Izabella Kaminska

Izabella Kaminska10:59Good Morning SMLers!

I see some of you are nice and early 🙂

I’m back. It’s a Friday, my non-Politico day. And well, with what’s been going on, how could I possibly not do a session?

Anjuli will be back on Monday with Betaville’s Ben Harrington. (Though I’ve sent a courier pigeon her way, in case she does want to join us.)

But fear not, it’s not going to be a one-woman talking shop. I’m joined today by Frances Coppola, who really is the go-to guide for all things financial crisis.

Hello Frances!

FRANCES COPPOLA11:01

FRANCES COPPOLA11:01Hi everyone. This is wholly new to me so I will probably drop some clangers. Hopefully not bad ones!

Izabella Kaminska11:01I’m sure you will be fine

It’s been quite a week. Best described with this meme:

Having Frances on is apropos because the way she came onto my radar originally was through her harnessing of the power of Twitter to analyse the original financial crisis.

Do you remember the hashtag #gfc2 I think it was?

FRANCES COPPOLA11:02Indeed I do. Back in about 2011 four of us (including Ian Fraser, author of Shredded – about the downfall of RBS) used to hold late-night discussions about the state of finance using the hashtag #gfc2. Then the Eurozone crisis happened and suddenly it became real.

Izabella Kaminska11:03Before we get to it. Just gonna flag that Frances has kindly agreed to do a session EVERY DAY next week, so Mon- thru-Fri we will be on every day

So where to start. How are the markets doing today?

FRANCES COPPOLA11:03Is it #gfc3?

Izabella Kaminska11:03ha

Major US indices finished in the green. Europe is up today.

BANK STOCKS: Mostly green, Last week’s panic seems to be over for the moment.

Soc gen up 2.4%, BNP Paribas up 0.66%, Deustche up 1.75%, Unicredit up 0.66 %

FRANCES COPPOLA11:04US regionals still wobbly though. More on that later.

Charles Schwab weirdly in the red

Izabella Kaminska11:04Ah yes we should talk about that. That’s the duration risk factor

EURO = 1.06 to the dollar following a wobble yesterday on Christine Lagarde raising rates. Go figure

POUND = holding strong against the dollar at 1.21

BONDS = US short-term yields up, long term down, UK yields down a bit, German short flat/uppish. Longer term down.

FRANCES COPPOLA11:05Seems markets think the ECB’s rate rise was too strong in the current circumstances

Izabella Kaminska11:05Yes that makes sense, but weird for euro to go down on the back of it

There was a hoopla because the vice president got allegedly “misquoted” saying that there were some concerns about European banks

FRANCES COPPOLA11:06ECB is walking a tightrope between fighting inflation and causing a financial meltdown. Currency traders seem to think it has erred on the side of meltdown. Not seeing much evidence of that in other markets though

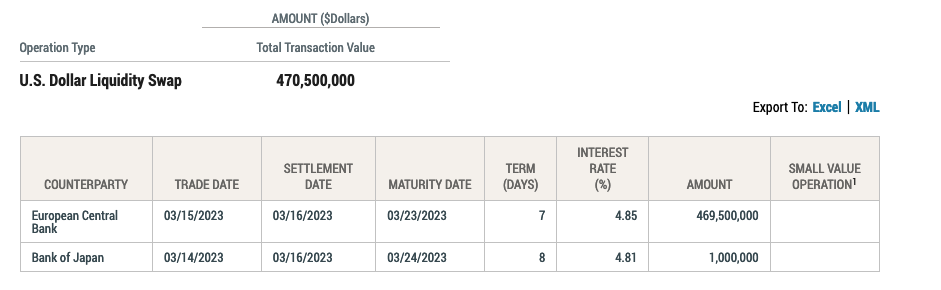

Izabella Kaminska11:07One thing I did note from the Fed Swap Line data yesterday

The ECB taking about $500mn of USD liquidity

FRANCES COPPOLA11:08So there’s a dollar liquidity squeeze in Europe. That would explain the Euro taking a hit on 50bps hike.

Izabella Kaminska11:08(AND YES, Belated Happy St Patrick’s day to you all)

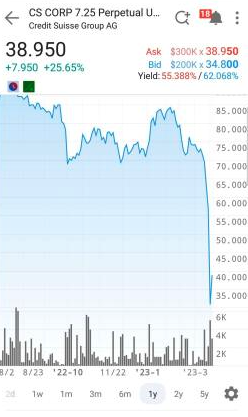

But let’s get to Credit Suisse

The bailout happened but the CDS are still up, and while CS is up relative to Wednesday, it’s not quite the recovery I was expecting

Here’s the stock courtesy of the FT data tool:

FRANCES COPPOLA11:10

FRANCES COPPOLA11:10Seems markets are not convinced that a CHF50bn lifeline from the SNB will be enough to solve its problems.

Izabella Kaminska11:11Frankly, I am surprised.

So why the disparity? Have people forgotten we are talking about SWITZERLAND??

Home of all the gold, all the Toblerone, all the Swiss watches, all the WEALTH….

There is no country in the world more prepared for a financial apocalypse. Until recently every house had a bomb shelter. And even all their tunnels are booby-trapped with explosives.

FRANCES COPPOLA11:12Izzy, Toblerone isn’t going to be made in Switzerland any more

It’s got to remove the Matterhorn from its packaging

Izabella Kaminska11:12Yikes. Well now we know what’s really spooked the market.

SWISS CRISIS ACCELERATES ON MARKET REALISATION TOBLERONE IS NO LONGER SWISS

And this I think kind of speaks of the problem.

Switzerland isn’t what it used to be.

While the economy is still more diversified than most (The Swiss, despite being known for their private banking, actually have a sizeable manufacturing industry and a good chunk of a real economy).

FRANCES COPPOLA11:13Chocolate, cheese and watches?

Izabella Kaminska11:13And drugs. Don’t forget about the entirely legal drugs.

Even so, there’s no doubt even Switzerland’s balance sheet has been knocked by the Pandemic and recent sanctions events.

Also the Swiss banks are no longer the private refuge of secret Russian wealth. Its USP has been swatted.

The SNB has also been battered with financial losses. They would say it doesn’t matter because of how many years they were deeply in the money. But the trend is clear.

Switzerland has a lot of runway (more than most Eurozone countries) but it, like most of Europe. is on cash burn mode.

(Tho Cash Burn is by design what the central banks have been going for.)

FRANCES COPPOLA11:14That’s the whole point of quantitative tightening… suck liquidity out of markets, burn lots of cash

Izabella Kaminska11:15Back to Credit Suisse though. And my assessment is that the markets still haven’t realised that what we have in Credit Suisse is “The Thing” style mutation of a global investment bank into a really boring domestic lender whose most exotic elements are being stripped out.

And in some ways also being turned into a full-reserve banking system.

FRANCES COPPOLA11:15Given CS’s history, that’s probably a good thing

It’s done far too many exotic things

Izabella Kaminska11:15Loans on a covered loan basis just means that the bank cannot do fractional reserving. I see RM is in the room, please correct me if I’m wrong. But the way I see it every penny it distributes in crisis mode is fully funded.

This to me is the prelude to CBDC banking – but let’s get back to that later.

The rescue deal the SNB and FINMA came up with in the early hours of Thursday morning was in my opinion pretty ingenious

Because it created a sort of positive circle boom loop in theory.

FRANCES COPPOLA11:16Izzy I somewhat disagree on the fractional reserve thing, if the collateral is longer duration than deposits then it is fractionally reserved – like SVB

Izabella Kaminska11:17Yes, but apparently it isn’t. Most of the CS stuff is short-term and/or hedged (supposedly)

One of the issues they face is that after the original crisis Credit Suisse was divided in such a way to make sure its dangerous international ops could never pose a threat to the lovely bunkered up Swiss ever again.

That saw it divided into Holdco and Opco.

FRANCES COPPOLA11:17Yes it was ring fenced

Izabella Kaminska11:17Now because of that divide not all creditors are equal.

Would you want to invest in a bank as a foreigner that had basically explicitly told you it has no interest in protecting your claims before those of its own people/citizens first?

Trump had America First. The story of Credit Suisse is: SWITZERLAND FIRST.

FRANCES COPPOLA11:18Protect our famous SWISS BANK. Actually this is probably the solution going forward….

Izabella Kaminska11:18The CDS is reflecting the chances of the holdco having to be bailed in. But that’s a very different story to the whole of Credit Suisse going down.

The Swiss heart of Credit Suisse will live on forever. But the international part might not.

BUT! At the moment the rescue deal involves a fascinating scenario where Credit Suisse is going to buying OpCo senior debt of up to 3bn Swiss Francs.

Using a loan from the bank of mum and dad to basically cancel your kids debt is what’s going on here.

And in the process, the market rate of that debt – when the market realises it’s actually dealing with mum and dad not the kid – then goes up.

But there’s another smart component beyond creating a squeeze in your own debt.

Buying back the debt below par creates an immediate windfall, that despite everything translates to an overall equity injection into group as a whole despite the holdco/opco split.

FRANCES COPPOLA11:20I am reminded of how Terra Luna operated when its “equity” layer was collapsing.

Izabella Kaminska11:20Yep, to all intents and purposes IMHO, CS Switzerland is now basically a stablecoin, drawing on the equity of its core business to keep its HQLA/assets funded at above the 100% coverage ratio. Except the weird thing is the equity is going down despite the bank being well over the 100% mark.

FRANCES COPPOLA11:20As the bond prices fall, buying them back generates more and more equity

Izabella Kaminska11:20Yep

And like a stablecoin it mostly just has to manage duration risk and liquidity risk.

It’s kind of become the core financial system’s equivalent of Tether. “Trust us honest we do have all the liquid assets we claim to have! And more!” but nobody believes them and keeps shorting the equity.

This makes sense because like Tether, it’s hard to trust a bank that has had so many associations with dodgy goings on. Think of Archegos, Tuna bonds, Greensill. Think of the dodgy HNWI clients.

But unlike Tether, it’s got the SNB and FINMA to endorse the fact that what it says is really true.

FRANCES COPPOLA11:21Funny you should say that given KPMG gave SVB the greenlight just two weeks before it went down.

Regulators and auditors don’t always get it right

Izabella Kaminska11:22You would hope the Swiss regulators can be trusted. Though if not that brings up larger issues about Switzerland!

But anyway, the point is that we are dealing with a bank that has more liquidity than it needs in a banking environment in which it’s actually quite hard to have a bank run.

There’s only really UBS as a direct competitor, and having lived in Switzerland I can tell you that signing up for another bank account is not that easy. It’s certainly not as easy as getting a Monzo card.

So liquidity isn’t really the issue.

FRANCES COPPOLA11:22As with TerraLuna, it is solvency that is the issue, not liquidity.

Izabella Kaminska11:22indeed

Imagine Tether being overcollateralised (i.e. having more liquid assets than it needs to meet run risk) and even then its equity being run to the ground by a broad panic due to “duration mismatch”. (Which apparenlty it doesn’t have)

This being the case even as it continues to generate cashflows for itself, and reparking them as its own bail-inable deposits in the group.

THIS IS NOT SVB. And it’s not news to anyone that its prime brokerage IB business has been on the decline for ages.

FRANCES COPPOLA11:23Market seems to be expecting some kind of recapitalisation

JP Morgan floating AGAIN the idea of a sale to UBS

We’ve heard this many times before of course

But we’ve also seen lots of CS recaps and restructurings none of which have solved the problem. So is it time for a breakup and sale?

Credit Suisse is on paper solvent, but one thing we saw with the US’s Silvergate Bank was that it was insolvent despite having a CET1 ratio in excess of 50%, because so much of its balance sheet was zero risk weighted.

Izabella Kaminska11:26 FRANCES COPPOLA11:26

FRANCES COPPOLA11:26Ouch

Izabella Kaminska11:26But the risk of bail in is real. That said, if you’ve got a spare dime why not?

FRANCES COPPOLA11:26That does look like the expectation of a bail-in, doesn’t it?

Izabella Kaminska11:26Peter thiel left $50m of his own money in SVB btw

FRANCES COPPOLA11:27No wonder he wanted the FDIC limit lifted

Izabella Kaminska11:27A good op to switch to US goings on. So Frances, tell us about what’s going on in America?

FRANCES COPPOLA11:27It’s been a bumpy ride…

Earlier this week, First Republic Bank’s credit rating was cut to junk by three ratings agencies because its balance sheet structure was uncomfortably similar to that of Silicon Valley Bank – lots of uninsured deposits backed by government securities on which it was taking unrealised fair value losses. Its share price fell 26% on the news, though it later gained a few percentage points.

Now,11 Wall Street banks have contributed $30bn new deposits to improve its stable funding. FDIC & Co say “we are eternally grateful”

Izabella Kaminska11:28Mates rates right?

FRANCES COPPOLA11:28 Izabella Kaminska11:28

Izabella Kaminska11:28How is this different to just normal interbank funding tho? I guess it’s the rate that matters?

FRANCES COPPOLA11:29Very much so. Lots more liquidity without tapping the Fed at a penalty rate. And stable funding – the Wall St banks are not going to pull their funds.

FRB’s problem, like SVB, is lots of uninsured depositors that all herd together, and unrealised fair value losses on the securities backing those deposits

Izabella Kaminska11:30And presumably, it’s all circular, this is them just returning the deposits that people transferred to them.

FRANCES COPPOLA11:30So if it can improve its stable funding, the run risk diminishes and so does the risk of having to realise fair value losses on a held-to-maturity securities portfolio

Yes it’s all funny money.

FRB is far from the only US regional bank with that kind of crippling duration mismatch and run risk, though.

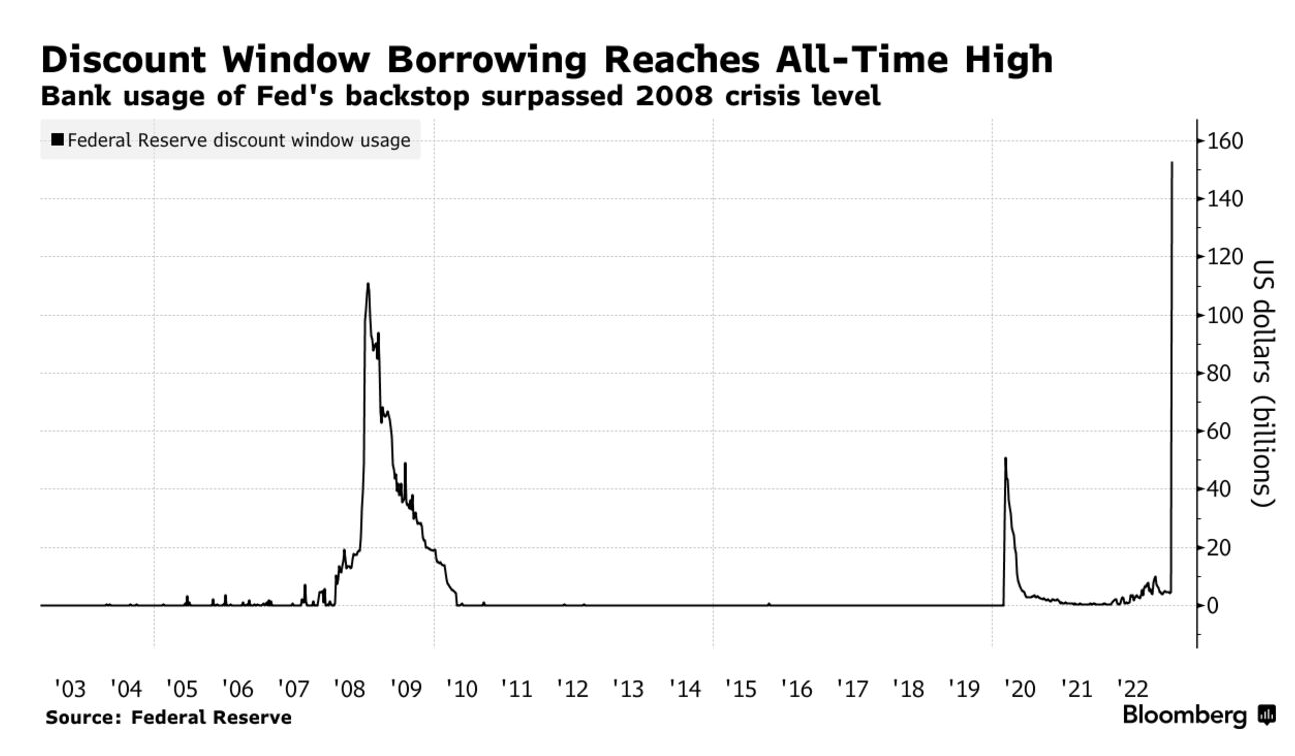

So the banks have been borrowing loads from the Fed

Bloomberg says they have so far borrowed $11.9bn under the new BTFP scheme which allows them to pledge collateral at par instead of market price. And they have also borrowed unprecedented amounts from the discount window.

Izabella Kaminska11:32I saw that repo expert Scott Skyrm (never can spell his name) was complaining that the Fed funds rate is now fake.

FRANCES COPPOLA11:32

That’s because of the collateral uplift on the temporary funding scheme introduced by the Fed

Izabella Kaminska11:33He sent me this note, but I don’t understand what he means. Maybe you have some insight.

It’s just with all the funding pressure yesterday sofr didn’t move from 4.55, where it’s been for weeks. I got a lot@of calls from traders complaining their sofr hedge wasn’t working since they funded higher at GC repo rate and no change in sofr

FRANCES COPPOLA11:33Banks can obtain funding from the Fed by pledging collateral at par instead of market price. That’s going to distort the fed funds rate

yeah exactly that it drives banks to the Fed instead of the repo market and thus distorts sofr

Izabella Kaminska11:34This is because it basically is tiering rates right? It’s like saying the longer term rate is really the short term rate?

as if rates have never changed

Back to future rates for some banks?

FRANCES COPPOLA11:34I thought when the Fed introduced that scheme that if it was heavily used the Fed would find it hard to keep control of the FFR

Yes ineffect it is cheap lending for banks

Izabella Kaminska11:35So now we have one rate for high street people like us, and another for distressed banks?

Is that fair? Is this what post crisis legislation was supposed to deliver?

FRANCES COPPOLA11:35Well no, and I think the Fed & FDIC interventions have driven a truck through Dodd Frank

11:37Banks seem to be making a concerted effort to improve their liquidity in case of a SVB-style run on uninsured deposits. But they are using the Fed not the repo markets to do it. So that distorts SOFR and hence the FFR. Also, on Twitter, Bill Ackman complained that the Wall Street bailout of FRB was spreading risk to the biggest banks. He called for the FDIC limit to be lifted. This would effectively make all deposits liabilities of the state and end the Dodd-Frank bank resolution regime under which uninsured depositors can take losses.

Izabella Kaminska11:37For those who don’t know, what’s SOFR?

FRANCES COPPOLA11:37Secured Overnight Financing Rate

Izabella Kaminska11:37I see the alternative to Libor which is unsecured

So bill ackman is basically recommending the dawn of state banking

FRANCES COPPOLA11:38Yes.

Izabella Kaminska11:38we are all USSR now 🙂

FRANCES COPPOLA11:38He’s not the only one saying all deposits should be insured

Izabella Kaminska11:39This is so bad for moral hazard, and it makes a mockery of dodd frank, because even if the bailouts aren’t coming from the Treasury side, its still a de facto state guarantee and that means the end of laissez faire banking

I can already see all sorts of conditionality being applied, like loans only for ESG friendly purposes and such.

FRANCES COPPOLA11:40Certainly much greater control over the purpose and ownership of deposits. We’ve been moving in that direction for a while though

after all what is KYC/AML if not control of deposit ownership and purpose

Izabella Kaminska11:41I don’t think it’s a coincidence that the cbanks are all suddenly pushing ahead with CBDC. They can keep the system afloat with these sorts of guarantees for a few years but eventually it will become transparently obvious that we are dealing with just one bank. And then you might as well have a CBDC.

FRANCES COPPOLA11:41It seems awfully timely that the Fed has just announced a July launch for FedNow https://www.federalreserve.gov/newsevents/pressreleases/other20230315a.htm

Not yet a CBDC but moving in that direction

Izabella Kaminska11:42Slowly all paths leading in that direction.

11:43And the Chinese as well. And Russia too. I suspect the whole way we deal with money might change. It won’t be a fungible asset anymore, your personal credit, profile and importance to the system (and or cause) will be what determines the rates you get and how much access you get as a result.

I mean, it’s funny because none of this has resulted from any master plan conspiracy, it’s just the way things are organically going.

FRANCES COPPOLA11:43And governments will have the power to shut people out of the payments system…

I think I might become a Bitcoin maximalist

Good point Robert

Izabella Kaminska11:44@robert makes a really good point. A CBDC would only exacerbate a bank run in the current situation.

They wanted frictionless banking, but they got frictionless bankruns instead.

FRANCES COPPOLA11:44In all the central bank papers on CBDCs, the prospect of disintermediating commercial banks is their principal worry

Izabella Kaminska11:45The Positive Money and MMT crowd people will be happy though

isn’t this what they wanted? the end of private banks and state money for all?

FRANCES COPPOLA11:46Positive Money wanted private banks only to do lending from voluntarily at-risk deposits. Rather like the Earn programs in crypto – you volutarily opt to put your deposits in a pool from which they would be lent out.

Izabella Kaminska11:46Everything is either state guaranteed or a private sector MMF/stablecoin.

FRANCES COPPOLA11:47The problem with keeping CBDCs small is exactly the same as the problem with keeping low limits on deposit insurance. It means really important deposits such as corporate working capital can’t be kept in CBDCs

Izabella Kaminska11:47Yep, agreed Frances. The issue is how the system keeps allocating wealth into real innovation with proper incentives. Doing so only on a fully funded basis, is going to make non-government backed innovation extremely expensive and much harder to do.

FRANCES COPPOLA11:49There’s also a credibility problem if you limit CBDCs to small deposits then when there is a crisis temporarily open them to all – which is what the Fed has effectively done with deposits

Izabella Kaminska11:49I went to a lecture with Mariana Mazzucato the other day. And I am in fact quite a big fan of hers on many fronts. She makes many good points, and her new book which trashes external consultants sounds great. But I was troubled about the limitations to her “entrepreneurial State” thesis. She always presumes that throwing loads of money at something will deliver results no matter what. But actually, without private sector incentives innovation can easily go down a blind alley.

Of course it looks like the VCs have done a pretty crappy job having supported loads of zero-sum unicorns, so are flying a poor flag for the private sector – and one of the reasons tech is exploding is because so much of it was being supported by cash burn rather than productive income generating business. We went from too much short-termism to too much long-term patient capital (as Mazzucato likes to call it).

But while I agree we need time for a lot of innovation to evolve, the problem with too much long-term patient capital is that it requires a cult mindset and continuous “belief” in the cause – and the problem with cult mindsets is that they don’t know how to let go when things aren’t really working. And this is what worries me. The Entrepreneurial state can go wrong. We saw that in USSR.

And that happened because of bad incentives. And I would argue the reason the private sector has let us down this time, in terms of managing those bad incentives, is because it too got skewed by too much cheap money.

Which is a good op to talk about the UK I think.

11:52What do you make of the HSBC takeover of SVB? I think nobody is talking enough about the security aspects, given HSBC is basically now an arm of the Chinese state. I was initially confused why they would want SVB, as they’re not a particularly tech friendly bank.

But someone pointed out how closely these these tech start ups operate with the UK government here.

FRANCES COPPOLA11:52I think they were leant on because the Treasury really didn’t want a tech startup taking over SVB UK

The Bank of London put in a serious bid

Izabella Kaminska11:53But the government angle is important. The relationships with the tech sector (and via that SVB) are either arms length, where a start up comes in, gets a loan, and is seen as viable because it has first dibs on a government contract through matey connections in White hall (a la PPE contract abuse) – which makes it a no brainer to fund for SVB

Or it’s direct co-investing with The British Business Bank

Or it’s some other government programme.

And of course Rishi being the Tech/Goldman Prime minister, he can’t be seen letting either the financial system or the tech sector go down. That heightens the incentive to keep pumping money into crappy never going to deliver start-ups.

But what’s the moral hazard in bailing out failing tech firms? Surely even worse than bailing out failing banks.

FRANCES COPPOLA11:55I spoke to someone who runs a biotech startup and had funds in SVB UK.

He said the problem was that businesses like his had to bank with SVB UK because the big banks wouldn’t deal with them. So this is a game changer for them in terms of access to the main UK banking services.

he says now a big UK bank is effectively giving tech startups banking services

Izabella Kaminska11:56But the core banks don’t want to deal with them because either they’re doing pie-in-the-sky things, engaged in dodgy crypto fintech, or pursuing high-risk activities – and banks were told both to take more risk (via cheap money) and not to take it (via regulation).

So now a big UK bank which is really a Chinese fifth column has taken it on instead.

This wouldn’t have been a problem 7 years ago – but everything I read suggests they’re not our friends anymore

What’s in it for HSBC other than we did you a favour UK government, now you owe us one.

FRANCES COPPOLA11:57HSBC has for years now been uncomfortably sitting on the fence regarding China

Izabella Kaminska11:57And if you thought the Credit Suisse opco holdco division was confusing, wait until we unbundle HSBC

FRANCES COPPOLA11:58It will eventually have to make a decision about whether it is a British bank or an Asian one I think.

Just as CS will have to decide whether it is a safe boring Swiss bank or a freewheeling internationl bank.

Izabella Kaminska11:58We are nearly at the hour

but worth pointing out Credit Suisse is down nearly 10% since we started the session.

But I’d stress 10% of a small number is still a small number, and the percentages are going to get very distorted as a result.

FRANCES COPPOLA11:59Haha, we’ve crashed its share price with our discussion!

Izabella Kaminska11:59Nonetheless it is concerning I think, that the market hasn’t picked up on the divide. But I don’t want to finish without talking about DURATION RISK.

I spoke to Nouriel Roubini this week: Here’s the politico story I did on the back of it:

That’s the dumbed down version. But what didn’t get in there as it was deemed too wonky for Politico (which is fair enough) was the following, which I am going to paste in here instead:

From a regulatory standpoint, Roubini said the system had been blind to the severity of the issue because banks, unlike other financial institutions — and despite all the crisis regulation — were never required to mark these assets to their present value, known as “mark-to-market” accounting. This, he noted, was a big regulatory failure.

I did not know that!

That Hold to maturity didn’t get M2Med unless it moved into the trading book.

FRANCES COPPOLA12:03SVB took $15bn of unrealised fair value losses on its HTM portfolio, none of which was in the accounts.

Izabella Kaminska12:03Now it’s also the case that I spoke to a former prominent cbanker and his take was as follows:

Regulators weren’t convinced by the idea that central banks and rate rises were to blame. One former British central banker, who spoke to ME on the condition of anonymity, said for banks to have missed this sort of risk would have amounted to incompetence. “It’s bog-standard interest rate exposure, not sovereign default risk,” the banker said, but admitted that if some failed to do it then perhaps some others were exposed.

Roubini agreed banks could have taken better precautions by investing in shorter-duration Treasury or government securities that rewarded lower returns. “They took a huge risk and they f***ed up, big time,” he said.

Now S&P have come out saying they don’t think this is a risk, but Roubini I think makes a fair point that this market risk is somewhere in the system.

If it’s not the banks (and btw I also spoke to a former rates trader ahem who said that it was quite common for the HTM portfolios not to hedge btw), then it must be the hedgies, or maybe even the Asset managers, pension funds etc sitting on these floating rate exposures

FRANCES COPPOLA12:05Hedging HTM portfolios is pointless if you really are going to hold them to maturity

Izabella Kaminska12:05this is what the trader said. They also said it’s really hard and quite expensive.

FRANCES COPPOLA12:05The problem is that SVB, Silvergate etc had to sell HTM securities

And when you do that you crystallise the fair value losses you haven’t recorded in your accounts

Izabella Kaminska12:05Right, and this is why the Fed giving liquidity AT PAR is so important.

It’s basically assuming the lifetime value of a HTM bond

FRANCES COPPOLA12:06Yes exactly!

So the Fed is taking the interest rate risk

Izabella Kaminska12:07@bruce – that’s exactly what Roubini said. Too much of this is unhedgable. BUT! Speaking logically, it’s only going to be as much of a problem as the cash that the cbanks drain from the system.

It’s musical chairs by design

And in theory it’s only the banks or entities with the weakest links that will end up without a chair. Which is kind of the point. What’s the phrase about how we find out who is swimming naked when a crisis strikes?

FRANCES COPPOLA12:09Also if you sell any HTM securities you have to move the whole porfolio to AFS and mark it to market, creating lots of unrealised losses too, which affect the bank’s capitalization.

So being able to pledge HTM securities at par solves both a liquidity and a solvency problem – temporarily.

Izabella Kaminska12:09I believe this is why people are worried about Charles Schwab, because a lot of that unhedged duration risk is sitting in the HNWI portfolios in theory, and is being held to maturity – does that make sense?

FRANCES COPPOLA12:10Yes that’s exactly what’s wrong with Charles Schwab

Izabella Kaminska12:10Does Schwab have access to the Fed tho?

I suspect no. In theory, it’s an asset manager, and has quite a thin layer of capital itself

FRANCES COPPOLA12:11If it hasn’t that might explain why its share price is red. Though it does have a bank.

Izabella Kaminska12:11On that last point,I just wanted to flag the UK budget, which Hunt presented as a fait accompli and so far the markets have absorbed it all because so much crazier stuff is going on. But I did notice this from the DMO head,

And it speaks to duration risk on the UK government side (this is from my subscriber paywalled service.)

The Debt Management Office’s chief Stheemansaid on Wednesday that global financial markets were stressed and volatile and that despite everything the UK’s 2023/2024 financing needs were a very large amount of money, and this is why the agency was now focusing on issuing more short-dated gilt supply. “Short-dated gilts are the easiest way to raise large sums.”

The reason that’s concerning is that it puts government financing increasingly at the mercy of short-term market conditions. This would be coupled with an £7.5bn expansion of the government’s national savings & investment products to tap retail savings.

(That’s me quoting myself btw)

So the DMO moving ever shorter down the curve…

That’s pretty glaring no?

If the UK can’t finance long? And why on earth didn’t it take advantage of the QE zero rate era to do perpetual issuance? Or very long term date? I guess if it did there would be even more HTM risk out there.

FRANCES COPPOLA12:14DMO is trying to limit interest rate risk

Right now floating rate or short-term debt is less risky than long-term, ask any mortgage holder

FRANCES COPPOLA12:16

FRANCES COPPOLA12:16This is Silicon Valley Bank’s parent

Izabella Kaminska12:16Will have to digest that.

FRANCES COPPOLA12:18SVB Financial Group – SVB’s parent – has filed for Chapter 11 bankruptcy.

Izabella Kaminska12:18I think on that note we are going to wrap up. But it’s been another extraordinary week. If you enjoy these sessions PLEASE do recommend others, you would really be doing us a favour. And remember, we are back next week EVERY DAY. Anjuli is here on Monday, with Ben Harrington, but Frances will also stop by to give the bank update if needs be. And then she’s hosting Tues-Thur by herself (maybe with Anjuli if she can free herself up).

If you want to direct people to sign-ups do it here:

Thank you for joining! And thank you to Frances 🙂

FRANCES COPPOLA12:19it was fun! Bye all

Izabella Kaminska12:20????????

One Response