked up about. He should have expected Abiy Ahmed to engage in another military invasion considering he received the Nobel Peace Prize in 2019

Now Ethiopia is amassing troops near the Eritrean border in Zalembessa – 45 miles from the port of Assab

It comes as the conflict between the Ethiopian army is increasing with the TPLF – which submerged the country in a civil war in 2020. Abiy Ahmed is also being accused of leading a dramatic escalation by scaling up military operations in the region

One way or another – the Horn is headed for a crisis; or several.

Right, cleaning team. there’s a spillage in aisle 7. Please attend.

Fare thee well a while.

Nunc tempus taciendi.