Good morning, Aloha and greetings fellow market wizards

Nunc tempus loquendi

joined once again, this grim, damp autumnal morning by our geopolitical zoomer, Dario

hola

Hola!

So, Dario, a disturbing anecdote

Do share

When I was young, my grandfather, a miserable, cranky, misanthrope if ever there were one,

would often dole out inappropriate advice – like ‘hold your grudges’

or

‘aim low, you wont be disappointed.’

But sometimes there was a nugget of sagacity in what he said

so, ‘never go to the toilet in your socks’ was one such piece of counsel to which I’ve always adhered

????

Imagine my surprise then to hear that RFK Jr, that copper-bottomed cretin running for pres.

Copper-bottom cretin.. brilliant

I object

RFK is a hero that says out loud what most people only dare whisper

That the govt’s a racket, the CIA killed his uncle, pharma lobbyists are out to get you, and that a man’s identity and trustworthiness should be based on little more than lifting very heavy weights.

@johndc77 – my grandad’s variant was ‘ dont do today what you can put off till tomorrow’

Or as we say in Spain – mañana

All steroids.

So, after that shocker let’s address the markets

The first thing on the menu this morning was UK labour data – according to Simon French of Panmure Gordon on Twitter

Steady set of U.K. labour market data – with all the sampling health warnings that come with it! Steady unemployment (4.2%), stable inactivity, modest real pay growth and vacancies (957,000) reverting towards their long term trend. Looks suspiciously like a soft landing – but difficult to be too confident given data deficiencies

The release is messy, one could construct dovish or hawkish arguments from it. What it does, more straightforwardly, is put tomorrow’s CPI data squarely in focus. That is a big number.

And speaking of CPI, haven’t we got US CPI first?

Yes, apologies for the UK-centric approach which isn’t like me at all, normally.

Yes, CPI data due today in US and 3.3% is consensus, versus 3.7% last time.

US mkts still feel like they want to travel higher and technicals/ flows are a big factor here

CTAs will be buying equities this week after SPX ended above our buy signal at 4399 (ESZ3 ref 4428) to flip long and SX5E closed yday above the 1st buy signal at 4213 (VGZ3 ref 4241) for funds to cover their shorts. We est` that CTAs will need to buy $18bn unlevered in SPX and $12bn unlevered in SX5E as a result. If we break > 4431, CTAs will move to ‘max long’ SPX and need to buy another $18bn unlevered in the mkt.

this was from Citi this morning.

What’s a CTA?

Commodity Trading Advisers

Basically, a bunch of hedge funds that trade futures or derivatives and who use quant strategies for the most part

I can assure you, that was not an investor base I called in my days as a sales trader.

Speaking of investing

I remember one of the first investment pieces of advice I received was from my A-Level econ teacher on the back of the Royal Mail privatisation

And on how it would make Royal Mail even better

I remember that privatisation because it made Vince Cable look like a fool

So we had news this morning that Britain’s Ofcom is to fine Royal Mail, owned by International Distribution Services, £5.6mn over a failure to meet its own delivery targets last year

“Royal Mail has struggled with falling demand for parcel deliveries as hard-pressed consumers cut spending and as a surge in online shopping during the Covid-19 pandemic has faded. The pandemic also gave rise to serious operational challenges, as a result of the need for social distancing at local mail centres and delivery offices and high levels of Covid-related worker absences.”

“The business swung to a £1 billion ($1.2 billion) loss for the year through March 2023 after it was also hit by strikes. Royal Mail’s workforce has shrunk by 10,000 over the past year, as employees have retired or quit, or lost their jobs because of cuts to save money and “rightsize” the business.”

My only experience with Royal Mail was shipping a vintage car watch from my dad to a repair shop up north

If Julian panics at the sight of a header and footer or TikTok, I panic at the sight of mail

After gingerly signing over the emotionally valuable package, I read on a sign the possibility of acquiring a tracked package label

Having inquired about this, the man behind the RM counter smirked and unconcernedly said “Don’t worry about that” and carelessly tossed the package over his shoulder into the delivery basket.

It never arrived.

I can tell you’re Spanish because no British person would find anything remotely surprising about that exchange.

Well, you must be right, because RM is down 10% since summer. And their performance over the last 5 years is just as poor:

The surprise is you expected it to arrive.

One can easily see the pandemic boom there and now you see the pressure of competition in the share price.

Speaking of pressure

The U.S. Supreme Court just signed an ethics code after a series of revelations regarding undisclosed property deals and gifts piled pressure on the Justices

‘Just’

Is le mot juste there.

In other words, Justice Clarence Thomas ruined the golfing:

Samuel Alito, another SCOTUS judge, did something similar, claiming not to know who Paul Singer was after accepting a trip on his private jet to a luxury fishing lodge in Alaska – with all the trimmings.

later on, he adjudicated in the case of Elliott v govt of Argentina

His defence was that if he hadn’t gone, the seat on the pj would have been empty…

Really?

That would have been the height of irresponsibility, really

And speaking of irresponsibilities

This a brilliant and sympathetic article on Business Insider on the rise of ‘overworking’

The practice of employees secretly holding numerous jobs – is this week’s must-read

I don’t need to read it. I’m living it with my three jobs, shortly to become four

Well, not exactly Julian, because this type of overworking’s first rule is like Fight Club – you don’t talk about overworking

Oh ****

I have no idea how anyone manages to do this

I struggle just holding down one job and tend to overwork at it

Some people are born with the ability to do this, I’m not.

I think it’s clear to see, me neither

My friend – anonymised as Mariel – does this. Her remote work schedule at Publicis was 9-10, 4-5 – one hour to do the day’s work, one hour to meet with the boss. But she kept a busy schedule of yoga, singing and dancing lessons, and hot baths throughout the working day.

She was pleasantly surprised with a promotion a few months into the job. Now she works as a marketer for a jeweller I’ve used on occasion. “I love Mariel’s work, she’s really brilliant” the jeweller told me a few weeks ago, “I’m just not quite sure what she does,” he said as he informed me on plans to bring Mariel even deeper into his operation.

It’s shocking but it’s a true story…

The stock is listed: short it.

(please don’t listen to our advice)

You should read the investment advice of Trade Routes Capital, as I did last night, though.

They are of the opinion that markets in 2024 remain in go-slow, inf & rate hikes in rear-view but no growth catalysts for eco momo. So, defensive, cash-generative businesses, and structural growth stories will command premium. US first to emerge into the growth phase.

One thing they highlighted from last week was the treasury auction.

institutional participation was low, those insist will demand higher rates to sustain their interest given the massive increase in issuance, subduing the US economy for 9-12 months.

Powell’s hawkish tone inhibits financial promiscuity. Rhetoric rather than rate rises will be used to control inflation going forward.

Contrast this, for example, with UBS strategists whose global outlook just published predicts 275bp of rate cut in 2024

Trade Routes are very bearish TSLA.

and because I abhor Elon Musk with every fibre of my being, I’m glad to endorse this

Competition news from China is the latest catalyst for TSLA weakness as Dario and I have cited at length in this parish of late. US autos trade on 8-10x forward pe, vs 55x for TSLA. EV trend is slowly equalising, and there’s a falling cost of entry. Industry growth comes at the expense of TSLA growth is their investment thesis in a nutshell.

But Tesla may have something to celebrate – recent news from India suggested the country’s EV imports may benefit from a five-year tax break, in a bid by the country to get more of its inhabitants hooked on EVs

But we have something far more exciting for you live SML watchers

A video seen by The Blind Spot has proven to us that Tesla cars have a gaping backdoor in their system

This is an SML Live exclusive that will be redacted from all transcripts

(I hope I get included in the scoop)

This backdoor happens even when a Tesla car has been sold████ ████████ ███████ ████ ████ █ █████ ███ ███ ████ ████ ███ █████████████ ██ █████ ███████ █████████████ ███████ ██ ███ ███████ ███ █████ ███

It’s related to the current car limit█████ ███ ███████████████████ █████ █████ ███ ███████ ██ ██ ████ ███ ███████ █ █████ ███ ██████

████ ███ █████ ███████████ ████ ████ ████████ ██ ██████ ███ ████ past created bugs where re-registration of cars does not ██████ ██ ████ ██ █ ███████ █████ ██ █████ ██████ ███████ █████████ ████ ██ ███ ████ ███████ ████ █████ ███████████████ ██ ████

This means that even after the car is sold ████ ███ ███████ ████ ████ ███ ████████ ██████ █████████████ █████ ████ ████ █████ ███ ███ ██ █████ ███ ██████ ███ ███████████ ████████ ██████

██ ███ ███ ██████████████ can control it, from taking an autonomous spin, to starting the engine, to unlocking it – see their location, the cars speed █████████ ███ █████ ████ ███████████ ███████ ███ ███ ███ ████ ██████████ ██████ ███ ███████ ███ ████ ██████ ██ ██████████ █████ ██ ████████ ███ ███████ ██ █████████ ██ █ ███ █████ █████████ ███ ████ ██████ █████ ███ ███████████

or ram-raiding?

I don’t know what that is

Well-known driving test procedure in Liverpool. You drive your stolen vehicle at high speed into a cash point and take all the money when it explodes

you won’t get a licence without it.

I’ve missed out on a lot in this life

Clearly!

(Late-night parking with easy shopping access is the euphemism they adopted to describe the practice)

But the worrying but is not that this is happening amongst ██████ – but that Tesla software and firmware can allow this to happen.

If the hack can be engineered by a customer accounts guy just trying to trouble shoot a capacity problem █ ███ ████ ███ ██ ██████████ ██ █ ████████clearly far more malicious stuff which could occur too.

But more critically still, it reveals that Tesla itself retains access to█████ █████ ████████ ████ ██████████ ██████ ██ ███████ ████ █████ ██████ ███████ ██████ ██ █████ ████ ██ ██ █████████████ █████

So if you’re worried about Elon’s control of Twitter, consider the fact he ████████ ████ ████████.

I am concerned about Elon and Twitter.

Firefighters also concerned about TSLA

Very difficult to douse an EV fire, apparently.

Enough of Elon… we revert to markets like a sailor holding onto the main mast in a typhoon

BAML fund manager surveys out yesterday

‘In Europe… Immaculate Disinflation…High conviction on lower inflation & rates, with hawkish central banks no longer seen as the biggest tail-risk by respondents. Robust growth and lower inflation fuel soft landing hopes, although the fallout from monetary tightening remains a worry. Investors turn bullish on European equities, with 68% projecting upside over the coming twelve months, up from 53% in October’

speaking globally, though

2024 investor playbook: soft landing, lower rates, weaker US$, large cap tech/pharma bull continues, avoid China & leverage. 76% say Fed done, 80% say lower short rates (most since

08), 61% say lower bond yields (most ever), just 6% see higher CPI. Investors slash cash from 5.3% to 4.7% (2-year low), move to biggest bond OW since Mar09 and flip to 1st equity OW since Apr `22.

so considering what a terrible three years bonds have had ( as have I) this thesis suggesting a paradigm shift

That dovetails neatly with Goldman Sachs’ recent announcement that hedge funds are shorting the American economy at near-record levels

/cloudfront-us-east-2.images.arcpublishing.com/reuters/M3XE3VTGFVL3DDVSCVWTJWBMOU.jpg)

“Global hedge funds built bearish positions this week to the highest level in nearly five years, Goldman Sachs (GS.N) said on Friday, without citing the underlying reasons. “Financials was the most net sold sector on the U.S. prime book this week and saw the largest net selling in seven weeks, driven entirely by short sales,” the bank’s prime insights & analytics team said in a note about trading flows.”

“The ratio between long and short positions is at a historical low, below 1.7 times. At the beginning of this year, the long/short ratio was at 2.6 times, sharply declining in March in the wake of the regional banking crisis.Overall, hedge funds are underweight financials, at the lowest level since May 2020, Goldman Sachs said.”

This potential bull trend in American bonds may coincide, indeed be a feature of, a bear market in Japanese bonds

Read a piece last night by Deutsche on what they make sound like a looming catastrophe, the overdue correction in Japanese bonds and the end of YCC

“The government of Japan is engaged in a massive $20 trillion carry trade. We argue that it is impossible to understand the consequences of Japanese monetary policy normalisation without analysing what it means for this carry trade. If the Bank of Japan decides to tighten policy meaningfully, this trade will need to unwind. If the Bank of Japan drags its feet to keep the carry trade going, it will require higher and higher levels of financial repression but ultimately pose serious financial stability risks, including potentially a collapse in the yen.”

Either option will have huge welfare and distributional consequences for the Japanese population: if the carry trade unwinds, wealthier and older households will pay the price of higher inflation via rising real rates; if the BoJ delays, younger and poorer households will pay the price via a decline in future real incomes.

Which way this political economy question gets resolved will be key to understanding the policy outlook in Japan in coming years. Not only will it determine the direction of JPY but also Japan’s new inflation equilibrium. Ultimately, however, someone will have to pay the cost of inflation “success”.

As the authors of the SF paper argue, the government is funding itself at very low real rates imposed by the BoJ on domestic depositors, while earning higher returns on foreign and domestic assets of much higher duration. As that return gap has been expanding, this has created extra fiscal space for the Japanese government. Crucially, one third of this funding is now effectively in overnight cash: if the central bank raises rates the government will have to start paying money to all the banks and the carry trade’s profitability will quickly start unwinding.

And the carry trade’s profitability will quickly start unwinding.

The last few years of extremely easy monetary policy have been relatively straightforward from a Japanese political economy perspective: falling real rates, improving fiscal space and income redistribution that has favoured wealthy, older voters. If Japan is indeed embarking on a new chapter of structurally higher inflation, however, the choices going forward are likely far less easy.

The last few years of extremely easy monetary policy have been relatively straightforward from a Japanese political economy perspective: falling real rates, improving fiscal space and income redistribution that has favoured wealthy, older voters. If Japan is indeed embarking on a new chapter of structurally higher inflation, however, the choices going forward are likely far less easy. Adjusting to a higher inflation equilibrium will require rising real rates and greater fiscal consolidation, in turn more damaging to older and wealthier voters, unless the younger voters get taxed. This adjustment can be delayed but at the cost of rising financial stability risk and a weaker yen. The yen, in turn, can only embark on a sustained uptrend when the Japanese government – via BoJ rate hikes – is forced to unwind the world’s last big surviving carry trade in the post-COVID world.”

I quoted large chunks there because I thought it was very difficult to paraphrase succinctly without risking misinterpretation

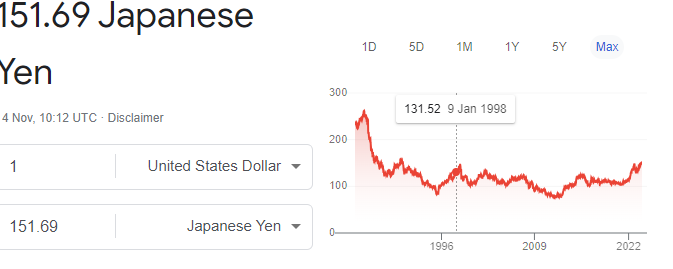

the yen is at a 36-year low

Speaking of new lows

Spain is in flames

Well, not really. But almost

It’s not every day that everyone from my bartender, driving instructor and my grandparents loudly proclaim their attendance – in person or spirit – to the anti-amnesty protests

In typical Spanish fashion, the claims travel poorly outside of our borders

Anti-amnesty? It even sounds bad and unfair

But when the 4th largest economy in the EU and 14th largest in the world finds itself in an unprecedented constitutional lapsus, you should all pay attention

The FT’s pieces on it are, well, very anglo-saxon

“ the plan has sparked fury among conservatives and traditionalists”

Which was whipped up as a last-minute measure by Pedro Sanchez – not included in any electoral manifesto – to guarantee a few votes for his investiture

While I don’t expect much from a news outlet whose nation brought so many volunteers who gladly flew over to kill my ancestors for a cause that wasn’t theirs, more nuance is certainly needed.

The constitution is a limit on the Spanish RIGHT – it limits the power of the conservative right-wing elite, monarchy, and military

Pedro Sanchez’s mockery of it will bite back the Spanish left, European liberalism, and Catalonia

I think a lot of the misunderstanding in the European continent is not getting how Spanish regionalism works

I’m fairly confident I speak for many when I say I do not understand Spanish regionalism fully either.

Spanish centralisation is not a left/right split; 2/3rds of Spaniards oppose the amnesty. In fact, appeasement and opposition of the Catalan region’s independence movements have been just as right as it has been left-wing

In fact, during most of Spain’s history, Spanish centralism from Toledo and then Madrid sprung from Spain’s progressive elites

When Castilian kings unified their kingdom under Roman Law in the 13th century it was to demolish ancient feudal privileges free from taxation, and the free use of arms against Muslims

In the infamous 2nd Republic, Madrid Socialists found their most bitter enemies were entrenched in regional power structures of Andalusia, Galicia and Navarre as they attempted to rein in the terribly powerful catholic church and landowners

Contrariwise, Franco’s dictatorship granted outsized industrial privileges to Catalonia. Aznar’s rule during the 2000s was hand in hand with Convergencia i Unio – the main Catalan (right wing) separatist party

Can I ask you where La Mancha fits into this?

Castile-La Mancha has typically been politically secondary in Spain

There is a reason… it’s the opening line of Don Quixote

Somewhere in la Mancha, in a place whose name I do not care to remember, a gentleman lived not long ago,

I come from the town where Cervantes based Don Quixote – Benavente

Catalonia has also been the most ring-wing region of the country for ages

They’ve always had a sizeable anarchist/communist/socialist voting bloc – but the urban bourgeoisie of Catalonia has ruled the trading hub forever

Even Aragon’s ancient hold over Catalonia was effectively invested by agreement from the Catalonian oligarchy – Aragon had a King, but Barcelona only had Aragon’s King as its Count-King.

While naturally, the amnesty deal will cause more anger on the right than the left – the fact of the matter is most Spaniards – and half of Catalans – do not identify with the region’s radical calls for independence.

And unfortunately, the conflict isn’t comparable to Scotland either. I’m not gonna do the classic right-wing Spanish bit on how Catalonia was never independent (it was never independent), because that’s unfair and broadly irrelevant.

A Catalonian secession would be a death knell because it would guarantee:

a-) right-wing civilian or military governments

b) aggressive right-wing civilian or military governments

c) aggressive and violent right-wing civilian or military governments

d) invasion of Catalonia by aggressive and violent right-wing civilian or military governments.

We’ve seen what happens when a country becomes obsessive over a loss they judge unfair (eg. Azerbaijan’s loss of Nagorno Karabakh – 20 years of preparing to take it back, and they took it back).

And now – what would be the market consequences

Spain’s has been enjoying a brilliant few years economically

But Catalonia isn’t exactly a part of this success

The region has been divested of corporate tax revenues after the original secession pledge made the Madrid government offer rapid tax incentives for companies to re-incorporate in Madrid from Barcelona.

Equity mkt flat over 5 yrs

Furthermore, Catalonia’s ongoing slide into independent radicalism has given the region’s communist and anarchist parties outsized power, meaning they have been imposing rent controls, limits on the purchasing of real estate by PE giants, and other such moves

Essentially, Catalonia is ‘damned if they do, damned if they don’t’

Ironically, if the current situation in Spain has proven anything, it is that our economic situation appears totally unmoored from our political context

But there are worrying precedents for the Spanish economy

The only other time where Spain enjoyed the fruits of FOREX pouring in that it is enjoying now was during the First World War – or our conquest of Latin America.

Where it received loads of liquidity from markets abroad that invested in Spanish stability, or huge influxes of gold and silver.

The same is happening now – with funds from Latin America; which go to either Miami or Madrid

So what worries me is not this anti-amnesty law in particular. It is that now the question of openly challenging the constitution is allowed de-facto (and hopefully not de-jure), so that when our economy inevitably feels the inflationary brunt of this increase in liquidity (that, as always in Spanish history, will be shown to have been very poorly invested) it could lead to a radical change in governmental composition

As happened every time this has occurred – the rise of the dictatorship of Primo de Rivera in the early 20s, or the collapse of the Habsburgs because of LatAm’s silver and gold

So, a story that certainly needs monitoring with the potential to blow up at some stage.

Potential? more like probability

That’s annoying Peter!

We’ll pass it on

on that note of Hispanic despair

nunc tempus taciendi