Good morning, aloha and greetings fellow market wizards.

I just realised I was typing in the wrong window.

I was frankly overcome with self-loathing yesterday when I realised that co-host Dario, has a Generation Z neuralink to the keyboard that allows him to type faster (and flawlessly) than I am able to even cut and paste stuff.

I could hear his keys clacking like a whole typing pool on speed while at this end the hunt-and-punch approach yields a keystroke every few seconds, almost half of which are unintentional. The zoomer left the boomer behind.

Today I was worried there was no co-host and I would be obliged to revert to my default position of talking to myself, an interlocutor with whom I always disagree and it’s a round-the-clock conversation, trust me.

Thankfully, the threatened monologue has been recalibrated as a dialogue.

And I’m joined by Neil Collins, veteran market watcher, prolific columnist, host of ‘A long time in finance podcast’ and quondam City editor at the Telegraph.

And I’m reliably informed, a fountain of dazzling apercus and caustic one-liners…

Good morning, Neil

It’s good to be back. It seems a long time since the start of Markets Live at the FT

That’s because it is.

I am hoping Neil types more slowly than Dario which will afford me time to think.

As we proceed into the 4th quarter, I was deliberating last night as to how I might allocate my overdraft and adjust its various weightings (wine bill, gambling debts, electricity i cant afford to turn on etc etc)

Is this a process you undertake, Neil, allocating your overdraft?

Do you do cash stuffing?

I dont know what it is but i’m very short of the stuff so i doubt it.

Neil Collins 10:37You put your cash into individual envelopes, so you can budget properly

and then someone comes along and steal the lot.

aha, presupposes you have some.

Admiral have said today that it’s not a good idea

They are fed up with paying out insurance claims

Up to £1,700, they say.

It seems like asking for trouble, not to mention fraudulent claims, to me

So if I were Admiral, I’d say “get stuffed” to anyone claiming

they were my car insurers last year when it was stolen

they were very understanding about the fact i left the keys in the car

My car is not worth stealing.

well, instead of cash stuffing i decided to read the advice proffered by Blackrock about how to approach 4Q23 and 1Q24

They highlighted five mega themes, all off which might be quite difficult for the individual investor to incorporate. AI, global rewiring (shifts in production/ trade routes etc), transition to low-carbon, shifting demographics, evolving financial system.

If you’re not cash stuffing, Neil, maybe this is how you go about it.

Blackrock is very much in the higher for longer camp

As CBs hold rates tight owing to stubborn inflation and think outright recession still likely.

They favour short-end UST, hard currency EM bonds (yielding >8%), DM AI plays, Eurozone bonds and among equity markets and they recommend an OW Japan.

Japan is interesting at this juncture

While I wasn’t looking, Japan became a dividend market.

Neil Collins10:45

Neil Collins10:45like the UK

as i was about to ask you

The sustainable yields on many/most companies are very attractive

Difference with japan is that unlike the UK it’s one of the few economies in the world where earnings are being revised higher

On UK dividends, look at BAT. If they stopped paying dividends, they could buy in their entire share capital at today’s price in eight years, after which I would be the only remaining shareholder, and would own the business.

@johnkingston, ww3 is in the megamega category

the cash is in a sock in the [REDACTED].

I hide all my money on the bookshelves in between pages of Joyce or philip larkin.

Safe in the knowledge burglars tend not to read much

Are we going to talk about inflation?

it’s always on my lips

Neil Collins10:51In the UK it’s proving still more persistent, and will collide with the triple pensions lock before long. The unexpected rise is down to petrol prices, where the market is much less comptetitive than it was, thanks to the Issa brothers, owners of Asda.

The triple lock will push up the old age pension by either 8.5 per cent or 7.9 per cent, depending on how the government treats one-off payments in wage settlements.

I make that either unaffordable or completely unaffordable.

The Isa brokers now control 700 petrol stataions. The retail margin has gone from 4.6p in 2019 to 10.8p in 2022.

Please dont call that price gouging

i was about to

but i won’t now

It’s all that debt they’ve got to service

Do you think the BOE will have the independence of thought to raise rates again if it’s appropriate or will they be browbeaten by Rishi who has one eye, in fact both eyes, on the electoral cycle?

Neil Collins10:57Bank Rate is always going to be political.

I think that Bailey has no choice but to keep up the pressure.

If he eased off, and inflation started to rise significantly, he would have to go

Having said that, I would guess that there will be no change in Bank Rate next time. The squeeze is still tightening.

Izabella Kaminska 10:58

Izabella Kaminska 10:58FLYBY – Did someone say petrol prices? I have a bit of stealth breaking news. Unite/GMB voted last night to strike at Grangemouth after refusing a deal for a 11.5% pay rise over two years.

But they’re back at the negotiating table this morning. If no deal is struck, then it could be petrol pump panic again.

Neil Collins 10:59so we may not even be able to buy dearer petrol at all

Izabella Kaminska 10:59This also comes in the context of Keir Starmer threatening to stamp out North Sea ops

With no investment, nobody wants to pay anyone anything.

Julian Rimmer 10:59if we can’t buy expensive petrol that might help inflation come down

Izabella Kaminska11:00

Anyway, that’s all from me folks. Just wanted to give you the heads up so as to get you ahead of the curve at the petrol station.

We would spend our money on something else, or WFH like half the civil service

This is all a bit parochial, especially on a day like today

How about global rewiring and plumbing for something less parochial?

Following on from the Blackrock mega-theme.

someone forwarded me a DB note yesterday about this very subject

and for once the term ‘fascinating’ is meant literally rather than glibly

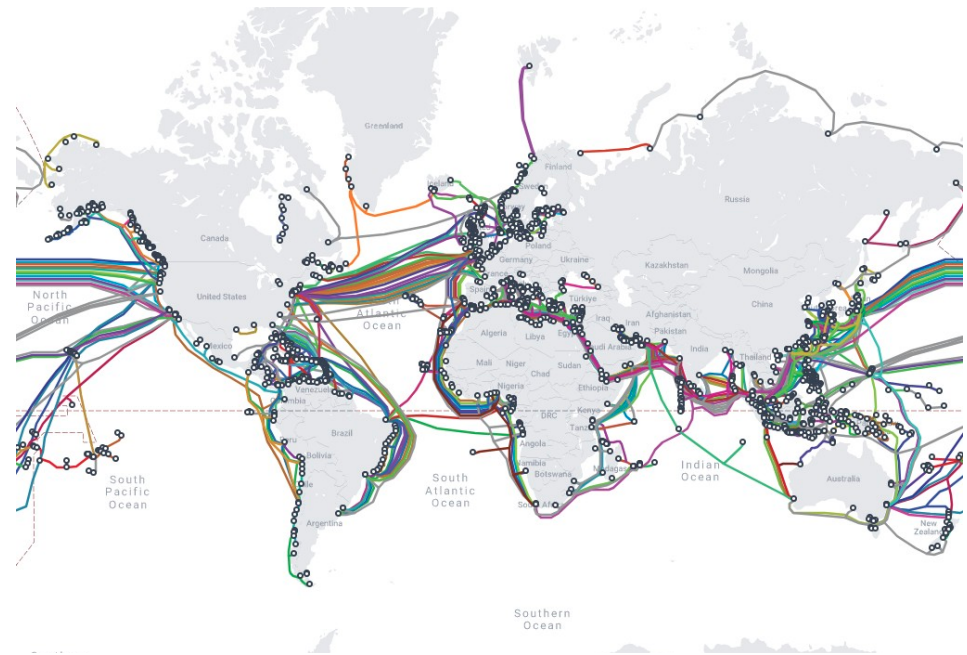

it was / is alarming, original and entertaining in equal measure, demonstrating ‘The five weak links in the globalised economy’. The authors manifest how ‘The global economy is built on a fragile web of vulnerable and largely forgotten pinch points. A scattering of cables, pipelines, land routes, sea straits, air routes and satellites have an importance to the global supply chain and modern life well beyond their negligible footprint’.

i will find the relevant chart in a minute to illustrate this point they make

Very useful information for Mr Putin

Mr Putin: the petrol-pump attendant for China

(currently in Beijing getting his e-360 year-end evaluation from the boss)

The cable chart is a cracker

DB lists the vulnerabilities of economies and infrastructure. For example, 99% of international digital communications – and $10trn of financial transactions a day — pass through fibre optic cables draped on the sea bed. Many are barely thicker than a garden hose.”

That’s actual cables, not £/$

I don’t know about your garden hose but mine has many holes in it

and this revelation, therefore, doesn’t fill me with confidence that this online forum will even go the distance now I realise how filipendulous it is

Izabella Kaminska11:06I happen to have it to hand

i was struck by the fact that Tonga is a very important hub

Who knew?

and that the undersea cables actually go above ground after passing through the Suez Canal

it’s a bit like the District Line, I suppose

some underground some overground but lesss susceptible to industrial action

Unfortunately susceptible to other types of action

The frailties are mostly often exposed by accidental damage: 100 undersea cables break each year, two thirds due to accidents with fishing vessels and anchors; the rest is environmental damage (eg, currents and quakes).

The important nodes are cables & pipes, roads & rivers, sea straits, sky corridors and satellites.

Izi: I think you know. The expression came from the first trans-Atlantic cable allowing transmission of fx rates across the pond.

Threats to these nodes are legion: sabotage and or cyberwarfare by (who else ?) the Russians and the Chinese (and I suppose there must be some other bad actors but the alacrity with which those two spring to mind speaks volumes); accidents, like the ‘Ever-Given’ tanker which became beached in the middle of the Suez canal blocking global trade for a fortnight,

like my wife trying to execute a three-point turn in Sainsbury’s car park.

Neil Collins 11:10you’ll be in trouble now

I was always am. i am a full-time resident of the doghouse

Natural phenomena affect oil pipelines; climate change causes droughts and dries up rivers rendering waterways non-navigable. Gas pipelines and cables between Estonia and Finland were mysteriously damaged on Oct 13th, last year witnessed the Nordstream pipeline blown up by the GRU/ the CIA/ maddie Jihadis (excuse the tautology), George Soros (delete according to taste)

I suppose the conclusion to be drawn, (I’m having to do the heavy lifting here because the Deutsche analyst did not make one)

Perhaps he was understandably worn out by his highly original research or his computer was hit with a virus by cyberhackers before he could attach it, thereby validating his whole note,

… is that disruptions to economic activity, global trade and normal human life, are more frequent than we suppose, are less surprising than we imagine and perhaps more predictable than we claim. It does not take much to bring the world to a screeching halt.

So can you think of an example?

ooh, off the top of my head, major disruption to life all over the globe?

no, im drawing a blank. nothing recent for sure

(A history lesson from Izi!)

This was, in part, the subject of Niall Ferguson’s depressingly-appellated book, ‘Doom’

I’m not sure Mr Ferguson’s track record as a forecaster is all that great

I stunned my family one year by requesting it for a Christmas present although my daughter complained it didn’t sound very Christmassy fare.

i told her our respective childhoods were diametrically opposed

I don’t suppose a book called Cheer Up would sell as well

So, deglobalisation is the upshot of when all this global plumbing and wiring comes unstuck.When people talk about deglobalisation, especially with respect to the aftermath of the pandemic

(oh yeah)

We’ll all be forced to buy locally, and then wonder why everything has got so much more expensive

Perhaps a more accurate description would be desinicisation (or desinofication – I’m not sure about the correct term) or de-russification factories leave China but don’t go back to the states, they go to Mexico, Indonesian or Vietnam.

It’s not quite so destabilising. People are uncomfortable with China’s communist regime or the sanctioned Russian economy and instead relocate to erm, the communist regime in Vietnam.

people just move to the next place along the block that’s just as cheap

There’s an insightful interview on youtube with Louis Gave https://www.youtube.com/watch?v=RX9Nc8KX27Q in which he discusses this subject

among others

Après moi, le déluge…

Further to the discussion on Monday about the looming Armageddon in VC (about which my banking friend very graciously told me I was ‘Approximately right rather than precisely wrong’)

(i’ll take that any day)

I’m grateful that MS very conveniently articulated what I tried and failed to state succinctly….

“Venture Vision: What If…Everything IPO’d at its Secondary Price?”

The glory days of VC and PE are clearly over. Both activities are reduced to taking in each others’ washing

They can’t find suitable candidates to put capital into, so like the antique dealers on the desert island, they buy and sell to each other and all claim to make a profit

Over the last 3 funding rounds of the largest 50 private tech companies, 71% of investments have underperformed an equivalent allocation in the S&P500 by 25%.

It’s worse than that. In the last three years, IPOs have underperformed the S&P by 40 per cent (Morningstar)

that is a sobering thought

MS: With fewer board seats than early stage investors, most growth investors face negative alpha exits. This chart made us think…: Are we about to have a showdown between early and late stage investors? This is not a new phenomenon. Every investor in a cap table will have different views on best timing, price and method of exit for a business.

Traditionally, companies came to market to raise capital for further expansion

The PE seller has already squeezed the lemon, and wants to get out

So: Collins’s first rule of investment. Do not buy a share until it has been on the public markets for at least a year.

my first rule of investment is: money in must be greater than money out but i’ve never implemented that successfully.

(@Willo: thank you!

The companies analysed by MS in this report have a collective valuation of c$114bn as of the last formal primary equity funding round. Yet, in secondary markets, they are being collectively valued at c$78bn

This is a big whack for a lot of managers and family offices, represents huge wealth destruction and naturally, is making it so much harder for smaller companies to finance growth.

@wilosaurus, yes i agree that the signal station looks pretty idyllic unless, of course, WW3 breaks out and the Russsians send a big missile to your weekend breakaway destination

you’d definitely want a refund on that and leave a terrible review on trip advisorr

A cheerful thought to end: Capital Economics is now forecasting a big fall in inflation next month, to 5 per cent. Let’s hope so.

inshallah. and on a possitive note for once, i shall take my leave so it’s goodbye from me

Neil Collins11:31and it’s goodbye from him.