Izabella Kaminska11:00

Izabella Kaminska11:00Good morning everyone.

Morning!

Izabella Kaminska11:00And welcome to Spot Markets Live – or as we like to call it – ‘Dispatches from the fall of Rome”. Or is it the Fire of London? Not sure.

I can take the Tacitus role.

I’m joined by my companion in arms, Samuel Pepys. Sorry, that’s Frances Coppola. Morning Frances, what do you see when you look out your window today?

Deutsche Bank. It’s always Deutsche.

Except when it’s Credit Suisse.

Or Boris Johnson.

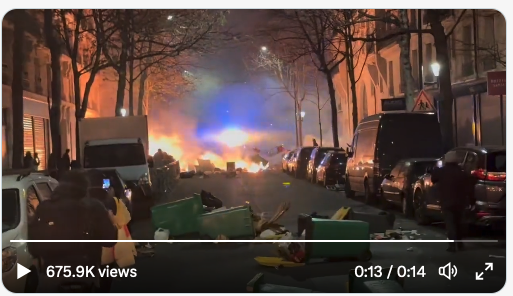

Izabella Kaminska11:02I’m actually just back from the Politico Finance Summit which happened in Paris yesterday. Landed in the evening, and as soon as I put my phone on I was bombarded with images of Paris in flames.

11:03VICTOR HUGO eat your heart out:

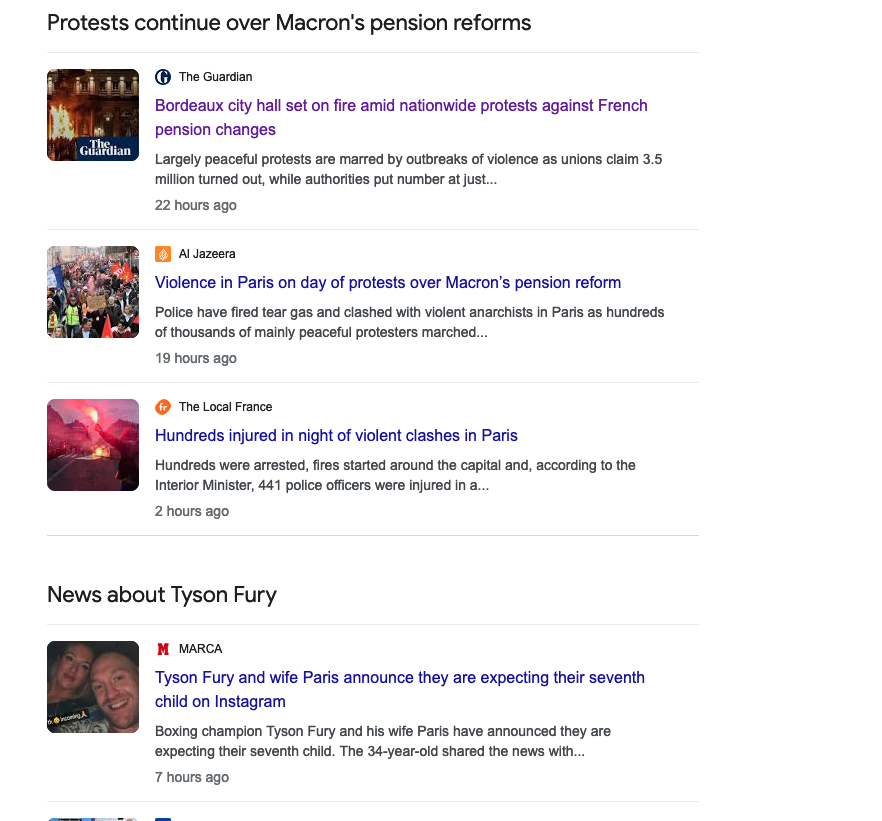

Except here’s the funny thing. If you google Paris in the news section on google you get:

One story about Bordeaux, one al jazeera story and one local news story (which somehow slips through) and then straight on to stories about Tyson Fury’s wife.

Go figure.

So what is going on? Is Paris melting – as per social media. Or is there nothing to see here?

Well, you’re the one who was just there… tell us!

Izabella Kaminska11:05That’s the funny thing, I was. And I have to admit I didn’t notice anything. And our conference was right next to the Arc de Triomphe. That’s not to say there weren’t other indicators of stress.

The rubbish situation is out of control, none of the taxis accept credit cards, and when I stopped at an ATM I was hustled for a 10 euro note by a woman who claimed her wallet had just been stolen on the metro.

Sounds perfectly normal for Paris.

Izabella Kaminska11:05So I’m going to go all Baudrillard on this and reference his famous “the Gulf ward did not take place” idea.

Though to be perfectly honest, I think both Macron and the protestors have a point. Macron is right that the pension liability is not sustainable

But the protestors are right that given they pay so much bleeding tax they should get something for it.

Oh and Charles’ trip has now been postponed:

King Charles’ state visit to France postponed – French presidency

BUT ENOUGH ABOUT PARIS! What about the markets?

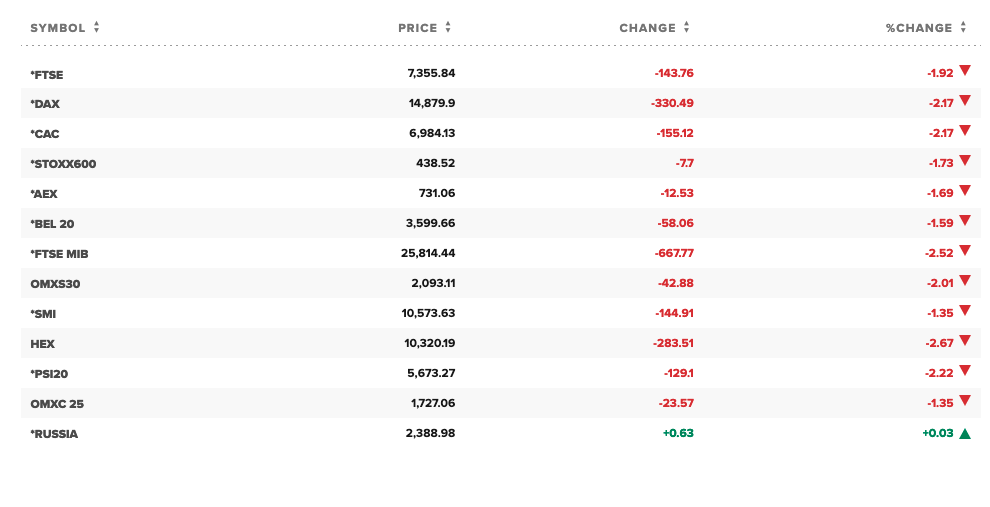

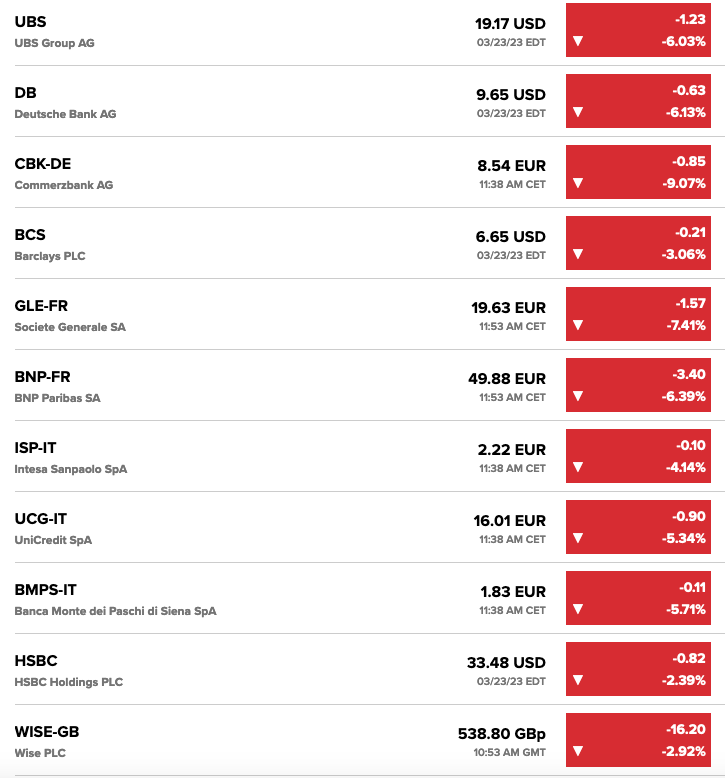

Deutsche Bank share and AT1 prices down as contagion spreads following Credit Suisse/UBS merger.

Izabella Kaminska11:07????????????????????????

Yes and all red today.

European Bank stocks leading the losses as the world belatedly realises the mess with the AT1 debt is bigger than anyone realised.

????

UBS WAS DOWN AS MUCH AS 8% apparently

Also this does not help:

Credit Suisse Group AG and UBS Group AG are among banks under scrutiny in a US Justice Department probe into whether financial professionals helped Russian oligarchs evade sanctions, according to people familiar with the matter.

The Swiss banks were included in a recent wave of subpoenas sent out by the US government, the people said. The information requests were sent before the crisis that engulfed Credit Suisse and resulted in UBS’s proposed takeover of its rival.

Subpoenas also went to employees of some major US banks, two people with knowledge of the inquiries, said.

The Justice Department inquiries are focused on identifying which bank employees dealt with sanctioned clients and how those clients were vetted over the past several years, according to one of the people. Those bankers and advisers may then be subject to further investigation to determine if they broke any laws.

It’s like America wants to shoot down Switzerland.

The timing of this announcement is distinctly suspicious, don’t you think – since the DOJ apparently sent the subpoenas before the Credit Suisse/UBS merger?

Izabella Kaminska11:08Absolutely

Also other banks are involved. Markets are so good at putting two and two together that this might help explain the contagion. DB’s US arm has fallen foul of the DoJ before.

Ben Harrington11:09

Ben Harrington11:09Oi oi

Morning Ben!

Ben Harrington11:09I know I’m not officially on today

Izabella Kaminska11:09Fly by from Ben harrington

Ben Harrington11:09wondering how I get onto the side with the rabble?

Izabella Kaminska11:09Little comment box right at the bottom Ben

Ben Harrington11:09Oh yes oops sorry to disturb

Izabella Kaminska11:10No worries. Let’s continue. All thrills here at SML

Ben’s like a British pilot dropping in unexpectedly in Allo Allo

Anyway where were we?

It’s all about the underwater bonds, and the valuations of the AT1 debt.

@graham made an interesting point about banks and interest. The chair of the European Banking Association was at our conf yesterday and actually made the point that higher interest rates aren’t necessarily good for banks.

Inverted yield curves are terrible for banks

and we have lots of those right now

Izabella Kaminska11:12

That’s from the Politico Pro subscriber story

@Ben if you mean sterling depositors, where would they move their money to?

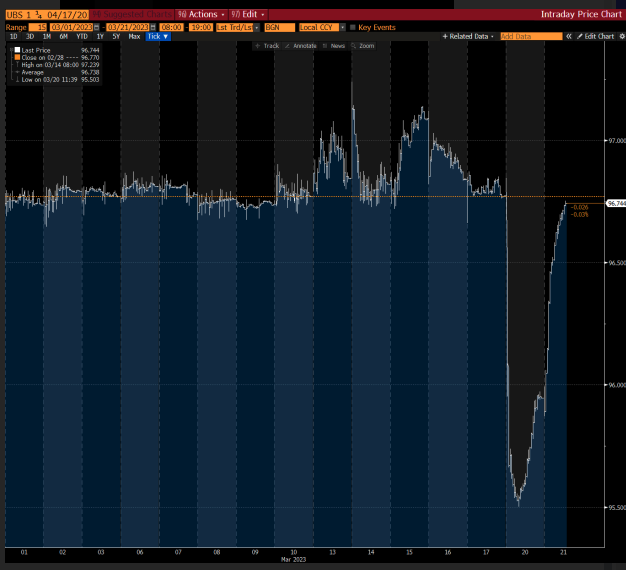

Izabella Kaminska11:13But before we go talking about under water bonds, I do think the rollercoaster ride in senior UBS debt is worth a look at

That’s a chart from March 21

Let’s go surfing

Izabella Kaminska11:13Don’t have a more recent one I’m afraid

but it’s worth comparing with CS

UBS, has governed by a similar ring fence holdco/opco situation as CS and now has de facto absorbed the loanbook that accountants said was absolutely fine, but it itself said it wasn’t by giving it a valuation of 3bn Sfr

you can’t have it both ways.

Anyway, you will see how the announcement on the 15th did establish a floor and prompt a bit of a squeeze.

But not enough. Btw, I genuinely did think that the offer to buy the debt could trigger a virtuous loop/squeeze that could lift the equity.

And it could have worked too if not for the broader issue about the uncertainty over the AT1 debt, which had an opposing force. That was MY BLIND SPOT.

I was always sceptical that it would work

I thought it would take too long and be insufficient

Izabella Kaminska11:15I think in hindsight they knew it wouldn’t. It was just to buy time until the weekend.

Anyway I think the Swiss situation is now summed up by this meme:

Izabella Kaminska11:16

Izabella Kaminska11:16ha ha!

It’s what i always suspected

Yep

Izabella Kaminska11:17The bankers are EXILING themselves to the middle east

because nobody can make the swiss model work in Euroep

Dubai, here we come

Along with all the crypto bros on the run from the law

Izabella Kaminska11:17This as UK minister Andrew Griffith indicated yesterday at our conf that the UK was finally ready to reach out to Europe on financial services regulation

Hinting the singapore on thames model is dead

It was never alive

I’m not convinced that the UK and US dragons are that fierce. Lawmakers in all three jurisdictions rolled over to have their tummies rubbed.

US Treasury guaranteed deposits for SVB and SBNY depositors

which upended the bank resolution regime

Izabella Kaminska11:19If the West doesn’t have the rule of law though, it has nothing

That’s the problem

we might as well all be living in Russia

And the UK relaxed ring-fencing rules to enable HSBC UK, the ring fenced bank, to take over SVB UK

Kathleen Tyson said on Wednesday that she was very worried by this outbreak of lawlessness

11:21What is the point of establishing things like bank resolution regimes and ring fencing if the moment a few banks get into trouble we throw them away?

@Robert I suspected it was not really an independent entity. We couldn’t find an entry in the Gazette confirming its PRA licence as an independently capitalised subsidiary.

Izabella Kaminska11:23This is exactly the point Frances, and I won’t say who told me this, but you can read about the context here

11:23

@Bruce the Swiss have not explained even why Credit Suisse needed resolving

Izabella Kaminska11:24As one former top British central banker told POLITICO, “They could have used bail-in; it would have worked; and banking would become part of a capitalist market economy” — a reference to the loss-absorbing processes regulators came up with after 2008 to ensure bank failures didn’t have to draw on public resources ever again. “The only stable equilibrium is one where bank resolution works, or socialism,” he added.

And on the US side, the asset recovery from SVB was expected to be good, so the US Treasury could have provided loan guarantees to ensure uninsured depositors had access to liquidity. There was no need to throw away the rule book in response to VC lobbying.

Izabella Kaminska11:25another central banker told me yesterday the problem is if they used bailin, it would have meant depositor haircuts like in Cyprus.

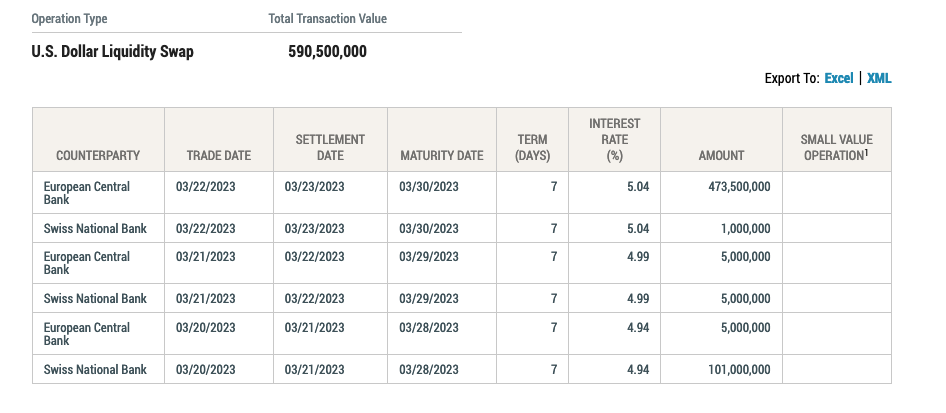

Anyway here’s what the pick up of USD has been like:

But that is the whole point, Izzy!

Izabella Kaminska11:26

This doesn’t look like a massive dollar liquidity squeeze to me

Izabella Kaminska11:27It doesn’t. And I wonder if that makes this very different to GFC.

The US situation is a mashup of Savings and Loans with the German Landesbanken

Izabella Kaminska11:28in 2008 the rout was caused by devaluation on dollar denominated debt, which needed dollar collateral for the margin calls.

This time it seems to be own debt leading the charge

So maybe it’s not a swaps story…

The problem is that does kind of mean every central bank is on its own.

It also suggests that one of the things that ties the system together to the dollar is diminishing in its effect.

But perhaps the dollar squeeze is yet to come?

This is all about maturity transformation, @Bruce. Lots of banks taking MTM losses on longer-dated government bonds, not all of which have been hedged.

Izabella Kaminska11:30And the dumb thing is, it was the most obviously flagged thing ever.

Anyway should we quickly divert to fintech and then come back to banks?

SQUARE/BLOCK NEWS!!

There was a shortseller attack on Jack Dorsey’s *other* company square/block on Thursday from Hindenburg Research. As they note about The Block:

Izabella Kaminska11:32Not this block to be clear

Which is equally mad

Basically, Hindenburg Research has accused The Block of fraud.

Which didn’t go down well, especially since the revelation last December that The Block was partly funded with loans from Sam Bankman-Fried

Izabella Kaminska11:33ha ha!

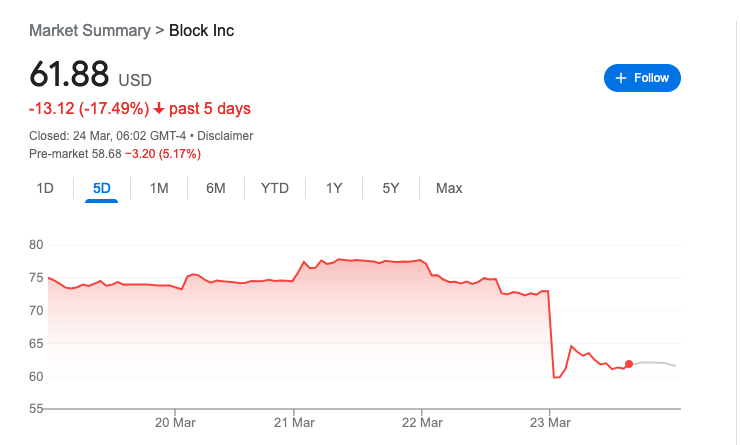

The Block’s share price is down 10.27% today.

(well yesterday, at close – you know what I mean)

Though on a longer time frame doesn’t look quite so bad:

That reminds me of the shape of the cobra and the hat comparison from Le Petit Prince

Bankman-Fried, as I’m sure you all know, is the former CEO of FTX who is currently awaiting trial for fraud.

The Block’s CEO, Michael McCaffrey, stood down after SBF’s involvement was revealed.

Izabella Kaminska11:34

Le Petit Prince Formation

Hindenburg are basically wondering if Block is the next Wirecard, but frankly, my assessment is – and I kind of felt this all the way through the Wirecard debacle – that the issue isn’t really with specific firms.

The entire fintech payments company model is subject to these poor incentives and these issues apply very broadly.

And frankly the same exact “Petit Prince” pattern applies to PayPal:

And other tech companies too. I think we’re seeing the QE-driven tech bubble of the pandemic years bursting. The crypto failures of 2022, and the tech-related bank failures of 2023, all speak to this. And the layoffs at big tech firms.

Izabella Kaminska11:36The only thing I learned from Hindenburg’s report that I didn’t already know is that they were gauging on FX fees.

And that the way they do that is by basically operating through a small bank to which the rules about not gauging people do not apply. I always wondered why PayPal banks with a small bank too.

The fraud and compliance multiples were also interesting, but not surprising. I.e. that given its size it has so many more cases of fraud than the equivalent at a big established bank.

small banks are more lightly supervised than big banks, especially if they are “challengers” or fintech – they are less likely to have stringent controls and may lack the expertise to recognise fraud. And there’s an obvious financial incentive for a small bank to be actively complicit in fraudulent transactions for its big customers if the regulators aren’t looking.

Izabella Kaminska11:37Which is why it’s very suspicious if a behemoth like PayPal continues to bank with a small bank!

Anyway, the key point this is revealing is that FLOAT MANAGEMENT IS NOT EASY.

And during ZIRP/NIRP the usual interest arbitrage that made these sorts of payment companies successful (because they basically skim interest from the floats they manage), became much harder, forcing them to take more risk on the duration side.

But payment companies aren’t supposed to take such risks.

. They are supposed to be full-reserve systems.

So if they’re not going to get interest, and they can’t charge fees (because TECH is underpinned by the fremium model) they’re going to make money some other way – notably by taking risk or by banking people nobody else will bank for a reason.

full-reserve banking never lasts for long. It’s fundamentally unprofitable and fractional-reserve banks will always eat full-reserve banks’ lunch.

Izabella Kaminska11:37Is Square/Block really going to be that much worse than any other fintech?

Exactly, Frances. Btw the only person who ever understood this was a guy called William Quigley who I interviewed at Web Summit this year. Turns out, he was one of the earliest investors in Tether. He calls himself a “co-founder”

I actually really liked him when I met him, and the reason I liked him is precisely because he understood the Paypal business model better than anyone and he like me, became fascinated with how it works.

That’s interesting. Tether originally claimed to be full-reserve – said it had $1 for every 1 USDT, in actual cash dollars. This turned out not to be true. We don’t know exactly when Tether became fractionally reserved, but it certainly was by 2018 when the New York Attorney General sued it for lying to its customers.

Izabella Kaminska11:38But it was exactly the same with Paypal! It’s been in and out of managing its own float in securities for ages

This is true of all payment systems. Ironically, when interest rates go up, the temptation to play around with duration and asset risk goes down.

It’s like the state is then paying them off to be honest/less risky. I am reminded of the deal Cicero cut with the pirates.

The history of “narrow banking” and full reserve banking is a pretty bad one. What typically happens is that banks that claim to be fully reserved find ways of leveraging deposits without telling anyone, then get caught out on interest rate risk or bad loans. As has happened with Silvergate and SVB, both of which were acting as “narrow banks” for their tech depositors – hence the predominance of govt bonds on their balance sheets. They juiced their (otherwise nonexistent) net interest margin by taking duration risk, and avoided having to hedge that risk by classing the securities as “held to maturity” even though they were backing runnable deposits.

The Fed is really suspicious of narrow and full-reserve banks. It recently refused Custodia Bank membership and a master account even though the bank said it was going to back all its deposits with reserves and T-Bills, do no lending, and make all its money from transaction fees. The Fed said it didn’t think Custodia Bank’s focus on crypto-related activities, and its plan to issue its own stablecoin, was consistent with “safe and sound” banking.

Izabella Kaminska11:40And Caitlin Long who was behind Custodia, was very pissed off about it.

She’s also very pissed off about the seizure of SBNY

Izabella Kaminska11:40

I had had a bet with my colleague Bjarke that they wouldn’t show after the debacle, but they did.

And that’s lucky as they were sponsoring the conference. Have corrected the image:

Circle’s USDC unpegged after SVB’s failure. The crypto world discovered that “fully-reserved” stablecoins that have cash reserves in fractionally reserved banks aren’t fully reserved.

the weirdness now is that USDT is apparently safer than USDC because it didn’t unpeg.

Izabella Kaminska11:44What about Coinbase Frances, our favourite unofficial broker-dealer without a broker-dealer license?

Ah yes, Coinbase and its woes… SEC hit Coinbase with another Wells notice yesterday. Back in 2021 the SEC issued a Wells notice to force Coindesk to pull the launch of its Lend program, which was basically a form of risky shadow lending targeted at retail depositors who were promised very high returns. The same business model as the (now failed) lenders Celsius, Voyager and Blockfi, and also Nexo, which the SEC forced out of the US last December by means of coordinated legal action with various states.

So now it seems the SEC has the rest of Coinbase’s products in its sights, particularly its Earn program and its DeFi staking product, both of which are really just variations on shadow lending. Coinbase has asked the SEC to tell it exactly which of its products it thinks are unregistered

securities, but the SEC’s position appears to be that all of them are securities unless Coinbase can think of a very good reason why they should not be. The SEC took the same line when it closed down Paxos’s Binance USD stablecoin in February.

Izabella Kaminska11:45@Robert – not sure.

I was always shocked that the Earn programme wasn’t obviously marketed as a money market fund.

That’s because just like the Block, the whole business model of crypto is about avoiding regulation. MMMFs are regulated.

Izabella Kaminska11:46It’s the same story over and over.

Maybe the lesson here is that finance is actually impossible to regulate?

it’s like whack-a-mole

Izabella Kaminska11:46Because it’s like a continuously evolving system which preys on the fact that most people are financially illiterate

and there is a sucker born every minute

Perhaps a better tactic is just teaching people finance at school?

@willosaurus – that was SOOO good. And also, I wish we could revive it one day.

Has it run out of dollars again?

Izabella Kaminska11:49well quite.

Crypto firms don’t have swap lines to the Fed

So before we close, I thought while we have Frances here we should delve deeper into Deutsche

because not everyone understands the uniqueness of the German quasi socialised financial system

While I get a chart, why don’t you give the context Frances?

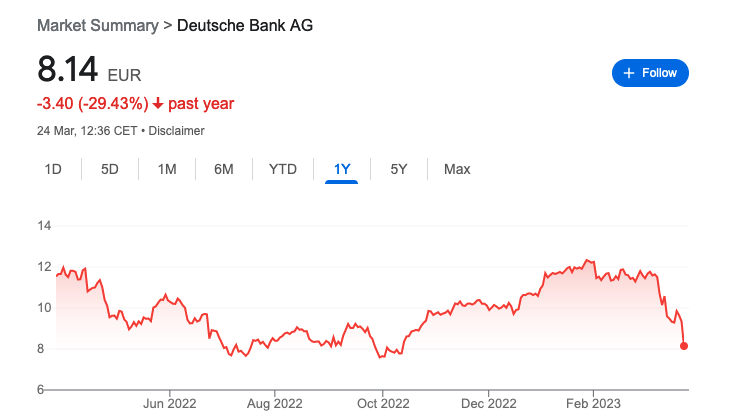

Deutsche Bank… where do I start?

Izabella Kaminska11:52

Deutsche Bank is Germany’s massive flag carrier, but German banking generally doesn’t rely on large banks like DB

Izabella Kaminska11:52

The Sparkassen, Landesbanken, and the two cooperative bank networks Raffeisenbanken and Volksbanken are the core of Germany’s banking system. Each of these as a network is too big to fail, but the individual banks within the networks can and do fail.

11:55So Germany is actually massively overbanked. It is also massively wedded to savings (hence Sparkassen), and historically has exported its excess savings to the rest of the EU. Lots of lovely property deals….

11:56(this is a considerable driver of its trade surplus btw, though that has evaporated rather fast due to the terms of trade shock

So Germany’s bigger banks – DB, but also Commerzbank and the Landesbanken, dipped their fingers into all sorts of dodgy deals and got badly burned.

DB has spent much of the last decade repairing its balance sheet and desperately trying to change its culture

But dirt sticks, so whenever there’s a story about dodgy banks, people assume DB is involved. Hence contagion to DB from Credit Suisse.

Izabella Kaminska11:56As @bruce rightly notes this connects to the Adler story

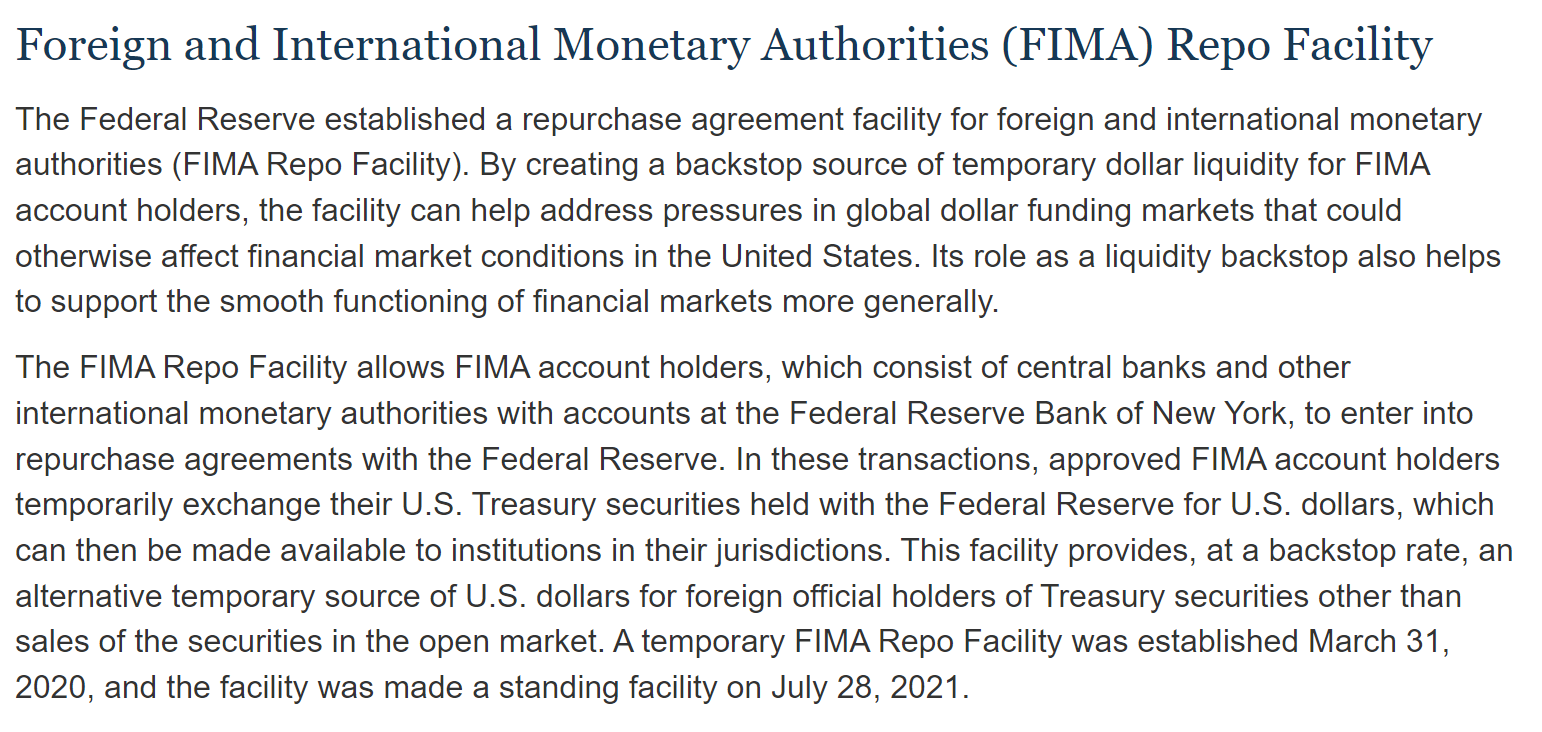

We are officially out of time, but I feel we should get to the bottom of this FIMA news.

FIMA

Izabella Kaminska12:01so let’s go for another 10 min

12:02So this sounds like a special repo for who? Other central banks? How is this different to the swap lines?

Swap lines are unsecured? And this is secured? Is that the difference?

So while everyone was looking at swap line data which was a bit meh, this is where we should have been looking instead?

This enables UST holders to obtain dollar liquidity Izzy

Izabella Kaminska12:03Oh wow. I didn’t even know this facility existed

So these might be foreign central banks that don’t have swap lines

Izabella Kaminska12:04I see, so this is the real marker of stress. But could also be western cbanks that have a lot of treasuries?

So basically, the Fed’s par facility is being extended through this? Or do they charge market rate?

Well this is fascinating.

So what do we think is going on broad picture? We have, as I mentioned below, according to Martin Armstrong a large flight of capital out of the western banking system at the moment too.

but Martin is a – how should I put it delicately – an insightful and often right analyst, with a “checkered past” and a tendency for off-narrative arguments.

Yes, so we may be seeing the emergence of an aligned and unaligned economic zone?

as Kathleen said on Wednesday

Izabella Kaminska12:08All I will say is that the net zero narrative, which I always thought made no sense with respect to actually fighting climate change (as it’s largely self-defeating) is a useful cover for nations that are about to get very poor very quickly.

no that’s great kathleen, we appreciate your insights, and I am now going to go research all about FIMA.

On that note I do have to go though, so thank you all so much, and we shall see what we can do next week.

Parting shot from me: Binance says suspension of spot trading is a “standard operating procedure”. Every time….

Izabella Kaminska12:09Lol

Alright take everyone, Anjuli is back on Monday.

And so am I.

Izabella Kaminska12:09Yay!

See you all then! Have a great weekend without too much drama.

Izabella Kaminska12:10Take care