JR = Julian Rimmer (Resident Boomer and former EM markets pro turned writer.)

DGG = Dario Garcia Giner (Resident Zoomer and former corporate investigations pro turned meme stock watcher and in-house drone expert.)

TLDR: Chat GPT Summary

- Market Mayhem: Julian and Dario bantered about China’s downgrade, bond yield forecasts, and NFP scenarios, sounding more like betting pundits at the racetrack.

- Bond Banter: They deciphered bond yield steepening and a rule called Sahm, turning forecasts into a high-stakes guessing game.

- Global Gossip: From El Salvador’s dictator-style president to Saudi oil promises and the Russian-Ukraine gas romance—more dramatic than a Netflix series.

- Turkish Twist: Turkey’s sky-high CPI, Mearsheimer’s controversial views, and Turkey’s roller-coaster ride from chill mediator to chaotic party animal.

- Shipping Sagas: Anecdotes about sinking freight shipments and the UK’s haulage companies going bankrupt faster than a game of Monopoly.

- Heroes and Villains: Dario praised Mearsheimer, while Julian dubbed Musk as a supervillain, blaming him for Twitter’s wild transformation.

- Wine Whimsy: Julian’s wine recommendation, the Le Riche Reserve Stellenbosch 2020, was praised more than a celebrity on a red carpet.

Good morning, Dario

With some heavy controversy over the selection of heroes and villains

And I haven’t even told Dario who my villain is for today

Memes of the day today

Which, as always, is about six months behind the bond mkt itself

However, the lodestar for markets this week is data

Eurozone GDP and German IP Thurs plus German CPI, Japan GDP and US NFP Friday

Consensus for this latter is 180k

And given recent mkt moves the mkt is highly dependent on a number around that sweet spot

Much less than that and people are talking recession and hard landing and DXY weakness, much more than 180k and mkts will push back the timing of the first rate cuts from March of next year to the summer.

Mkts are priced for perfection.

Which brings me on to the DB outlook for bonds that, funnily enough, had exactly that title.

‘Full steep ahead We expect 10Y UST to decline to 4.05% and 10Y Bund to remain broadly unchanged around 2.6% at the end of 2024. The most salient feature of our forecast is a significant steepening with 2YRUST declining to 3.15% and 2Y Bund declining to ~2%. As markets are already pricing a soft landing close to perfection and term premia remain too low, the risk reward for steepeners is attractive, in our view – notwithstanding the current uncertainty about the timing of an easing cycle. On the other hand, the BoJ is significantly behind the curve in tightening policy. The more the easing cycle in the US is delayed, the more likely it is that the BoJ will have to hike interest rates substantially more than currently priced.’

Standard Chartered Bank is worried about the Sahm rule being triggered by payrolls data Friday.

‘Sahm Recession Indicator flashes red when when 3mth moving average of UNR rises by 0.50 ppt or more, relative to its previous 12mth low’

Standard Chartered Bank

Identify several scenarios

NFP at 100k and a further 100k of downward revisions (15% probability) would take the three-month moving average (3mma) down to 150k, the lowest since mid-2020 and a sharp drop from Q3 levels. This may be enough to have about 30bps of policy rate cuts priced in for the March FOMC from about 16.5bps now. But February FOMC pricing could go from 2bps to 15bps of policy rate cuts.

We do not assign a substantial probability to such a large drop because none of the usual labour market indicators are pointing to such weakness. We doubt investors would be willing to price much more than one 25bps rate cut for March, as there are three more NFP releases between the 8 December release and the March FOMC meeting.

This scenario is most ambiguous for the USD. It combines a high probability of sharp rate cuts with some possibility that the pace of slowing activity is too fast for investor comfort. It is possible that the rates side dominates and the USD falls across the board, but if confidence is shaken, high-beta and EM currencies would be at risk. We believe the safest position is short USD-JPY or AUD-JPY on the view that the JPY would benefit from yield compression and will not be hit too hard from shaken confidence.

Secondly

NFP at 150k and no revisions (35% probability) is slightly weaker than our forecast. Such an outcome would probably take March FOMC pricing to about 20bps and January FOMC to about 10bps. This is probably close to the optimal ‘bad news is good news’ scenario, with activity disappointing enough to move rates but not so bad as to force big downward activity expectations. Unlike the first scenario, this might be a slowing that is fast enough to put downward pressure on yields, but not so fast as to shatter confidence in activity. In this scenario, we might see the higher-beta currencies outperform safe havens such as the JPY and CHF.

NFP at 180k and no revisions (30% probability) would be in line with the consensus. With about 30k added because of reduced strike activity, the underlying 150k would probably be seen as good enough for a mid-late Q2 or early Q3 policy rate cut. UST yields have dropped sharply in recent weeks; this outcome may not be enough to maintain downward yield and USD momentum, but it is likely to be a ‘not so fast’ signal on yield and USD downside pressures rather than a trend breaker.

And thirdly

NFP 210k and positive revisions (20% probability) is probably the most dangerous outcome from a market perspective. It would force a re-evaluation of how fast the US economy is deteriorating and how fast the Fed would have to cut rates. This scenario is the most USD positive (see Scenarios for the US economy). With only one NFP release before the 31 January FOMC, it would be hard for that report to be bad enough to put cuts on the table at the January or March meetings. Moreover, if the January release turns out to be strong as well, the market would probably reintroduce a small hiking risk in March – so the possibility of a major upward lurch cannot be discounted. With ECB commentary and data tilting towards dovish, this could lead to a significant pullback in the EUR.

NFP 210k and positive revisions (20% probability) is probably the most dangerous outcome from a market perspective. It would force a re-evaluation of how fast the US economy is deteriorating and how fast the Fed would have to cut rates. This scenario is the most USD positive (see Scenarios for the US economy). With only one NFP release before the 31 January FOMC, it would be hard for that report to be bad enough to put cuts on the table at the January or March meetings. Moreover, if the January release turns out to be strong as well, the market would probably reintroduce a small hiking risk in March – so the possibility of a major upward lurch cannot be discounted. With ECB commentary and data tilting towards dovish, this could lead to a significant pullback in the EUR.

While we cast our scenarios in NFP terms, further increases in the UR would attract both the Fed’s and market’s attention. Our version of the Sahm rule has already triggered and we suspect there are a variety of such rules out there. Breaking upwards to 4.0% or higher would likely be viewed as confirmation that the US economy is at least slowing. Our and consensus’ expectation that the UR will consolidate at 3.9% adds a little more evidence that the economy is slowing, since it brings the 2mma higher. However, we think the UR increasing to 4% or higher is needed for the market to put NFP aside and focus on the UR.

Hopefully, that has everyone fully debriefed about NFP so now it’s a question of waiting for 130pm Friday

However, if you knew what the release would be you could trade it on it now rather like some people seem to have done before Oct 7th…/

Dario?

A new study by Columbia and the NYU found the Israel ETF, which only usually has about 2,000 shares shorted, shot up to 227,000 shares shorted on October 2

They ran a backwards comparison in time and found this short selling activity was “really extraordinary” especially in the almost-total absence of parallels in the history of short sellers of Israel

“We think it’s virtually impossible this happened by chance,” Mitts told CBS News.

Finding out exactly who made the trades, and the profit, would be “exceedingly difficult,” and Mitts says he is “pretty pessimistic” that whoever was betting against the Israeli economy will be found. Similarly, Mitts says it’s “not so easy to stop this sort of trading” from happening. Instead, he suggests a different goal.”

This comes amidst more news indicative of failures in the usually competent IDF

I actually knew the commander of a female intelligence battalion, but one in Hebron, and I can actually sort of understand what could have happened

These battalions sound fancy but they’re mostly people staring at computer screens for long amounts of time

A quite low prestige job in the IDF – and staffed with very low-morale recruits

It had a reputation as a place where ‘you didn’t wanna end up’

Perhaps this unit’s reputation got the better of its intelligence? Who knows

I heard the intelligence was misinterpreted and ignored

I was turned away by 2 buses yesterday to Luton

And then told off by an old English senior for rushing into a bus with a ticket in hand

He said it was a breach of procedure

At this point I’d been running 1.5 hours late and in danger of missing my flight back

He replied something like “I’m not green in the head”

And speaking of green

(Technically he’s a millennial)

Millennnnnnnnnial

This rounds off a strong 2023 for Nayib Bukele, also known as the world’s coolest dictator

Which is a self-given name!

(soi-disant)

But his supporters say results speak for themselves

El Salvador’s crime rate, which spiked at 107 per 100,000 in 2015 fell to 7.8 per 100,000 in 2023

It’s also sparked pro-Bukele rallies in nearby countries

Are babies born with tattoos there?

And I’m sure it’ll turn topsy turvy at some point soon

But its obvious why someone taking exceptionally violent measures is popular in a place plagued with exceptional violence

And speaking of despots

Still desperately trying to talk oil back up by promising cuts would be fully implemented and more would be forthcoming (if speculators don’t buy crude futures now).

(My parentheses)

It’s not working.

And in other news we missed (or, at least, that I missed) Brazil is expected to join the OPEC+ group of countries

Though Petrobras importantly announced it wouldn’t be joining the production cuts

Formally joining OPEC+ on January 2024, it means OPEC+ will control around 50% of the global oil market

And speaking of oil – did you know that Russian gas was still transiting through Ukraine, Julian?

And they will continue functioning until December 2024 – when Ukrainian Naftogaz severs its supply contract with Gazprom

That’s because Austria has storage and pipeline facilities to pump this gas to Hungary, Germany, Italy and Slovenia

Ukraine has agreed to facilitate access to Russian gas for European traders on a case by case basis, it’s unknown if Austrian’s Gazprom contract will be allowed

Theoretically, if an Austrian company books the Russian gas directly through the Ukrainian pipeline and avoids Naftogaz, there is no direct relationship between the latter and Gazprom, meaning supplies could continue

The country had planned a pipeline with Germany to diversify its imports from the West, but work on the pipeline hasn’t started and won’t be finished until 2027 – leaving the country with at least two additional years of reliance on Gazprom.

Sometimes, war is weird!

Everyone benefitted, even if this dutch imported timber was quickly turned into Spanish ships that would then harass Dutch shorelines

As this chart I caught at the weekend illustrates perfectly

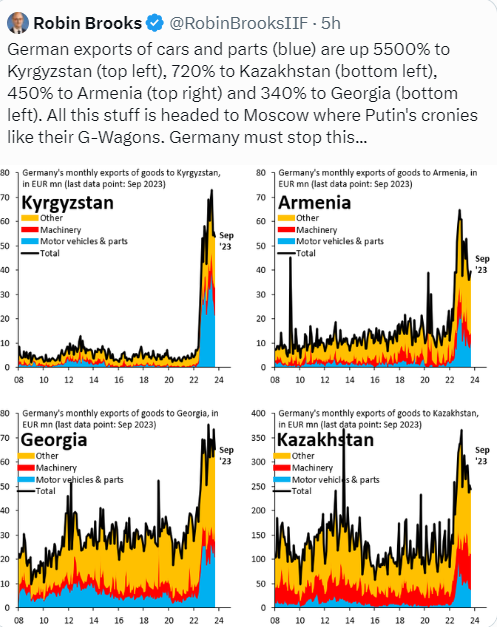

We did mention something along these lines last week but as data becomes available, the scale of the sanctions-busting becomes ever more clear

Once, the poster-child for EM equities

A cheaper way still to perhaps take advantage of this are the stocks Prosus and Naspers

And to this end I saw a note published by Investec a few days ago on this subject

Prosus & Naspers – Under Promising and Over-delivering. A new paradigm and structural shift lower in the discount to NAV?Mgmt have done a superb job in reducing non-Tencent portfolio losses and per the chart below, this means that Tencent earnings fell back to 114% of core earnings (chart below), a number not seen since FY14. Cash flow from operations for the first half up to $904mil (ex. Multichoice) a record! Turning to Tencent, Dave ups his earnings forecasts 6% and 14% respectively for FY23e and FY24e on better GP margins and strong cost mgmt.

I’m generally not a fan of this complex and run a structural underweight, I see layer upon layer of reasons to address this:

- Per last week’s notes, we believe the China macro is starting to turn for the right reasons. If this kicks we’re in the money

- Tencent’s results were decent and the stock currently trades at 15.4x fwd, right at the bottom end of the very long term range. If there’s a re-rating back to the long term average and / or mgmt continue to surprise on the earnings front, we’re again in the money

- PRX and NPN are trading at 35% and 39% discounts to NAV respectively and while I think it’s premature to pop the champagne after a single result, another couple of halves like this and there must be downside risk to these discounts. If this plays out, we’re again in the money….

In summary, Investec move Prosus to 10% of their model portfolio. Proper conviction there

Someone who made the shortlist for my top Ten Villains of 2023 without actually getting on it is President Erdogan of Turkey

The man whose facial expression always gives me the impression of someone trying to remember a shopping list expressed hope for a fresh beginning in bilateral relations with Greece.

Obviously now the Turk elections have passed, he has no need to be xenophobic and hostile any longer

On his upcoming visit to Greece scheduled for Dec. 7, he said: “I hope a new era begins between the two countries. We are trying to make more friends and less enemies.”

(Obvs that should be fewer enemies, forgive my pedantry)

This sounds like an interesting idea, Erdo, being friendly to neighbours?

That’s called diplomacy, something the Turks have not practised for more than a decade now.

‘Zero problems with our neighbours’ was Davitoglu’s promise back in 2016

But this promise fell apart and was sacrificed on the altar of populism and nationalism

Mostly of their own making

Turkish CPI for Nov just the 62% yoy, they just raised rates to 40% last week

However, Turks have become experts at managing fx risk

And they were/ are heavily invested in fx hedges like bitcoin, gold and real estate where possible

And smthg like half of all bank deposits are held in hard currency

The average bloke on the street is much more in tune with fx rates than anyone in G7 i guess

That CPI data is ‘official’ and not the real number which, of course, it goes without saying, is higher

Some interesting anecdotal rumours surfaced on Reddit yesterday

An individual who claimed to run a family owned shipping business in Antwerp said:

“A lot of factories started to produce less and less because of the high energy prices since the start of 2023. This resulted in a drastic reduction of shipments that we do. It has been going down ever since. We’ve had a couple of really good weeks during this period but when you look at the general picture, it’s dogshit.

I’ve started to look at other ports and area’s in The Netherlands, Germany and France. Same shit everywhere. We have a pretty big network with companies in our region and all of them 1 by 1 are pulling the alarm. Drivers used to stay home a couple of days a week because of the shortage of freight trips, now they’re being sent off because the cost of keeping them is too big.”

Not exactly surprising. The man finished his anecdote with an eloquent summary of the situation:

“We are getting f*cked atm and I see it everywhere but there just is no f*cking artice anywhere on the news reflecting our situation.”

(my censoring)

The story was reflected by fellow market watchers of freight rate declines

If you wanna check for yoruself:

Our freighter philologist missed a relevant news story from April, however

That 453 haulage companies in the UK reported bankruptcy over the past year

UK SME hauliers hit by rising costs going bankrupt every day

The yearly rate of collapse has doubled since 2020, with one or two hauliers going under every day in the UK

“A study conducted by The Loadstar shows at least 90% of those that failed in the past month have been independently or family owned. And in the past three days, Companies House shows five have declared bankruptcy, all independently run.”

The reasons?

A deadly combination of cost of operating transports, reduced freight volumes, and less demand

Higher interest rates turning the screw on hauliers relying on debt financing

I remember at Kroll Julian

In my final year I saw SO MANY debt financing startup acquisitions

Specifically for logistics

At the time I thoguth it seemed a very logical and wise investment

Now I see it was likely a hype derivation of exceedingly low interest rates

“Price Bailey also looked at the credit risk score of the UK haulage sector. Some 33% of businesses in the sector are deemed at maximum risk, up from 22% 12 months ago, “considered at imminent risk of collapse”, it said, “and will find it almost impossible to access extra funding unless directors provide personal guarantees”.

And, please everyone, take this as a warning, Dario’s is very controversial as he’s picking a hero who’s on my villains’ shortlist

So my hero is on my hero’s shortlist

John Mearsheimer!

A bloody waste of time and only one thing stuck with me from it – his theory of offensive realism

That great powers are billiard balls with no real difference between them but size

The next thing I remember from him was a post-2015 speech where he said Ukraine was between a rock and a hard place and that the West would never provide sufficient support for it to head off a Russian invasion. He then said Ukraine was unwise to put its support in the West for that reason

Now – I really thought for all of 2021 and 2022 he was being proven wrong

It seemed like the West was providing enough aid

That is until this summer’s counter offensive by Ukraine slowed it all to a grinding halt

So I think the professor can add another accolade to his record – for being a smart cookie that isn’t cowed by going against the herd and being proved right int he end

I think someone on this chat very much disagrees with this

I wonder who

Before we move onto my villain, which I think may provoke a similar diametrically opposed view from Dario

Let’s have a brief vinous interlude

And wine No2 of my top ten wines for 2023

Le Riche Reserve Stellenbosch 2020

Full-on cabernet sauvignon made within 10 miles of the Indian Ocean at some degree of altitude but not especially high.

No wonder this wine is scoring close to perfection by many wine critics.

£50 a pop.

11:27 JR:

Or museum wines https://www.museumwines.co.uk/wines/red/

Right, three minutes left to deconstruct my first villain of 2023

NapolElon Musk

My biggest problem is squeezing all the people I despise with every fibre of my being into the five people I have allocated out of the ten we choose. So much hatred and so little time to indulge it.

Elon Musk, primarily for his breathtaking, unsufferable arrogance, for his blatant anti-Semitism, his parroting of Russian propaganda and his preoccupation with nutjob right-wing conspiracy theories.

And his moobs

Also, I was a late convert to Twitter and only really properly adopted the technology when the war started in Ukraine.

The resemblance to trump is not surprising

So the damage Musk has inflicted on Twitter, turning it into a cloacal wind tunnel and bogging it down with the crappiest of advertising is a real loss

@robert – not had. good?

But

I do think Twitter is, and was, and has always been a cloacal wind tunnel. But I do see reasons why Musk’s just made it worse

I have so much ship on my feed now