| SNEAK PEEK |

— Izzy catches up with investment advisor Russell Napier, who tells her credit rationing and central bank politicisation are on their way.

— A growing chorus of voices are acknowledging that we all become Liz Truss eventually, including Jeremy Hunt.

— Dario explores how the confiscation of Russian assets may have major reverberations for sovereign immunity and a very specific legal case being brought by investors against the Spanish state.

Good morning subscribers! And welcome to Sunday.

I’d like to start today’s newsletter with an observation about contrarians, which is how I’m often described. It’s a reputation that has even gotten me a slot on the judging panel of Ali Miraj’s Contrarian Prize. I share this with economist Vicky Pryce, whistleblower Michael Woodford, and Nigel Farage’s favourite PR man Gawain Towler. As can be expected, we have wide-ranging and heated discussions.

But contrarians don’t all come in the same shape and size. Indeed, I would argue there are two types of contrarians in the world. Those that argue for the sake of arguing, usually taking the opposite of any position regardless of whether there is any merit to it. And then there are those who argue for the sake of exposing the blind spots and stress-testing the popular narrative, in the hope of being ahead of where the story will be tomorrow, rather than today.

I would like to think we at the Blind Spot fit into the second category. And in that capacity, I have to say, it can sometimes be tough being a contrarian! For the most part, it involves saying things that can, at the time, be deeply unpopular or discomforting for those around you, ensuring significant backlash. But that isn’t even the worst of it — if you’re too far ahead of the curve, by the time the story you’ve been predicting comes about, it’s often the case everyone has forgotten that you were saying these things long before it was fashionable to do so. It is our (admittedly annoying!) Cassandra complex.

So, as the Blind Spot heads into its third year of operation, I thought I would reflect on some of the views we got right despite the odds, or views that are now finally entering the mainstream consciousness as acceptable.

I want to start by giving a huge shout-out to Dario. Not just because he is so incredibly resilient and forgiving of my crazy and chaotic schedule, but because he has been a fantastic colleague who has taught me so much about my own blind spots. I’ve always known I had a geopolitics weakness, and there’s no doubt Dario has helped me fill that void over the last two years. Whether it’s assessing the power complexities in Africa’s Sahel to keeping me abreast of zoomer meme-talk and MrBeast burgers, nobody has been more ahead of the curve on such subjects than Dario. But his most commendable insight has clearly been his very early take that Western weapons sophistication won’t be enough to win the wars of the modern age. Small, nimble and cheap to reproduce arms will be key in Ukraine to Nato’s detriment.

On our part, the biggest single theme we’ve tried to convey over the last two years has been our strongly held conviction that Western economies have been consumed by the same corruptions and economic malaise that beset the Soviet empire towards its end. More so, that we had sleepwalked into a command economy structure and didn’t even know it, largely because of the subtle changes we’d brought in over time into our management systems.

And that’s why we were both overjoyed and overcome by our Cassandra complex when we saw historian Niall Ferguson arrive at a similar conclusion this week. (Though, to be fair, he has been warning about the risk of a relapse into authoritarianism for a long while.)

Most important to our own analysis, however, has been the view that the West will eventually face its own Perestroika moment where, like the communist bloc in the late 1980s, it will be presented with a choice between reform of the system or a doubling down of authoritarianism into an even more acute (AI-led) form of command-collectivisation, or what we have been calling, since our FT days, Gosplan 2.0.

Choosing reform (‘perestroika’ being the literal Russian word for restructuring) means helping nudge the system back into a market-led value-led economy where free enterprise and capitalism is once again allowed to thrive and help the system innovate its way out of its issues. But making this choice is akin to a shock therapy and comes with much risk. Risk of the unknown, risk of potential chaos and risk (just like Russia in the 1990s) of exploitation and plunder by the remaining vested interests. If it goes well, the shock-induced pain won’t last long and the fruits of the transition will pay off handsomely. You can consider it a model where fortune favours the brave. But it does have one major vulnerability: It’s unlikely to work unless we collectively come to understand that “liberty does not exist in the absence of morality” or shared common values.

Choosing the status quo on the other hand, means an increasingly accelerated slide into authoritarianism, centralisation and command structure. It might seem the steadier and safer pathway at first sight, but the perception that it is riskless is wrong. The risk with it is that it calls us to put complete trust in a paternalistic order, on the assumption the overseers we anoint really do know what they’re doing and have the people’s interests at heart, rather than their own. Some might say it’s a model that worked in the world post WW2 and delivered great prosperity. We should give it a chance. This is true. But they must also remember that, back then, it was a different era — the New Deal came in the footsteps of a period of great sacrifice and national cohesiveness, centred on clearly understood collective values. Putting trust in technocratic overseers that believe in nothing, is not the same thing at all.

Both pathways require cohesiveness and a lack of corruption to work. But they also require population-wide engagement in a common mission, ideally one underpinned by a positive idea of tomorrow, not a defensive scary one which fills the younger generation with anxiety and fear. The only question is which pathway, if it fails to live up to that challenge, is potentially more destructive for humanity? Corruption in the free system can at least be offset and fought off with competition in an open market for both commercial goods and ideas. Corruption of the authoritarian system allows for very little course correction.

The blind spot in the system, I think, is that it is the paternalistic technocrats who are commonly judged to be pro-liberalism and pro-competition, with the populists judged to be those nudging us towards authoritarianism. My hunch is that the risks actually lie the other way around.

As usual, this newsletter was brought to you by me, Izabella Kaminska, and Dario Garcia Giner.

Send tips to [email protected] and [email protected].

| THE BIG BLIND SPOT THIS WEEK |

THE POLITICISATION OF CREDIT: This week The Blind Spot was fortunate enough to catch up with the Solid Ground newsletter’s Russell Napier to get his thoughts on the latest occurrences in both France and the UK.

Napier’s long-standing view, for those who don’t know, is that financial repression is inevitably coming to Western markets, because that is the only way those economies can constructively cope with the stagnation induced by over-indebtedness and low productivity. The last shot we had at avoiding this fate, he says, was with the Truss “go for growth” plan. But that opportunity was skewered by the market reaction (fanned by a million editorials lambasting Truss’s economic plans without any attention to their merit, in publications like the FT, I should add). As a result, no politician should, in theory, be mad enough to try it again.

Or, as Napier put it: “She said let’s just go for growth and we’ll grow at such a high rate it just won’t matter [if we get inflation] but the bond market just said no, and the only other way to get out over-indebtedness is austerity or default … they have to go to financial repression because high growth as a strategy out of over-indebtedness is not going to be funded by the bond market.”

No ideologue: To be clear, as with our own defence of Truss, Napier’s view seems not to be driven by political ideology. It’s based instead on a cold hard reading of market and economic conditions, as well as pragmatism. Indeed, the view arguably derives from an acceptance that you shouldn’t let political ideology get in the way of market analysis — so if someone you’re not politically aligned with is presenting a viable plan, you can’t just dismiss it out of hand because it’s unfashionable or doesn’t compute with your own biases (cough, cough, the FT).

Butskellism: Napier’s other big point is that the current economic circumstances don’t allow for much political manoeuvering or variance. There’s a reason why the same economic remedies — all skewed towards financial repression — are being pushed by the main parties. This is where the path of least resistance leads politicians who don’t want to rock the boat and think the promise of stability is more of a vote winner than the prospect of the unknown. The only viable alternative to financial repression and credit rationing, as we’ve mentioned already, was the Trussonomics defibrillator shock. And he says we know how that ended.

So where does that leave us? “If the Truss government was the last attempt to sort of take a different way out, it’s gone. I think it doesn’t matter who you vote for, you end up with roughly the same thing. So the market’s not maybe saying we’re very sanguine about Labour. They’re just saying it doesn’t really matter who you vote for. We are heading towards this route,” says Napier.

SCHNABEL AND MACRON

So how does it all fit into the bigger picture? This summer’s elections will be crucial to how the future pathway is laid out and to what degree the technocrats come clean about the politicisation of their supposedly neutral institutions. To that end, Napier says the European Central Bank’s Isabel Schnabel’s May speech on the benefits and costs of asset purchases is a must-read since it offers a big tell about what’s to come.

“She’s saying that QE has undermined their ability to meet their price stability targets because it’s undermining their balance sheet, i.e. the more they put interest rates up, the more losses they have on their bonds, the more governments get upset about recapitalisation, the more politicised they get… A lot of us have been making these criticisms of the ECB for years and they’ve kind of denied it and she just came out and accepted all the criticisms and said that’s why we’re going to stop QE,” Napier said.

That, according to Napier, is as strong an admission as you will ever get that QE was a mistake and that it’s no longer a viable pathway.

The other big tell: Well, that was Macron’s April speech at the Sorbonne, where he de facto highlighted that, without the explicit politicisation of credit and central banking, “Europe might die” — by which Napier assumes he means the European Union project.

“Macron said [in that speech] that the ECB should no longer have a price stability target. He said that categorically. It’s not good enough. He wants a growth target,” says Napier, adding that comes with more targeted liquidity for bank lending and the risk of massive politicisation of the process.

“If it results in more money flowing to France than Germany, the European Central Bank gets inherently political. Cutting interest rates and letting the market decide which banks lend money and who gets money, well, you can hide behind the guise of central bank independence, but when you use the word targeting — I know they’ve had these before, but if that’s the word — then in the construct of the new industrial policies for Europe, it’s a pretty dangerous combination in my opinion,” says Napier.

THE POLITICISATION OF THE ECB

How might ECB intervention look this time? Well, as we already speculated in the Blind Spot last week, a lot like the BoE’s intervention on Truss. That’s to say, it certainly won’t be preemptive because the whole point will be to allow the chaos induced by market instability (and any potential associated civil strife) to teach the French electorate a lesson. Napier seems to agree.

“If Macron really is aiming for chaos, and he legitimately is trying to do that, and you think Macron is an ally of the project, then you don’t use [the Transmission Protection Instrument] until after there’s some type of chaos. It’s deeply political when you use this TPI now,” says Napier. “If you want Macron to win, you don’t use the TPI before the election. He’s trying to frighten people and one way you do that, as we discovered in the UK, is to let the bond market sell off.”

The new ‘Whatever it takes’. According to Napier, if ‘whatever it takes’ means whatever it takes to hold the single currency together then that now means “whipping the French electorate into line to keep the single currency together, which means the ECB not buying French bonds.”

“Imagine if you’re running Italy. Well, Italy is a system that runs on patronage and the patronage is now flowing from Frankfurt not flowing from Rome? So the Italians will want a say. And there will be a great big battle over how the money flows. If it just flows to the banks and the banks can lend it however they like, well, that’s fine, because the Italians control their banks. So that’s absolutely fine. But if targeted means it’s only going to fund green projects, well, if you only target funding for green projects for instance, maybe Germany gets 80 percent of all the credit because that’s the manufacturing power of Europe. So it’s just a deeply political monetary policy.”

No more Covid-style fragmentation: But it’s also the case that the technocrats feel that subsidies can no longer be determined on a state level. Hence, all the compulsive talk about upping Europe’s competitiveness, (which we at the Blind Spot increasingly think is merely code for centralisation). “I thought what was really important in Macron’s speech is that he said the response in the last two years has been subsidies at the national level, which fragments the single market. I mean that’s really important stuff. So I imagine they’re bringing Draghi up to try and stop the fragmentation of the single market. I think they’ll fail. But he’s the man you’d go to,” he said, with respect to the much-awaited Draghi report on Europe’s competitiveness that’s set to come out this July.

Crystal-balling Draghi’s report: According to Napier, it’s not hard to predict what will be in that report. “I think I can guarantee its conclusion… there needs to be more state involvement in the allocation of capital and that the state that needs to be doing it is the supranational Commission and not the individual member states,” he said. “‘Whatever it takes’ means whatever it takes. And if it’s the deep politicisation of the ECB to support centralisation, Macron doesn’t seem to care anymore.”

Overt politicisation: And if the ECB are of the same opinion as Macron, they won’t care anymore either. “There’s no point in pretending that they’re a nonpolitical organisation. Whatever it takes means centralising power, whatever it takes, full stop. Whatever it takes is not running monetary policy, it’s the centralisation of power and the saving of the euro. And if Macron says that the current policies lead to a fragmentation of the single market, then it has to be stopped whatever it takes. So yeah, they will have to be overtly more political.”

Pathway for a queenmaker: Of course, if the ECB comes to the rescue of an induced French debt crisis that also lays a solid path for current ECB boss Christine Lagarde to one day become French president.

Napier: “Let’s say Lagarde and Macron agree that what the French need is a bit of chaos, so that when the 2027 election comes, they vote for somebody like Lagarde. Well, I mean, assuming she wants to run (and I think she probably does want to run) she’s clearly going to be the moderate pro-EU candidate and if Macron really genuinely believes this stuff, she would be helpful. She would be helpful in a bit of chaos … because it massively increases her chances. So she’s legitimately a candidate with the ability to control French bond yields when Lagarde believes that chaos has achieved the necessary political goals.”

What happens when chaos strikes? Napier for one can’t predict: “This is social engineering on a grand scale. I can’t forecast what will happen in the chaos, and neither can Macron and that’s why it’s such a gamble. It can spread to other countries. It doesn’t have to be a French thing. If bond yields blow up in France they can blow up anywhere.”

And where is the risk? Everybody knows that France’s over-indebtedness lies in the private and corporate sector, but nobody can really find where exactly it is. The source of the consternation is the BIS, whose numbers say France’s private sector debt servicing ratio is near 20 percent relative to the UK’s 14 percent, and the US’s 15 percent. “In terms of the corporates, this is the great mystery about France — if you look to find the corporates that are over geared, it’s quite difficult to find it in the listed sector. So, therefore, where is all the successive corporate gearing that the BIS has been reporting year after year? It could be it’s in the unlisted sector. It could be that it’s small and medium enterprises, but I don’t actually have an answer for that,” Napier says, saying the BIS has not provided him with any further clarity.

CREDIT RATIONING IN THE MODERN AGE

And what will financial repression look like? Key to the new financial order will be the repression of the growth in non-bank credit, specifically corporate debt. “You have to keep that suppressed because in repression actually borrowing money looks quite attractive because interest rates are below inflation. So that means you have to politicise credit and bring in restrictions on the ability to create credit in the marketplace because you need to create quite a lot of credit through your state-run banking system to generate growth in broad money and nominal GDP,” Napier says.

Are we all China now? Pretty much. “You’re massively politicising the flow of credit and there’ll be some corporates who you think should get credit and some who won’t,” he says. Except our credit rationing — the process by which only those corporates that serve the “national interest” get credit — will be dispersed in line with a narrative focused on meeting the great ’emergencies’ of our time.

The post-WW2 parallel: Napier reminds us too that none of this is new. “The fantastic little example of this is after World War Two, when the United Kingdom had a thing called the Capital Issues Committee,” he says. “If you and I wanted to issue a corporate bond we had to go to the capital issues committee and get permission, (and) it decided whether the investment we proposed to be funded by the bond was socially useful or socially useless. And we politicised the flow of that form of credit.”

This, however, ensured that after WW2 the corporate bond pretty much died. “The state didn’t want to fund all those guys. It had its own ideas and what should be funded,” he said.

You ain’t seen nothing yet. Macron’s vision of what should and shouldn’t be funded is very clear, says Napier. If you’re not in the three things he’s defined as essential — all part of his new ‘industrial policy’ for Europe— then you’re going to struggle. “That is Macron’s view of where credit should be flowing to if there was a Capital Issues Committee for Europe. You could be damn sure if you wanted to gear up a piece of commercial property or do a private equity deal that you wouldn’t be on the top of the list to get your credit.”

The other form of repression: Look out for more news and developments with Europe’s so-called capital markets union project, which — even though it has failed to gain traction for over 10 years — is now seriously back in vogue. This time, however, the political will is there to take it to the next stage. Except, rather than being a mechanism that allows for the free flow of credit across Europe, akin to the way credit flows across the US, it’s likely to be shaped into a system that serves a higher calling. “The reason they want a capital market union is so they can steer the private sector capital/savings to where they want it to be,” says Napier. “That’s what his Sorbonne speech was all about. I think we all accept that means steering it over here towards Europe and away from the US. What we don’t think about it is where is he steering it away from who’s who’s not getting the credit?”

Credit rationing: “Credit is a scarce national resource to be deployed for political means. This is exactly where we were after World War 2 in rebuilding Europe. And that is the agenda, but somebody has to not get credit as part of that shift and we’re not focusing on that enough,” Napier concludes.

Only the polycrisis gets funding from now on: As Napier succinctly puts it, “the more they talk in terms of emergency, the more they can bring in emergency finance, which is to ration credit. As opposed to let the market price credit.”

Unconscious authoritarianism: Napier doesn’t think any of this is necessarily consciously malevolent. It’s a reactionary move following the path of least resistance by politicians who think this is the best way to appeal to whoever they value appealing to.”They have to go to financial repression because high growth as an exit strategy from over-indebtedness is not going to be funded by the bond market and austerity, default or hyperinflation won’t get anybody re-elected.

The debt, in other words, is conditioning the policy they have to follow.

| BUSINESS, ECON FINANCE ETC |

WE ALL BECOME TRUSS EVENTUALLY: While framed as defending the indefensible, Chancellor Jeremy Hunt was revealed on Tuesday, in the Guardian, as coming to a similar conclusion as Truss on how best to stimulate growth. According to audio leaked to the left-leaning British newspaper, the chancellor told a meeting of students that he was “trying to basically achieve some of the same things” as the former prime minister, but that he was doing it “more gradually”.

The problem is … Trussonomics literally can’t be gradual. This is what Hunt and U.K. PM Rishi Sunak failed to understand (and what Labour’s Rachel Reeves and Keir Starmer are similarly failing to understand). The go-for-growth model, if it’s to kickstart growth, can only be triggered by an escape-velocity achieving shock. All other pathways lead to financial repression, as Russell Napier has eloquently explained above.

Larger factors at play: Hunt nonetheless praised Truss for “accepting the mistakes she’d made with good grace” and suggested the episode had not had a lingering effect on the U.K. economy. “No, I don’t think it’s had an effect. I don’t think it’s the main cause,” he said.

IT’S OK WHEN LABOUR DOES IT. The establishment’s slow-running realisation that Truss was probably right, however, is making it increasingly difficult to claim the opposite was ever true. The hope seems to be the public just won’t notice the hypocrisy when the time comes to admit as much. That time seems to be now. The FT, for example, reported this week that fund managers now believe a Labour government could raise extra money for investment from bond markets without causing a Liz Truss-style gilts crisis.

A reminder: Aspiring chancellor Rachel Reeves has been explicit throughout the election campaign that “borrowing more is not an alternative because debt as a share of GDP is the highest it’s been since the 1960s,” and that taxing more was also “not an alternative because tax is already at a 70-year high”. And yet, fund managers are now saying things like, “if the UK were to borrow a little bit more, would it get out of hand? No,” according to the FT and that, “markets have been quite agnostic about high deficits”. How long before Labour buckles too?

This sounds like a familiar Reform policy? The FT then notes that:

Investors may also be more tolerant of a relaxation of fiscal rules than Reeves suggests. For example, some fund managers and economists suggest Labour could tweak its definition of net debt to exclude losses on the BoE’s bond portfolio. “There is scope to modify the framework to allow more borrowing,” as long as updated rules were policed by the Office for Budget Responsibility, the fiscal watchdog, said Simon Ward, an adviser at Janus Henderson.

Labour could “probably” add “£20bn or £30bn” to the gilt remit without pushing up borrowing costs, said Tomasz Wieladek, chief European economist at T Rowe Price.

You can’t make it up! One man who’s definitely spotted the insanity is SocGen’s Albert Edwards, as he noted on X this week:

PROJECT PEUR: French Finance Minister Bruno Le Maire, meanwhile, warned on Tuesday it’s not just the far right that threatens to destabilise France. He pointed out the country could fall into a “debt crisis” and be placed under the supervision of the International Monetary Fund and the European Commission, should the far right or the left-wing alliance come to power in upcoming elections and enact their programmes. “Opening the floodgates to public spending at a time when we should be restoring our accounts will lead to France being placed under the supervision of Brussels and the International Monetary Fund,” Le Maire told Le Monde in an interview. “The next step is already written: Austerity and massive tax hikes.”

NORINCHUKIN IS CHUCKING $/€ ASSETS: The BoJ’s plans to embark on a yen-denominated-asset dumping spree may be derailed by domestic stresses. One of Japan’s biggest banks, agriculture bank Norinchukin — with $840 billion worth of assets — said on Wednesday it would have to dump about 10 trillion yen ($63 billion) worth of U.S. and European sovereign bonds between now and March next year as it battles bad bets.

Wrong-way risk: The bank first reported it would be restructuring its investment strategy in May, when it predicted “wrong-way risk” on its books would generate up to 500 billion yen ($3 billion) worth of losses in the fiscal year. That figure has since mushroomed to 1.5 trillion yen ($9 billion), according to Bloomberg.

How on earth? In its rush to escape negative rates in Japan, Norinchukin had bet large on European and American sovereign bonds, including collateralised-loan obligations, a position that soured after rates stayed high longer than expected. The bank now needs about 1.2 trillion yen ($7.6 billion) of capital to plug the hole in its balance sheet.

Fed support? Clues that something was going wrong at Norinchukin were afoot as early as December 2023, when the bank first appeared on the Fed’s list of approved counterparties for its standing repo facility. More than 50 percent of the bank’s investment portfolio is in dollars.

Carry trade factor: Eurodollar University’s Jeff Snider says the purpose of Norinchukin’s bond sales come down to two words, and neither are inflation. He says it’s all down to the carry trade and the fact the bank has been forced into a negative carry position. See his full take here.

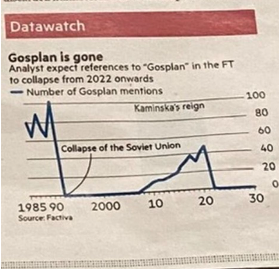

| GOSPLAN |

FROM SHOCKFLATION TO GOSPLAN: Europe’s most controversial command-economy sympathising economist, Isabella Weber — who advocated putting in price controls between 2021-2022 to battle inflation — has been gaining traction in Brussels. In a joint paper written with Jens van ‘t Klooster published this week at the request of the European Parliament Weber argues that interest rates should be abandoned in favour other tools to fight inflation.

According to Weber, it’s too hard to predict when and how rates impact the economy, and they often end up harming market participants indiscriminately, jeopardising key investment objectives, in green energy for example.

Drawing the wrong lessons: In their view, policymakers’ current anti-inflation toolkit dates back to the 1970s. Therefore, it’s overly focused on the threat of a wage-price spiral — broad-based inflation that results when workers flex their labour power to secure pay increases that end up feeding into prices. But, write van ‘t Klooster and Weber, that wasn’t the case with this latest round of inflation, which was profit-led rather than wage-driven. The price spike that is now ebbing away showed up in unit profits, not wages, which in real terms even contracted.

Get with the times: “The European governance framework is only suited to rein in at the conflict stage and not at the impulse or the sellers’ inflation stage of amplification and propagation. At every stage, shockflation becomes increasingly costly to contain,” they write.

The policy prescription: Better equip governments both at the EU and national level to fight inflationary shocks preemptively. That means access to better data so that Eurostat can monitor key prices in real-time and identify issues as they emerge.

Reminscences of Gosplan? Weber says it means creating strategic plans for sectors that are judged as key (Ed — perhaps five years in length?). The authors point to the EU Chips Act as an example of what that could look like, though, competition policy as well as windfall taxes also have a role to play here, penalising firms that take advantage of temporary bottlenecks to price gauge. That word dreaded by economists, “price controls,” even makes an appearance, as a way to “correct the overshooting of prices in response to shocks that induce endogenous price uncertainty [which] can help to buy time.”

Oh, and of course there would be grain collectivisation and silos: Because why wouldn’t there be? As the Guardian keenly picked up, the paper also advocates for the creation of buffer stocks of grain that could be released during shortages or emergencies to ease price pressures. “Literally the worst of times for global hunger seem to be the best of times for the companies managing the global trade in food staples,” Weber said. “It might seem utopian in the current environment, but there is such clear benefit in terms of economic stability that it’s not as utopian as it seems.”

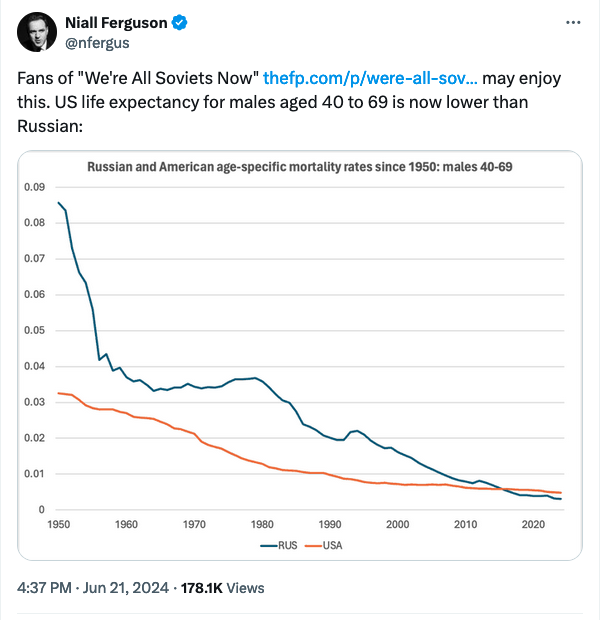

WE ARE ALL SOVIETS NOW: Historian and friend of the Blind Spot Niall Ferguson (now Teflon-coated due to having been knighted) broke the internet this week with a piece proposing not just that we’re all Soviets now, but that we might also be the baddies, as per the famous Mitchell and Webb sketch: Are we the baddies?” While Blind Spot readers will be familiar with the argument, Ferguson’s historical expertise ensures that his rendition of our Sovietisation provides even richer comparatives. Do read the full piece. One of the most important observations in the piece, we think, is the theory that we only have ourselves to blame for it.

Or, as Ferguson puts it: “We also need to contemplate the possibility that we have done this to ourselves—just as the Soviets did many of the same things to themselves. It was a common liberal worry during the Cold War that we might end up becoming as ruthless, secretive, and unaccountable as the Soviets because of the exigencies of the nuclear arms race. Little did anyone suspect that we would end up becoming as degenerate as the Soviets, and tacitly give up on winning the cold war now underway.”

Mortality parallel: Ferguson rightly spends a lot of time comparing the mortality disaster that impacted the Soviet union at its end to that now impacting the US — and the observation has justifiably gone viral.

Just to highlight the value our readers get from subscribing to the Blind Spot, we made a similar observation in our March 25, 2023, newsletter comparing the American fentanyl crisis to Russia’s alcoholism crisis.

| QUOTES OF THE WEEK |

“Investors should be alert to possible challenges to the institutional culture of central banks in 2025,” former World Bank chief Robert Zoellick wrote in the FT this week.

“Gorbachev’s reforms not only faced opposition from senior Central Committee officials and some Politburo members, but even when initiatives were agreed and laws passed they languished due to bureaucratic resistance and outright sabotage by local officials,” — a response from the Gorbachev Foundation by Robert David English on October 2022, to assertions after his death that Gorby was a “quintessential apparatchik”.

| INFLUENCERS |

POLITICO’S LATEST POLL OF POLLS FOR THE UK:

ELECTION CAMPAIGN TACTICS: What’s the big new thing in campaign dirty trickery and shady influence ops? According to the Guardian’s Jim Waterson, anything but personalisation and microtargeting. That means less Cambridge Analytica and more old-school broad messaging and creative sloganeering. Digital strategist Tom Edmonds supposedly told Waterson Facebook had banned political campaigns from using many of the tactics deployed in past contests. “Running a campaign aimed at 500 people didn’t earn them much money and just got them loads of shit,” he said.

Big picture messaging: “Edmonds, who ran digital campaigns for the Conservatives in the 2010s, said this general election would instead be defined by parties spending tens of millions on online adverts designed to reach as many people as possible,” the Guardian reported.

Who’s spending the most? In the U.K., parties have up to £34 million each to spend on campaigning, and thus far it is Labour that’s been spending most online: What’s the blind spot? Labour’s epic online splurge doesn’t seem to have stopped the party losing ground to Nigel Farage’s Reform. They’re still on track for a super-majority, don’t get us wrong, but given the return of back-to-basics campaigning and the ready admission that microtargeting doesn’t even work that well, is Labour missing a trick?

What’s the blind spot? Labour’s epic online splurge doesn’t seem to have stopped the party losing ground to Nigel Farage’s Reform. They’re still on track for a super-majority, don’t get us wrong, but given the return of back-to-basics campaigning and the ready admission that microtargeting doesn’t even work that well, is Labour missing a trick?

Deepfake anxiety: Deepfakes were supposed to cause an election crisis this cycle. And yet, none of these predictions have come true yet. What seems to have happened instead is that the perception that deepfakes may be all around us has made real-world engagement more valuable. There is now more pressure on candidates to get out and about in communities directly, and to be seen on old-school media. And it’s at that sort of stuff that someone like Nigel Farage excels, not just because he’s had his own radio show for years but because, unlike most politicians who only go on “I’m a celebrity” to rebuild their credibility after they’ve been disempowered or disgraced, he had the wisdom to do that show pre-emptively last year. And he came second.

There’s something about Nigel? Nigel has been saying there’s something traditional polling isn’t capturing, something he will be taking advantage. Informed voices say, on the polling side, don’t be surprised if he’s proven right.

Don’t completely dismiss microtargeting. Sources close to Cambridge Analytica tell the Blind Spot that when it comes to commercial microtargeting, there are thousands of firms doing exactly what Cambridge Analytica was doing. “That’s the irony of the whole thing,” the source said…”When the scandal happened what we were doing was perceived to be the work of the devil … now almost every leading digital agency is driving their targeting and engagement in creative data. It’s just become the rule of thumb now.”

THE ANTI-FARAGE OP HAS BEGUN? Farage claimed on Saturday that Google had blocked Reform’s ad accounts to stop their message getting out, calling it election interference. But who is really playing who? Consider the following time line:

— Nigel Farage causes a media storm telling the BBC’s Nick Robinson that European expansionism provoked Putin to attack Ukraine.

— The establishment brings out the big guns to denounce Farage, starting with Hamish De Bretton Gordon, followed by Christopher Steele, Jon Sopel, and John Simpson.

— George Galloway speaks up for Farage.

— In a curious case of “pre-bunking” the story in Nigel Farage’s favour, it emerges that a clip of Jeffrey Sachs “educating” Piers Morgan about who really baited who in Ukraine goes viral 24 hours before Farage’s interview.

— Donald Trump, meanwhile, also comes out with a similar line about Ukraine at exactly the same time.

— Another clip goes viral showing Farage in April 2014 asserting that the establishment’s push for Ukraine to join the EU and Nato, would be seen as a deeply provocative act by Putin and would give false hope to the Ukrainians. “They actually toppled a democratically-elected leader, yes I know Ukraine is corrupt, I know it isn’t perfect but they toppled a leader,” he says in the clip before concluding an expansionist EU project will be a danger to peace.

— And here’s Gorbachev in 1997 on Nato expansion. “I believe it’s a mistake, it is a bad mistake and I am not persuaded by the assurances I hear that Russia has nothing to worry about. You can not humiliate a nation, a people, and think that it will have no consequences. So my question is, is this a new strategy?”

BOTTOM LINE: Whether you love him or loathe him, it never pays to underestimate Nigel Farage. Just like with Trump’s lead getting stronger in the polls with every arrest, the blind spot is thinking that Farage’s supporters will be discouraged by media scare stories about him.

READ ALL ABOUT IT: CHEAP FAKES! All those videos you’ve been seeing of Joe Biden online where he appears cognitively impaired or physically constrained: they’re cheap fakes. Got it?

That at least is the official White House line on a viral clip of Biden in which the US President appears to stall, needing help from former President Obama to be escorted off stage. “It tells you everything that we need to know about how desperate Republicans are here,” White House Press Secretary Karine Jean-Pierre told reporters, labeling the clips “cheapfake” videos.

Disingenous defense? Donald Trump is no poster child for cognitive capability. There’s little doubt about that. But rebranding “selective editing” — an everyday occurrence in media all over the world — as a sinister “cheap fake” attack, has its own manipulative agenda too. The term has obviously been concocted to trigger a deepfake word association in people’s brains on a subliminal level, much the way the peddlers of fake goods try to dupe us into thinking their goods are real by slightly misspelling a major brand name.

Blowback potential: Selective editing has been de rigueur in media ever since television was invented. It is certainly misleading, as this famous Guardian ad spells out, but it’s not the same as a fake. The blind spot here, we think, is the inadvertent blowback that the rebranding of selective editing as “cheap fakes” will have on overall trust in the media. As we know, the term fake news has become common parlance for media bias and propaganda — with both sides deploying it liberally to the detriment of viewers and readers, who are just being conditioned that there is nothing balanced or unfake out there. The problem with the cheap fake “selective editing” slur isn’t just that it now justifies Trumpian claims that he is continuously being clipped out of context, but that it can also be applied to almost all media edits that purposefully make people look better on screen than they do in real life.

Nothing new under the sun: But none of these deceptive tools are new. Making a thing of them being a thing now, only risks eroding more trust.

Cheapfake origins: In case you’re wondering where the term originates from, it seems to have been coined by a couple of disinformation academics in 2019 in a study funded by Data and Society, a left-of-centre think tank “that promotes censorship of online speech and applies critical race theory to technology issues” that has received funding from among others the Ford Foundation and Open Society Foundation.

| OPEN TABS |

— China plans new measures to attract venture capital investment (Bloomberg)

— Chinese president told European Commission president that Washington was trying to goad Beijing into war (FT)

— Keir Starmer does lunch with the FT (FT)

— Danes are told to stockpile water, food, anti-radiation iodine pills for possible Russian crisis (HNGN)

| SPY CRAFT |

THE STARMER FILES: The Daily Mail went big with a story about how aspiring PM, Labour leader Keir Starmer, ended up in Communist spy files after joining a Czechoslovakian work camp at the height of the Cold War. The key line was: “The Czechoslovak secret service was using these camps to gather information on bright and idealistic young people in the hope that one day they might be of use to them, one way or another.”

SNOWDEN FLAGS OPENAI’S NSA LINK: NSA whistleblower Edward Snowden shared some strong feelings on X about the appointment of retired US Army general and former NSA head, Paul M. Nakasone, to OpenAI’s board of directors. “Do not ever trust @OpenAI or its products (ChatGPT, etc). There is only one reason for appointing an @NSAGov Director to your board. This is a wilful, calculated betrayal of the rights of every person on Earth. You have been warned,” he stated.

SPIES IN CANADA: One of the world’s most stable democracies was gripped by growing panic about foreign agents working in elected office, Politico reported. According to a bombshell report by Canadian lawmakers, unnamed politicians have been covertly working with foreign governments. “The new report from the National Security and Intelligence Committee of Parliamentarians is the first to suggest that lawmakers in Canada’s parliament may have helped foreign actors meddle in political campaigns and leadership races. Heightened anxiety in Ottawa about foreign interference comes in the middle of historic global elections where factors such as artificial intelligence and emboldened foreign powers are testing the resilience of democratic systems,” Politico noted.

| CRYPTO |

MAR-A-LAGO BRETTON WOODS: Following a high-level meeting with crypto’s most influential miners at Mar-A-Lago over a week ago, Donald Trump has reportedly come over all pro-crypto. The meeting was allegedly organised by Bitcoin Magazine’s David Bailey and the discussion centred on the potential pathway for the Fed to get involved, among other things. No specific promises were made, but it certainly hasn’t hurt Trump’s standing in the crypto community. Crypto promoters Cameron and Tyler Winklevoss tweeted on Thursday they had each donated $1 million in bitcoin to the Trump campaign.

DJT MEME COIN FRENZY: Somebody created a DJT-themed Trump Coin on Solana a week ago, and its value mysteriously soared 385 percent within 24 hours achieving a valuation of $363 million. The scale of the move triggered a furious hunt to expose the creator of the coin, with speculation mounting that a Trump family member could be involved. Eventually, all roads led to the unexpected figure of Martin Shkreli, the former disgraced pharma investor who served time for securities fraud. He then popped on a Mario Nawfal spaces chat to explain all, claiming that he had been asked to create the coin by Donald and Melania’s Trump’s son, Barron Trump, and that only he had the coin. The valuation of the coin has since collapsed.

| GEOPOLITICAL HOT SPOTS |

URI GELLER SAVES ISRAEL. The psychic Israeli spoon-bender told GB News he had played a key role in helping Israel defend itself from Iranian missiles back in April, but he couldn’t offer more details as the work was classified. He also warned Britain that any attack by Hezbollah on British bases in Cyprus would inevitably drag the United Kingdom into war in the Middle East.

DARIO COMMENT — Only a miracle has stopped Israel vs Hezbollah attacks from spiralling into a full-blown war, a senior US official said when responding to the escalating situation on Israel’s northern border with Lebanon. American officials outlined their concern not just at the threat of continuous escalation, but also questioned whether the IDF has sufficient anti-air reserves to effectively counter the large barrage of available long and medium-distance weaponry Hezbollah has at their disposal.

News and concern about the continually ongoing escalation in northern Israel, with Israeli outlets claiming they have repositioned certain divisions to the Galilee region to prepare for a potential assault into Lebanon, have coincided with long-range strikes on Israeli ports.

In the last few weeks, the Houthis struck ships in the Israeli port towns of Ashdod and Haifa, alongside Hezbollah strikes targeting ships anchored in Haifa port. This comes after reports on June 3 that Houthi missiles struck targets in the southern Israeli port town of Eilat.

That these militias have the capacity to threaten Israeli security, as well as their food security (imports and shipping) with rudimentary rockets —even if this threat can’t be sustained for long — goes to the heart of strategic vulnerabilities in Israel that practically guarantee its implosion in the decades to come.

The core of this problem is that no matter how technologically advanced Israel may be, it suffers from a lack of territorial extension and from a total numerical disadvantage. In the first instance, the big problem is that it remains within easy range of its enemies.

Israel’s claims that it should move the conflict north to ‘destroy’ Hezbollah are disingenuous at best and total misinformation at worst. If it couldn’t destroy Hamas in a thin strip of land, a little mouse in comparison to Hezbollah’s power, it stands absolutely zero chance of denting Hezbollah’s well-established, state-like power in Lebanon.

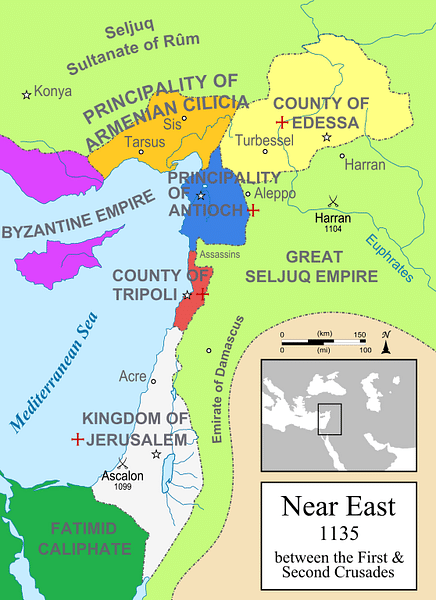

While many have pointed to Israel’s presence in the region as historically unprecedented, and quite distinct from the traditional growth of states worldwide, history begs to differ. There were very comparable states with near-identical core problems only a few centuries ago: the Crusader States.

Similarly to Israel, the Crusaders held significant technological superiority over their Arab foes. They had immensely superior siegecraft, with trebuchets and catapults, as well as centuries of experience honing the European art of fabricating impregnable castles — something the Arab forces sorely lacked. They were also at a distinct numerical disadvantage to the Arabs, with extremely long supply chains to their European homelands.

Similarly to the Arab counterparts to Israel, the Arabs of the Seljuq and Fatimid caliphates suffered from decades of internal and external inter-Arab squabbles that meant they hardly ever managed to unite their forces for long enough to defeat the numerically inferior Crusaders until the arrival of Salahuddin, who united the Arabs and quickly expelled most Crusaders from the Levant.

The most critical aspect of comparison between the two states is how the majority of the Crusader and Arabic aristocracy, and their respective extremists, viewed each other. As is usual in history, the middle and upper classes in most states will opt for peace over war — regardless of cultural differences. This allowed for the relatively rapid expansion of peace initiatives between both sides, and the enactment of much-needed, and sought-after trade routes connecting the Silk Road to European markets. But unfortunately for both, the extremists didn’t let it happen.

Crusader orders like the Knights Templars and Hospitallers would often go on unauthorised raids deep behind Arabic lines, forcing the Crusader Kings to respond once the Arabs would aggressively react in kind. In many ways, it was the behaviour of these extremist fighting sects that doomed any chance of long-term peace between these two ostensibly opposed factions, rather than any inherent problems existent between their respective Christian and Muslim elites.

This is a brutally simplified perspective and comparison with the Crusader states, but it makes for a good point: extremists on both sides are interested in sabotaging attempts at an enduring peace.

Taking from the excellent Israeli documentary “the Gatekeepers”, where all the former heads of Israel’s Shin Bet — its internal intelligence agency (an MI5 equivalent) — joined together to denounce Israel’s current security policy. The quote “one man’s terrorist is another man’s freedom fighter” reverberated throughout the documentary, as these experts in security scratched their heads at how exactly cross-border raids into Palestinian homes could ever result in a safer Israel. Instead, every killed or arrested Palestinian, every demolished home, goes further in guaranteeing Israeli insecurity. The documentary also reviewed how the extremist right in Israel has consistently managed to sabotage peace attempts by the Israeli liberal center and left, including in the assassination of Israeli Premier Yitzhak Rabin following the signing of the Oslo Accords.

The same thing can be said for the extreme wings of Palestinian political opinion — a viewpoint that has only become more popular since October 7 and the Israeli onslaught in Gaza — with support for the two-state solution in the Palestinian territories dropping like a rock.

Once we accept the historical likelihood of the power held by extremists on both sides, and their encouragement and interest in creating and continuing a state of war, we get into Israel’s main problem: arithmetic. While there are 9 million Jews and only 2 million Israeli Arabs in the territory of Israel, that’s where the pro-Israeli arithmetic ends. Because of this numerical disadvantage, like the Crusader States, Israel’s only hope for long-term stability is in securing a viable peace agreement with the Arab populations it is surrounded by.

Unfortunately, the more the country is held in the grips of the “security”-oriented Netanyahu government, and his outsized military actions continue to be a rallying cry for Palestinian extremist organisations, the less likely this becomes.

The same mistake will likely be made should the conflict extend further to the north. Going further than the incredible Hezbollah recruitment and political campaigning tool such an Israeli invasion would become, Israeli invasions of Lebanon have usually become the graveyard of Israeli governments (and their armies). The Israeli intervention in Lebanon in 1981 — arguably the only successful of the two Israeli invasions — directly led to the end of the Ehud Olmert government that authorised it. Similarly, wide media coverage of the vast number of casualties being suffered by the Israeli army during its second and far more mediocre intervention in 2006 led to a widespread Israeli outcry against the war that ended in a haphazard and rushed Israeli withdrawal from Lebanon.

Western supporters of Israel should bear this pessimistic but realistic position of Israel in mind when they spout the traditional pro-Israeli viewpoints that rely on military action for peaceable political outcomes. Unfortunately, this Israeli policy is arguably the most anti-Israeli policy there is — something many Israelis are well aware of since tens and hundreds of thousands have been marching for a peace agreement with the Palestinians in exchange for hostages every Saturday for months now. In fact, a new survey for April found that 62 percent of the Israeli public prefers a peace deal to release the abductees over more military action in Rafah.

In an ironic twist of fate, therefore, supporters of Israeli military operations — particularly diaspora Jews and neoconservative/liberal Western elites, unaware of the intrinsic weaknesses of the Israeli state — may be the ones ensuring Israel’s eventual destruction.

| LAWFARE |

SOVEREIGN IMMUNITY UNDER THREAT? EU nations are among governments facing legal charges from investors that are using international court mechanisms to target their assets, a fascinating oped by Charles McKeon, director and co-founder of litigation PR firm Thorndon Partners, noted in Politico last week. He noted that ongoing attempts to enforce an international court judgment in London against the Spanish government — which is claiming sovereign immunity — are likely to be pivotal.

DARIO COMMENT — London may become the European capital of state-owned asset seizure as Madrid’s appeal to halt the seizing of its state-owned land in the United Kingdom was refused by a London court.

The consequences of the Ukraine-Russia war and the recent extraordinary step taken by Western governments in seizing $50 billion in frozen Russian assets and using them to underpin loans to fund Ukraine’s reconstruction and war efforts have gone far beyond any impact on Russia.

Unsurprisingly, such a step is risks permanently damaging states’ ability to claim sovereign immunity, setting a precedent for state-owned property to be seized and used at will. Unfortunately for myself, my home country of Spain seems to be the first in line to suffer these consequences.

But the story is not directly related to the seizure of Russian state assets. Instead, the claim is part of a World Bank international arbitration decision against Spain which demonstrates that Russian state asset seizure is only a part of an ongoing parallel process that is stripping states of their sovereignty and legal superiority over private corporations in the West, particularly in Anglo Saxon countries.

Over 50 investors sued Spain for a total of €8 billion in damages after its government changed tack on incentives to stimulate its burgeoning renewables sector in the mid 2000s, with the investors claiming Spain breached its Energy Charter Treaty obligations.

Spain, naturally, refused to pony up to these investors claims, whose recent court wins have recently entitled them to around €2 billion and counting from the Spanish government. As a result, two educational and cultural institutions belonging to the Spanish state in London have been subjected to court orders that allow investors to seize the underlying land to repay Spain’s debts.

Spain tried to deploy its “sovereign immunity” argument to deflect its arbitration debts from being enforced in the United Kingdom, an argument rejected by London’s high court. Its arguments ran into a not-too dissimilar ruling in the United States, where its courts gave an ambiguous ruling on whether it can rely on this immunity. An Australian High Court also unanimously dismissed Spain’s appeal and ruled in favour of the aggrieved investors.

This has made the UK more attractive to investors seeking to enforce judgments, especially since this ruling against Spain confirmed that arbitration decisions made inside the EU — “intra-EU” — can be formally recognised in the UK, leaving other EU nations guilty of breaching the Energy Charter Treaty of similar seizures by London courts.

As a Spaniard, the concept of Britain becoming the haven for corporate raiders and pirates, siphoning public funds for private gain from sovereign countries, doesn’t come as a surprise. Read into the comments section of any slightly right-leaning Spanish media outlet covering the UK and you’ll find the top comments all read any version of “these damned pirates”. It may be almost have a millennia since Sir Francis Drake stole Spanish bullion, but the Spanish haven’t forgotten any of it.

The greatest irony of all is that I may have played a small part in this outcome. Within my first week at Kroll, a more experienced analyst dropped a case regarding a potential seizure of Spanish state property on my desk. He was trying to leverage my Spanish expertise, and I complied. I used my knowledge of the web of Spanish institutions to compile an extensive list of land registry records owned by Spain and sent the information back over. It took me less than two hours. While funny feelings of traitorhood abounded, I reassured myself that sovereign state property couldn’t be seized by foreign corporations. How wrong I was!

Irrespective of whether my small Judas-like moment had any real impact or not, arguments of the immutability of state sovereignty go to the heart of political thought. One is reminded of Thomas Hobbes’ famous exhortation in the Leviathan – that the all-powerful ruler of a hypothetical state’s laws should cover everyone and everything, but not himself. Since he enacted the laws, being their fountain, he must naturally be above them. And this goes further into well-known territory for The Blind Spot – that such a sovereign must effectively retain its ability to call for a state of exception: that the sovereign is the only one with the power to up-end its own system.

So what happens when a sovereign denies another’s sovereignty? We are accustomed to this occurring in war conditions — where such seizures of assets and property are legally understood. But if a foreign state can claim there is an exception to one state’s sovereignty and treat it as a private entity that is under the law without a state of war, could we be looking at the end of sovereign statehood?

If this ruling and Western actions on legally sovereign assets of the Russian state is anything to go by, the answer is yes, we are. It’s foreseeable that this could have two consequences. The first is the existence of a supra-sovereign legal parameter in Anglo-Saxon capitals which allow them to demolish other state’s sovereignties. Without sovereignty, states are effectively reduced to being treated like large private corporations. In so doing, I could see how this will be removing the legal impediments for private corporations to arm themselves like states, creating a re-flourishing of private armies like the East India Company once more.

The second would, presumably, be the friend-shoring consequences of such a move. Would foreign countries be as willing to support investment or have a presence in countries that, effectively, do not recognise them as equals?

While we are not experts in this subject, and cannot read the future, it’s worrying to know the erosion of state sovereignty that two years ago was written on as the ‘unintended consequences of Russian state asset seizure’ has already materialised. The final irony is that its first victim, Spain, an EU and NATO member, signed off on effectively the same argument that will doom its legal efforts to defend sovereignty.

| TLDR |

WHAT WE HAVE MARKED FOR READING OR WATCHING LATER:

— Jeff Snider explains the Norinchukin carry trade.

— Two RUSI papers on the latest goings on with FATF, one on the weaponisation of FATF standards by authoritarians, the other about using the FATF as a fig leaf to target civil society.

— The entirety of the Isabella Weber Gosplan paper.

— The ECB on how banks deal with declining excess liquidity.

— The ECB on home bias in repo rates.

— The full G7 communique.

— Macron’s full Sorbonne speech.