")

Today’s Spot Markets live session is with Anjuli Davies, formerly of the Telegraph and Reuters, Davies’ last posting was as Senior City Editor for the Telegraph, moving there from her role as Acting Chief UK Financial Correspondent for Reuters. We also have a fly-by from Tom Hayes, the former UBS rates trader who was sentenced to 14 years in prison for dishonestly driving manipulation of the Libor market, on the back of news that US courts have now thrown out charges against him.

Comments addressing audience statements are in bold.

Izabella Kaminska 11:57

Izabella Kaminska 11:57

Hello and welcome to today’s spooktastic Spot Markets Live.

Happy Halloween…

We are having a Halloween party tonight so I have a very excited four-year-old on half-term in the house.

Today I’m joined by Anjuli Davies.

Hello Anjuli! How was half term?

Anjuli Davies 11:59

Anjuli Davies 11:59If I never see another pumpkin again….

Slightly disappointed we won’t be discussing a Halloween budget this morning.

Izabella Kaminska 11:59Yeah, quite.

Anyway, let’s crack straight on with what’s going on in markets/finance etc.

The big news over the weekend is obviously Elon finally taking over Twitter and bringing a kitchen sink with him on his first day.

He’s now floating all sorts of ideas about how to better regulate speech on Twitter, and some of those ideas seem to align with ideas I want to pursue for how to better organise journalistic resources.

But that doesn’t mean I am evoking Elon! (as some people on Twitter are suggesting) Quite the opposite.

I think it’s important this is all led by journalists from the bottom up. Anyway, we will be discussing all these issues at 1 pm UK time in a dedicated Twitter Spaces session

Do join me if you’re interested.

Anjuli, where should we start?

Anjuli Davies 12:01I saw you were getting it in the neck a bit there Izzy… anyway, how about the LIBOR CASE.

Izabella Kaminska 12:01There’s been big news here.

The BBC’s Andrew Verity has just put out a piece reporting that The United States has thrown out criminal charges it brought against the first trader to be jailed for “rigging” interest rates.

Anjuli Davies 12:01That’s former UBS trader Tom Hayes, who was the first of 38 people to be prosecuted.

He actually spent time in prison for this.

Izabella Kaminska 12:02It was definitely a sizeable chunk of time.

I think maybe 5 years?

I have a lot of thoughts about this case.

It’s another example IMHO of what’s currently wrong with journalism.

And a good example of what happens when the media gets swept up in a singular “virtue signally” narrative.

Around 2010-2012 there was only one permissible angle on the topic.

The system had just gone through a major crisis, and the public wanted scalps. Libor traders were the ones in the dock, and there was huge political pressure to deliver some bodies.

Nobody really cared about the details.

Anjuli Davies 12:03Let’s face it, who in the general public even understood what Libor was? It just became a symbol of a rigged system and the public needed scapegoats.

Izabella Kaminska 12:04Also, the case was incredibly complex and full of jargon, and mostly beyond the capacity of most people who don’t operate in finance to understand.

You covered this right? What were your thoughts at the time?

(@bruce we can def talk battery minerals)

Anjuli Davies 12:04I was at Reuters at the time and I took turns sitting at the trial and reporting what was said.

Not just Hayes’ trial, but the Barclays guys as well. It was an incredibly difficult trial to follow and report on… a lot of decimal points to describe, but I did feel really like there was an injustice being done.

It was evident that everyone, I mean everyone from the CEOs to the Bank of England knew exactly what was going on and in a way perhaps it was justified for the sake of averting financial Armageddon at the time…but it was just too convenient to look back and point fingers at the guys trying to hold it all together.

Also, there was a lot made of some of the more salacious details about drinking cultures and big spenders which was a way to paint bankers as bad/arrogant/rich.

Izabella Kaminska 12:05That’s quite right.

I was just a lowly FT Alphaville reporter at the FT at the time.

I know this may sound retrospectively self-serving, but I think you won’t be surprised to hear that (as usual) I wasn’t convinced by the prevailing narrative.

I would have many discussions internally about this with people like Lisa Pollack, who had come from the industry and understood the mechanics really well, but the focus at the newspaper was very one-directional — it was hard to push back in writing.

It wasn’t really until the FX rigging cases that I felt I had enough internal authority to put anything in print…

.. and even then it was mainly only because Matt Levine had questioned some of the bandwagon thinking on the whole thing.

Here’s an example:

How did you find it?

Anjuli Davies 12:08Well at Reuters, we had hired the WSJ guy who basically broke the story – I think his name was Carrick Mollenkamp. So there was a huge drive to identify all the individuals involved and break out details etc.

Izabella Kaminska 12:08RIght. Btw do let us know what you think so we don’t stay in our bubbles.

I met Andrew Verity at the LBMA conference a couple of weeks ago.

He has done an amazing job at the BBC drawing light on the judicial malpractice here.

I don’t want to speak for Andrew, but we did share thoughts about these sorts of stories coming out in spite of editorial management, not because of.

The issue really is that even if what the traders were doing could be perceived as morally questionable, it was not illegal.

More than that, it was de facto sanctioned by the norms of their employers.

Do check out his podcast:

Even more striking is the fact that the BoE knew about what was going on, and happily leaned into similar practices to achieve rates that suited it.

Personally, I think the manipulation encouraged by the BoE was far more systemically impactful and dangerous than the profit-motivated manipulation conducted by the traders until then.

Anjuli Davies 12:10@Darren, yes there were many meetings with the legal team.

Izabella Kaminska 12:10The BoE gave a false impression of what the cost of funding was. It was an act of market suppression.

And rather than “solving” the crisis, it arguably fed the imbalances even further.

Of course, it does get tricky.

It’s easy to argue the BoE does have the mandate to influence market rates.

What is QE if not overt rate market manipulation?

Anjuli Davies 12:11And as Bruce says, name a market it’s not happening in.

Izabella Kaminska 12:11Quite.

But the issue, for me, is doing it in a way that is not transparent. Though again, complexities here as the BoE has I guess a right to obscure its actions to help calm markets.

It’s one of those moral ambiguities.

Anjuli Davies 12:12The problem is, it emerged that a lot of money was made on these “manipulations”, and that’s what didn’t go down well. The fat paychecks and the big bonuses.

Izabella Kaminska 12:13Yeah. And the optics of that were the problem.

Anyway, Tom Hayes was engaging with me on Twitter earlier. And has agreed to do a podcast with me – so we will try and arrange a leaked lunch with him asap.

Have invited him to SML too, not sure if he’s made it though.

I think based on our prelim convo, he is being incredibly stoic about what’s happened to him.

And agrees the system was terrible and inherently full of conflicts of interest…

Fascinatingly, he isn’t too angry about the media reaction. Kind of sees the hysteria as the inevitable consequence of the fact that no one on the trader side was able to speak to the press early on.

And I guess that is what’s hard in such situations. The people being accused are often unable to give their side of the story.

So it will be very interesting to hear from him.

Anjuli Davies 12:18The thing with the Libor saga was that there were two distinct periods.

The pre-Financial crisis, business as usual, and then then the near death of the banking system when it all emerged.

The BBA had warned about libor setting in 2005

Hi Tom!

Izabella Kaminska 12:19Speak of the devil – hello Tom

🙂

Tom Hayes 12:19Izabella Kaminska 12:19

Tom Hayes 12:19Izabella Kaminska 12:19Thanks for joining us, would be fascinating to hear your take on all this.

Anjuli Davies 12:20Thanks for joining us, Tom. So what are your thoughts, what questions should we now be asking?

Izabella Kaminska 12:20@Tom – and yes, I’m very interested in your take on the media response and what we can do as journalists to make sure this sort of stuff doesn’t happen again.

Tom Hayes 12:24Hi all!

Anjuli Davies 12:22Bob Diamond was at least a sort of sacrificial lamb

Tom Hayes 12:24Ok so as I was saying we were told to not talk to the press and that was a major problem

It allowed the narrative which followed the zeitgeist of the time to take hold

And politically it was convenient

Anjuli Davies 12:25It’s always good to have a friend who is a journalist…

Tom Hayes 12:25I worked in JPY in Japan.

And I should have been prosecuted there!

I had nothing to do with the U.K. or the USA.

But UBS used me adroitly to minimise fines and management exposure.

Initially, the SFO sent it back to the FCA in 2011.

But when it looked like the DoJ were going after lowballing they had to seize control of the investigation.

Compare Libor prosecutions in the U.K. to the way the SFO dropped the FX stuff.

I wasn’t an angel but I wasn’t a criminal and all my actions were known about by many layers of management.

Izabella Kaminska 12:29Right exactly. And I get your point about jurisdictions. Though wouldn’t it have been worse being prosecuted in Japan (basing that assumption on Carlos-Ghosn?)

Tom Hayes12:30Well firstly, Japan relies on codified rules

Anjuli Davies 12:30Tom – have you read any of the books written about you/Libor out of interest? The Fix and The Spider Network?

Tom Hayes 12:30Secondly, the hierarchy there means if your managers know then you are in the clear.

They didn’t even sanction me on a regulatory basis.

Izabella Kaminska12:31Good point about the hierarchy. In fact, that explains the Carlos issue.

Tom Hayes 12:31Lastly, their system of justice relies on the concept of shame

I lost my job

I was publicly shamed.

They were actually very bemused by what happened in Anglo-Saxon countries

And reasoned it was due to anger over the GFC.

Izabella Kaminska 12:33Yeah, this is the issue. How long did you end up spending in prison?

Tom Hayes 12:335.5 years mostly in high-security prisons sharing cells with murderers.

Izabella Kaminska 12:33This is exactly the opposite of innocent until proven guilty, and the idea that justice is blind etc. Really very sad. And I for one feel very strongly that the media would do it all again.

Tom Hayes 12:34I’m watching the case of Lucy Letby.

And the condemnation is insane.

I just read a piece from the royal statistical society about the use of statistics in medical cases.

The public doesn’t understand p numbers and you get cases like Sally Clarke which results in awful miscarriages of justice.

Who sadly died after being freed

Izabella Kaminska 12:36No idea about that, and in the interest of not talking about stuff I don’t know about it I will share a story about something I do know about.

I am also in touch with Kweku Adboli. I’ve always been very open-minded about his take on the whole affair. There was a point when Alphaville was hoping to hire him in a frank Abagnale manner, to help inform about wrongdoing in markets.

A couple of high-level editors felt we should help him avoid extradition back to ghana, and his being employed by the FT would have helped his case.

So we spent some time trying to get him involved, and there was a general fear that UBS would take it the wrong way.

Tom Hayes 12:37Yes, I don’t know about Kweku but I do know about UBS.

I wish him luck as whatever the case I don’t think his story has been properly told.

Izabella Kaminska 12:37There was a very animated internal discussion about it. Some people thought the optics would be terrible, and it would compromise our access to UBS.

Tom Hayes 12:38This is what I mean the banks are so so powerful

Izabella Kaminska 12:38I can host Kweku one day too maybe. But I know he also feels like he was scapegoated.

Tom Hayes 12:38They ran the investigation by the SFO into mine. And had total control of disclosure. Hid exculpatory evidence – I can prove in my case they lied to the regulator and Court.

So great question on different desks Libor exposure. Generally, the exposure is greatest on derivative desks, but even then internal funding has a big impact on treasury desks.

UBS nicely solved this by having a spreadsheet where everyone put their exposure – aggregated it and then shaded the submission.

Of course not for yen! Hence the evidence against me. I was the spreadsheet. Actually my requests only correlated to my own book’s exposure 53% of the time. My requests represented my desk’s net exposure – and were often ignored by the cash desk if they were the other way round.

My plans tend not to extend beyond tomorrow, I just have so many uncertainties.

I have to go to speak to the Times now.

But I’ll pop back in the future, was lovely chatting!

Izabella Kaminska 12:38@Darren – I’ve always been very impressed by Kweku’s conduct, tho UBS spun that as “you see! He’s so charming, he’s such a great conman!”

Thank you Tom!

Now, it’s worth just looking at a few other stories before we finish.

The pound still likes the Rishi news, and my ‘standwithGBP’ trade is still looking solid.

Izabella Kaminska 12:40

Over in NY Fed swap spread news, the Swiss have finally fallen off the system:

This is likely related to the news that the Saudis have come in to prop up the bank by buying a 9.9% stake.

Here’s CNBC on the matter:

The chairman of one of Credit Suisse’s newest and biggest shareholders called on the beleaguered bank to deliver a swift overhaul and return to a “very stable, conservative Swiss banking posture.”

Saudi National Bank, the kingdom’s largest lender and majority-owned by the Saudi government, announced Wednesday that it was investing up to $1.5 billion in Credit Suisse — representing a stake of up to 9.9%.

“We got it at the floor price. I think the bank has been battered,” Ammar Alkhudairy told CNBC’s Hadley Gamble on Sunday. “It’s trading at less than a quarter of book value, of tangible book value, which is, which is a steal. And it’s 160-year-old brand, the brand has a lot of value.” The bank is reportedly set to become the second-largest shareholder of Credit Suisse, second to Harris Associates.

Any thoughts Anjuli?

Anjuli Davies 12:41The Saudis are buying up everything? Aren’t they also the second largest shareholder in Twitter…which begs the question about all its free speech expectations …

Izabella Kaminska 12:41Good point. Not exactly known for protecting the rights of journalists.

Over in Europe though, the inflation pressures are persistent.

Italian inflation surged in October. But now we have broad European Consumer Price inflation also “surging” again, overshooting expectations:

*EURO ZONE OCTOBER CPI INFLATION RISES 10.7% Y/Y; EST. 10.2%; PREV. 9.9%

Anjuli Davies 12:41

Anjuli Davies 12:41Have you seen the video of Christine Lagarde saying inflation “came out of nowhere”?

Izabella Kaminska 12:41Yes, it’s hilariously outrageous. Here it is:

Click on the link for the full spectacle

Can I share a sneaky plausibly deniable story from FT days.

For example, I cannot confirm or deny whether heavyweight names occasionally do off-the-record briefings with select managing editors/journos in bulk form.

I also cannot confirm or deny if I’ve ever attended such meetings, where such heavyweight names – especially ones with a penchant for wearing scarves – are mostly gently challenged on issues of the day, on account of the journalistic body collective being largely overly grateful for the special access they are being given.

Last, I cannot confirm or deny if at such meetings certain heavyweight names may have ever expressed that they were more interested in investing time in learning German rather than in learning about how repo markets actually function.

For which they largely depend on other heavy-weight names to inform them on.

Anjuli Davies 12:43sycophancy at its best…

Izabella Kaminska 12:43These things may or may not have happened.

@anjuli didn’t you always have to book Lagarde for CNBC slots when she was the finance minister of France?

I remember her being ridiculously over-available.

Anjuli Davies 12:44Yes, and chase her around at all the Ecofin meetings in Brussels.

Izabella Kaminska 12:44Anyway to round off the inflation news: ECB’S VISCO: RATE RISES MUST CONTINUE IN ORDER TO REDUCE THE RISK OF PERSISTENT HIGH INFLATION.

Izabella Kaminska 12:46@bruce are you giving mdm Lagarde the benefit of the doubt?

It’s been great of Tom to join us. What I still want to know, is how has the judicial process into this impacted the regulatory reform of the market? And what are the blind spots in the new structure? Do we need this excessively complex framework they have now created?

Hopefully we will have him back some day to answer that question

Thanks again for the flyby Tom!

Let’s move on to some other stories quickly then.

Somewhat related but not related.

News circulating that Elon is wanting to charge for Verification on Twitter to help monetise the business.

Is this a good or bad thing?

For context, I’ve been on Twitter since 2009.

For the entire time I was at the FT I resisted being verified as very early on I just felt there was an incredible one-upmanship associated with the whole thing.

I felt it tiered the system.

But after becoming independent, I realised that my engagement and follower build-up was suffering from not being verified.

So, I finally capitulated and decided to go for it. I was finally awarded the prestigious blue tick about a month ago, and yes. It really has made a difference.

Also for those you don’t know, being verified opens the door to a special Verified only tab which normal users don’t get – see that on the right:

Anjuli Davies 12:50

Anjuli Davies 12:50I got the blue tick quite early on, it was very simple at the time, you just needed to fill out a form proving you worked for an organisation.

Izabella Kaminska12:51There’s a lot of pushback about paying for verification, but I actually don’t think it’s that bad an idea.

For verification to be done well, it can’t be a charity system.

Anjuli Davies 12:51I think it’s the opposite, unless you’re not an A-lister, you might benefit from it.

Izabella Kaminska 12:51Also, there should be some sort of mechanism to ensure that legacy verifications that don’t really count anymore (because people have left organisations) don’t persist eternally.

It really depends on the mechanism by which you get the verification.

Independent or via your institution.

Anjuli Davies 12:52I’d definitely be booted out then.

Izabella Kaminska12:52Concern that this will make it too expensive for independents or academics is fair enough.

But that’s why you need an “innscribers” [SELF PROMOTION ALERT] type model to help filter and rank verification rights.

I see the problem as very similar to the Nanny problem.

In fact, I had a long conversation with the CEO of Bubble, Ari Last about his app Bubble, to see what I could learn from him about how he has tackled the problem of adding trust to the nanny market.

[Parents in the room, if you don’t know Bubble shame on you. It changed my life in the early days of parenting, before you have school networks to depend on]

Nannies have to pay for their own DBS checks, qualifications, and verification documents. I don’t see why, if nannies have to do it, journalists shouldn’t!

Anjuli Davies 12:53But unlike independent journalists, employers cover nannies’ insurance, sick pay, NIS, and holiday pay….

Izabella Kaminska 12:54Depends on the type of nanny. The floating nanny ones either work for themselves or are fully employed by parents. But I still think the analogies are very similar.

Anjuli Davies 12:54Not that I want Musk to dominate the session but an interesting story this morning from the FT, on Tesla and Glencore holding talks on a minority stake sale. It’s been mooted before that the auto companies might want to get in on the source of natural minerals so in demand at the moment, so could it be a when not an if with one of the other automakers…

Izabella Kaminska 12:54That is actually very interesting.

Anjuli Davies 12:55Sources close to the matter told Financial Times that Tesla and Glencore held preliminary discussions last year. Talks between the company continued until March 2022. Glencore’s chief executive Gary Eagle visited Tesla’s Fremont Factory in March.

Tesla planned to buy a minority equity stake of 10% to 20% in Glencore but the two companies were not able to reach a deal. The EV manufacturer had concerns over Glencore’s compatibility with Tesla’s environmental goals.

Izabella Kaminska 12:55I still find it funny that nobody had really heard of Glencore at all in financial markets until 2009.

But yeah, battery minerals … someone wanted to talk about that earlier.

It’s not my specialist area, but it seems key to geopolitics at the moment. My totally amateur take is that I’m not convinced owning 20% of glencore really secures all that much. And there is indeed a conflict in the ESG conceptual classification.

@ Bruce – interesting. Had not heard about the battery mineral OPEC.

Here’s the FT story

Indonesia is studying the establishment of an Opec-like cartel for nickel and other key battery metals, highlighting the geopolitical confidence of nations that are rich in resources needed to make electric cars. Bahlil Lahadalia, the country’s investment minister, said Jakarta was looking at mechanisms similar to those used by Opec, the group of 13 oil-producing nations, that could be employed in the supply of metals that are central to the energy transition.

Anjuli Davies 12:58Looks like for banks the pain is yet to come… Barclays beat on FICC trading but then are setting aside funds to cover loan losses

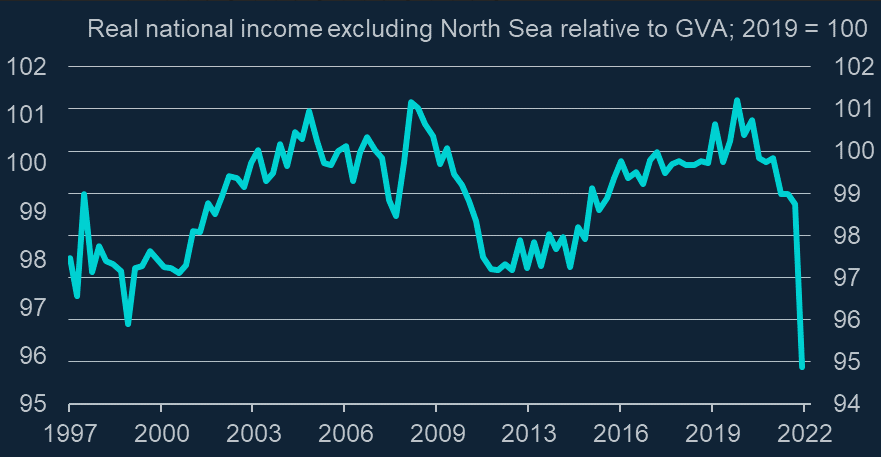

Izabella Kaminska 12:58For me in the UK, it’s all about this chart

That’s the real income in the UK, from a recent BoE paper

If income doesn’t keep up with interest rates we are definitely looking at banks having to reassess their mortgage portfolio risk, IMHO.

Yeah, so I think bank stocks are going to be interesting in the next quarter. But a lot of the pain hasn’t yet been absorbed.

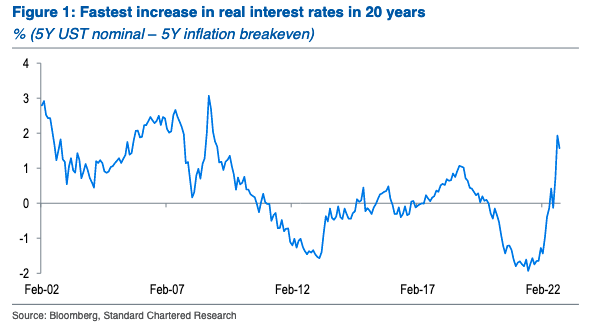

Izabella Kaminska 13:02Right – 12 noon – and I have a Halloween party to organise. But before we finish off.. a couple of interesting charts from Steve Englander at Standard Chartered.

He’s anticipating a slowdown now in the Fed’s rate hiking schedule

Our forecast is that the Fed raises by 75bps in November, 50bps in December and

25bps in January. Money markets are currently pricing 75bps, 60bps, and 36bps over

these three meetings. If Fed Chair Powell raises the possibility of a pause, we could see

market expectations for the December and January meetings ease towards our forecast.

Despite our view that the Fed will characterise any prospective slowing of policy rate

hikes as technical rather than dovish, we still expect money market yields to come off

and asset markets to rally if a slowing of the hiking pace is indicated. Investors would

see the discussion of slower hikes as an indication of where the Fed expects and

wants policy rates to go. The USD would likely follow US yields downward, but

leadership in any weak USD move could alternate between high-yielding EM

currencies and low-yielding G10 currencies that have been heavily sold

There has been a lot of dovish discussion of pivots and pauses, but June 2023 fed

funds futures are less than 10bps off their cycle highs and end-2023 fed funds

futures are only about 25bps off their highs. Market commentary has been more

dovish on pivoting so far than market pricing.

Powell will probably argue that fed funds at 4.5-5.0% represents a significant degree

of tightening that plausibly could restrain inflation. The increase in real interest rates

has been the fastest in the last 20 years and rates are now higher than any level

since 2008 (Figure 1). If we make reasonable assumptions on the path of inflation

expectations before inflation breakevens became available, the increase in real

yields over the last six months is probably the fastest since the early 1980s.

But also worth noting – that Treasury market liquidity is now definitely on the radar

This bit I found particularly interesting

Fed Chair Powell will likely be questioned on quantitative tightening (QT). The FOMC

probably still hopes that QT can proceed behind the scenes without being seen as a

major contributor to policy tightening. Powell will probably argue that the QT impact

thus far is modest, while admitting that the impact is difficult to quantify.

Asset-market, and especially Treasury market, liquidity is a plumbing issue that the

FOMC would prefer to disengage from monetary policy. If asked, Powell is likely to

indicate that the Federal Reserve Board is monitoring liquidity conditions, but we

doubt he will provide concrete proposals or a timetable for any regulatory changes.

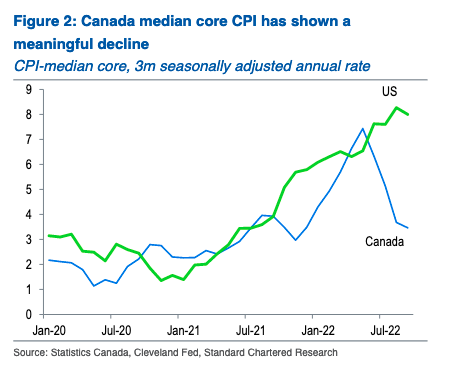

Last and not least, I found this divergence between Canada and the US quite interesting:

The shape of things to come maybe?

On that note, it’s halloween party prep time for me!

Have a lovely spooktastic evening.

Ciao for now.

Anjuli Davies 13:06ciao!

Happy Halloweening – have a spooky time

Remember if you want to take part in the live sessions you need to be a Blind Spot or Betaville subscriber. If you already are, please fill out the application form here and we will get you a login. The sessions are run on the Coodash platform.