…

10:59Good morning and welcome to Spot Markets Live, the weekly round-robin of stocks and markets news. Today I’m excited to be joined by Helen Thomas, CEO of BlondeMoney, an elite macroeconomic consultancy which you can sign up for here:

Welcome Helen !

Hello everyone!

Thank you Anjuli for the invite

Shall we kick off with a bit about your background Helen? It sounds very impressive from your website.

I have worked in both the City and Westminster

Sell side, I started out in 2001 at Merrill Lynch on the FX desk

Buy side, I ended up at SSGA running currency alpha

But in between I worked in politics

For George Osborne when he was Shadow Chancellor

So it’s a real mix

That must’ve been interesting…

Oh yes!

I was there when Lehman went under

I remember George walked in that morning and I was reading the newspaper (how old fashioned) and he simply said “I bet you’re glad you’re not doing that anymore”

Instead you were saving the system !

hahaha well…. trying….

During that period I ended up listening into the calls with John Varley but also with Swedish politicians who were sharing experience from when they had their banking crisis decades before

anyway

this is probably very dull and historical for all the cool young people on here

They only see markets go up 😉

Well, until now…history repeats itself and all that

Ok so where shall we start?

Markets are having a down day off the back of that surprisingly strong US Labour data on Friday, some hawkish comments from the BoE this morning and ahead of some economic data out later this week.

I think you are absolutely the perfect person to have with us today Helen…should we go straight into Liz Truss’ 4,000 word essay? Have you read it? I like the part where she was instructed to “get back home woman and start hustling”

hahahaha

Here’s the opus

Yes I was left thinking which MP was that ….

Any giveaways in that style of speaking?

A man of a certain age I reckon

but anyway

the essay is kind of the good the bad the ugly

Shall I put up a few highlights?

yes pls do

it’s pretty wide ranging

Her justification for not including the OBR:

There were concerns in some quarters that the announcement would not be accompanied by forecasts from the Office for Budget Responsibility (OBR). However, the OBR’s core purpose is to produce twice-yearly forecasts on whether the Government is on track to meet its fiscal targets. Commissioning a report at that juncture would not have been appropriate, given that the forecast would have been unable to take into consideration the future spending decisions we planned to outline in the Medium Term Fiscal Plan a few weeks later.

It’s also worth recalling that no OBR forecast has accompanied many other fiscal announcements, not least the Covid-19 furlough scheme, which cost £70 billion.

it’s well worth a read for markets people as she actually refers to the markets so much !

Her 45p tax rate shocker :

There were some concerns about the abolition of the 45p tax rate, a small measure and virtually the only one I had not trailed during the leadership campaign. We were simply returning to the top rate that was in place for the vast majority of the 1997-2010 Labour government, although clearly the political sands had shifted.

So I have to say

on the 45p rate

11:07when I was watching Kwasi give the statement, of course my jaw dropped because it was such a surprise… but then I started thinking about when that rate got put in and how it was under Brown

well it was 50%

then Osborne cut it to 45%

but basically that in the scheme of things this is pretty recent history and it was all done in response to banking crisis

and yet it was treated as if it had been around forever

and it is fascinating how certain things become conventional wisdom

conventionally accepted

Well, isn’t that the current criticism that the Tory party has moved so far left it is basically the Labour Party in disguise?

yes and then Truss/Kwarteng was far too much of a lurch back to the right

but the bigger question

is what has happened to the electorate

I think Liz and Kwasi were surprised that even people in the City on the 45% rate didn’t want it abolished

they’re kind of stuck in a Thatcherite time warp and the truth is that the old 1980s left vs right needs to be redrawn for a new world

Yes, that was a shock, similarly on banker bonus cap albeit for different reasons

The important thing in all of this political noise is to recognise the change in the electorate

it’s not just in UK, it is across the western world

How do you think they have changed and why?

After 2008, the electorate split between pro and anti establishment because the system wasn’t working, the banking crisis bailed out the rich and people were fed up (understandably)

so then any leader who could portray themselves as outside of the establishment could win big

hence Trump, Brexit, even Macron, Syriza in Greece etc

A la Nigel Farage

exactly

but then 2020 pandemic comes along

and it’s the perfect storm for those who hated the establishment, because ONLY the establishment could step in

the State had to get bigger

the State puts the vaccine in your arm

so now the electorate is splintered again

authoritarian v libertarian

I like to frame it like this

“Take Back Control”, such a simple solution

but for some people it meant “Take back control for my parliament” = authoritarian, for others it’s “take back control for me” = libertarian

That’s really interesting … but at what point and how does the backlash begin

and that’s why now the old Trump routine and Boris routines don’t work

backlash already begun

that’s why we have 3 party coalition in Germany for first time

Macron attacked by left and by right in his own parliament

Italy, first quasi-fascists in power for decades

none of them can govern

Is left and right as we know it fundamentally no longer the way an electorate splits?

This is important for markets because it neutralises fiscal policy response

yes that’s a good way to put it Anjuli

you can see the havoc it plays in Germany in response to Ukraine

leaders are consumed domestically

hard to do anything with foreign policy

I see Darren has asked a question that optimistically suggests politicians might solve some social issues

I doubt it

because we need a whole new generation of politicians

and a whole lot of crises first

I would put Italy back on list of tail risks this year

Italy debt default risk / spread widening

Bund-BTPs

What will that mean for the Euro Zone?

It will be another eurozone political crisis … although it will not be existential… usual thing where it all looks like it will blow up but it will survive. This time.

The ECB will have to activate its TPI tool

the new Transmission Protection Instrument

What’s that ? I haven’t heard of that one

They’ll step in to prevent market dysfunction in the spread between BTP and Bunds that will emerge when Italy debt comes under pressure due to higher interest rates and lack of growth

so TPI is yet another piece of alphabet soup the central bank has come up with to try to solve issues

If you remember, Christine Lagarde said initially she wasn’t there “to close the spreads”

but that’s exactly what the new tool will do

the thing is, nobody really knows how it will work because they haven’t had to activate it yet

they hoped by announcing it, would be a bit of a Whatever It Takes moment and its mere existence would mean it wouldn’t have to be used

but that’s before they had to jack up interest rates as inflation got into double digits

Ah, interesting

from their website:

The TPI will be an addition to the Eurosystem’s toolkit and can be activated to counter unwarranted, disorderly market developments if these pose a serious threat to the smooth transmission of monetary policy across the euro area. In such a case, the Eurosystem could purchase securities from individual countries in order to combat deteriorations in financing conditions not warranted by country-specific fundamentals. These purchases would be made on the secondary market and would focus on public sector bonds. Purchases of private sector securities could be considered, if appropriate. The scale of TPI purchases would depend on the severity of the risks facing monetary policy transmission. Purchases are not restricted ex ante.

It’s a bit like what the BOE ended up doing to Gilts due to the LDI blow up

and similarly tricky to announce bond purchases even as they’re trying to sell bonds via Quantitative Tightening

BOE managed to get it done and exit for a profit, amazingly

but then there’s still a lot of liquidity sloshing around the system so these blow ups haven’t yet become systemic

Is it just Italy, or are other countries at risk ?

Last year we basically had the default of the London Metal Exchange and the blow up of UK pensions, along with FTX…. but didn’t quite turn into full contagion… but this year the market has to get used to Higher-For-Longer and genuine liquidity withdrawal

Italy is the main one to focus on

As someone has pointed out in the comments, Italy is the big one

that always needed to have some kind of backstop because it can’t really finance itself

That’s true, it’s always been the gorilla

yep

In this context, does the UK look in a relatively good position? Just trying to counter balance the doom

Also, before we move on just wanted to get your take on Truss’ LDI comments

However, brewing in the background there was an issue relating to pension funds, which neither of us had been made aware of – a problem that would ultimately bring my premiership to an abrupt and premature end because of the panic it induced.

At no point during any of the preparations for the mini-Budget had any concerns about liability-driven investments (LDIs) and the risk they posed to bond markets been mentioned at all to me, the chancellor or any of our teams by officials at the Treasury. But then, late on the Sunday night, came the jitters from the Asian markets as they opened. I was alerted to this on the Monday morning, at which point the Bank of England governor was wanting to make a statement on LDIs.

Readers will not be surprised that, given their impact on events, since leaving office I have spent some time looking into LDIs. I was shocked by what I discovered.

Only now can I appreciate what a delicate tinderbox we were dealing with in respect of the LDIs.

Was this really such a Blind Spot ?

And how much is the BoE responsible?

BOE is definitely responsible, along with FCA and PRA

they had mentioned LDI issues previously but never said what they would do about it

they’re doing the same thing now when they talk about financial stability risks

Andrew Hauser is a great guy at the BOE, well worth reading his speeches

but even he said that what they’re doing is “monitoring”

Can I post in here an article from Risk magazine

yes sure

one sec while I find it. From early September. What’s most shocking to me is how the LDI schemes were ALREADY struggling to meet margin calls because interest rates had been going up AND that they had been leveraging up by rolling up their profits on their interest rate swap structures

Yes, it seems to me that if you weren’t aware of this building up you shouldn’t have been in the job

Whilst you’re finding the article thought it would be interesting to get some of the reaction

Anjuli Davies11:27

Anjuli Davies11:27Crispin Odey, who of course made a fortune from shorting the pound had the following :

Hedge fund tycoon Crispin Odey has said that “we probably need a Labour” government to force the Conservative party to rally behind the low-tax economic agenda advocated by Liz Truss.

Reacting to the former prime minister breaking her silence on her 49 days in Downing Street, the City investment manager conceded that last autumn “wasn’t the right moment” to thrust Trussonomics onto the British economy.

Mr Odey had been a prominent supporter of Ms Truss’s plans, but said in hindsight that announcing when “everyone is very poor” had proven a mistake.

“This Conservative Party looks like Ted Heath’s Conservative Party,” he said. “It has stolen the policies of Labour the whole way along.

“It has stolen the policies of Labour the whole way along… The trouble is that we probably need a bit of Labour.”

He added: “Strangely, Liz Truss isn’t a million miles away from where they [the Conservative Party] should be. This will be the agenda for the Tories when they’re trying to get back in.”

Jeremy Hosking, the financier behind Marathon Asset Management and Hosking Partners added: “The Truss/Kwarteng reforms were a well considered and justifiable approach to reinvigorating Britain’s growth prospects, that had a lot of contemporaneous support.

“The Conservatives entirely mis-diagnose the source of opposition to ‘dry’ economic policies.

“The establishment elite or Blob that controls Britain has been captured by leftist progressive ideologies riddled with political correctness.

“Before any sensible economic policies can be adopted a culture war needs to be fought in educational establishments and other infiltrated institutions, including the civil service. The Conservatives dearly want to avoid this at all costs, but this obstacle is no longer ‘swervable’.”

Crikey

that’s punchy

!!

yes, post-facto

I think that trying to blame it all on the blob doesn’t help the argument

nor does Crispin’

saying it “at a time when people were very poor”

how crass

I have often found that Westminster and the City talk in very different languages

But does ‘the blob’ need to move away from its orthodoxy?

Although they’re both right that the Tory Party is having a battle for its soul and also that it is important to challenge the economic orthodoxy given we have had such a huge economic shock

It’s very crass…

I always say, business is about what works but politics is about what sells

you’ve got to make the argument

the truth is that central banks do this all the time

Powell tried to convince everyone inflation was transitory

now he’s trying to convince everyone they’re doing Whatever It Takes To Kill Inflation

and for some reason the market didn’t believe the transitory story even though that is to some extent what we will see

we weren’t going to sit at 8-10% inflation

We reached out to Izzy for comment and she came back with

“The reality is the UK has no other pathway out of the situation without debt monetisation. It’s like one of those Sci Fi space dramas when the crew realises that to get out of a gravity doom loop vortex, they need to lean into the crisis to slingshot themselves out “

we were going to settle at 4-5%

from a 1-2% world previously

hahaha Izzy always has a good metaphor ready !

I think the UK isn’t always as bad as it looks. You have to remember our national press love to tear everything down

just look at our poor England football managers

Like Darren said, who’d want the job…

I’d do it!

I would love to be England football manager

or indeed Prime Minister

Rishi was my year at Oxford

same degree

#HelenforPM you heard it here first

ahahhahahha

Did you know him?

Yes

Not a best mate or anything like that but yes would see him at various things

ha ha @JohnDC77

ahahahahahahahah

there you go!

exactly

Rishi a bit like that too. the quiet studious one

Talking of rates and inflation then , what’s your latest ?

Catherine Mann has been talking this morning

From The Telegraph: Catherine Mann, a member of the Bank’s Monetary Policy Committee, said uncertainty around when the turning point for inflation would come “should not motivate a wait-and-see approach” over setting interest rates.

She has been uber hawkish

Ms Mann, one of the most hawkish members of the committee, warned business leaders in a speech today that “the consequences of under tightening far outweigh, in my opinion, the alternative”.

I Was surprised by how candid she was at the annual BOE Watchers Conference which took place end of November last year

the BOE speakers were all getting asked Qs about policy mistakes, not tightening quick enough etc etc

and she just said, well I always voted for big hikes so I didn’t make the policy mistake

sorry that was meant to emphasise the “I”

I am not the best typist

I feel a bit for the BOE

A clock is always right twice a day…

they actually started hiking first

and then got all the criticism

well not first, but before ECB and Fed

they should have done bigger hikes sooner and started QT earlier

but

they were probably worried about systemic reaction

step forward LDI when they did start going for it !!

The central banks are in a complete pickle

They have schooled the Pavlovian response in the market that when the sh1t hits the fan, they’ll cut rates

So now for some mad reason, even with rates having only just got towards the peak, there’s the obsession with when they’ll be cutting

Go back to 1994 US rate hike cycle… after they hit the peak, they stayed within 75bp of that for 7 years

Yes, it’s hard to believe how the conversation has moved in that direction now

as in, in normal times, it’s not about starting to cut again

it’s not like ZERO is the baseline interest rate

we had 5% base rate for years in the UK didn’t we?

although it has been since 2001 so …. I get why there is that reaction function

yes… I locked into a mortgage at 5.75% in August 2007 so don’t talk to me about it

That’s why I’m not a trader !!

unlike the audience for this chat

you might also remember that UK CPI hit 5% in aftermath of financial crisis, or I might need to check that it could have been 2012

but either way, it was weird how everyone got hysterical when CPI started to go up because in the UK at least it had been at that level in recent memory

obvs it got a lot higher

Anjuli Davies11:40There’s also the ticking debt timebomb

but that is a lot to do with Mr Putin

SO

here’s the thing

I’m not worried about debt

for once

AH, do explain why..

This is not a normal economic cycle

it’s not a cycle at all in fact

I wish we would stop banging on about inflation and/or unemployment rates

it’s like an aeroplane going into a stall and someone just looks at one irrelevant indicator on the dashboard

The whole world changed as of March 2022

we got the technological revolution compressed into a 12 month period

and governments had to take on a lot of debt to manage the schism between two regimes

it’s going to take a decade for the economy to settle into its new shape

I mean even that US jobs number

so it turns out that there was MASSIVE immigration

and 91% of the migrants got jobs

so that is how you get lots more jobs, but NOT much higher wages – average weekly earnings fell

participation rate went up

and the reason for the big migration is that the whole world is reassembling itself

Fascinating

US will get to its new equilibrium first because it has such a flexible labour market

you see it already

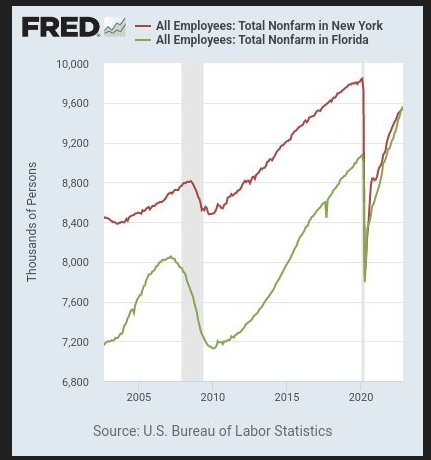

there’s now more jobs in Florida than NYC

I’ll post chart in a sec

people don’t want to be care home assistants when they can be Amazon delivery driver

So, does that mean the FED will pause?

Feb 14 I think is the next CPI print

no I don’t think they pause

or rather I think this relates to what one of the contributors said

about no fed dot plot cuts until 2024 at least

Kashkari’s new year blog is the key here

let me post link

here’s the chart you just posted

Once we see the full effects of the tightened policy, we can then assess whether we need to go higher or simply remain at that peak level for longer”. Those are the two options: higher, or high-for-longer.

thanks Anjuli !

Powell speaks tomorrow in Washington DC

5.40pm UK time

I think he reiterates that message. It’s pause, or hike.

that’s it for the year

rather than “Pause and then cut”

BTW if that kind of migration continues into the US, then you might just get the nice soft landing…

growth, employment, but not too much inflation

as labour supply comes to meet labour demand

The BLS report said that most of the migration was male, from Asia… would be intriguing to know if that trend continues or what prompted it

we need to watch migration data for rest of the world to see what happens to labour market

but this is why the unemployment rate tells us so little

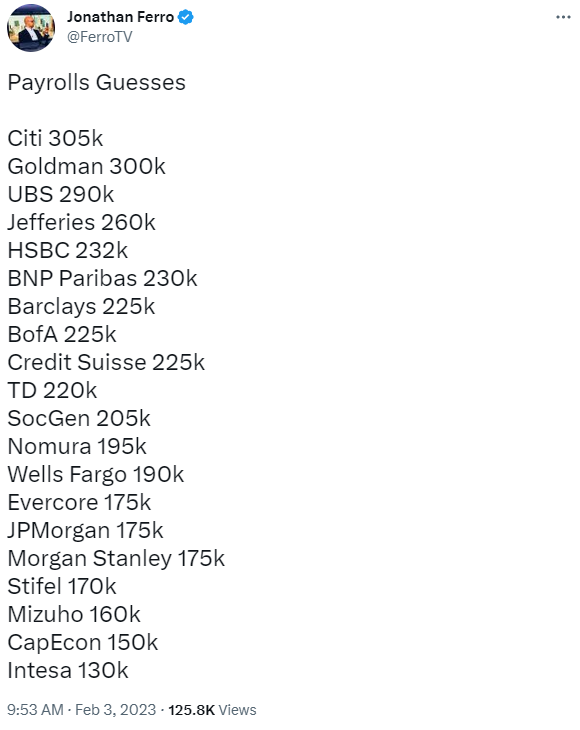

Why is so much of the data coming out “blindsiding” the markets

if you look at the predictions for NFPs last week

the reason there’s so many jobs available for pub staff is because nobody wants to do it… and the pubs should probably not be offering all the services they offer because people have got used to leisure at home, or going out to eat at a restaurant etc. There have been HUGE changes in life/work habits and there are still zombie jobs and companies going because of all the economic stimulus from 2020-21

I have a lot of sympathy about predicting data right now

I mean

it’s tough enough at the best of times

but

we shut down the world economy several times in separate stages and then pumped a load of heroin into the patient and then turned it off and then made the patient get out the hospital and go for a run

to mangle metaphors

I like it

it’s just impossible to estimate this stuff

Go back to 2008-09

about 4 years later the US statistics office revised GDP growth

it had fallen far more

than they thought at the time

and that was just because a bank went bust

this time we have had a global breakdown

it never ceases to amaze me that the beautiful optimism of humanity means we should expect everything to be “normal”

It must be impossible to trade the data then at the moment

kind of

I think it’s like poker

it’s all about what’s in the other guy’s hand

as my boss put it to me at Merrill when we used to play liars poker on the desk

What’s everyone else thinking and how does this particular piece of data relate to that

but that’s just for short term

you also need to keep an eye on options gamma

that’s one of my fave topics

Do go on…

I’m this macro fundamental person who has had to accept that the options market moves the spot market

not to talk down to the learned people of this group

but basically

options market makers are the only people who have to trade every day because one of the factors they’re managing is time

as time decays, the option price changes and therefore the hedges change

that’s the first thing to say

second thing is, what’s the overall position. are the options market makers short or long of gamma

without boring everyone to death

short gamma means they sell on the way down and buy when it goes up = exacerbates price action

long gamma is opposite = rangebound

and most of the time they’re long gamma because that has paid off

it goes back to central banks and all the money they pump into the system, that bears down on volatility so these guys tend to soak up all the vol selling and then just buy low and sell high all day long

Is this why people like Citadel are doing so well?

This guy is great

their market making business

you can follow him on Twitter, he’s called SqueezeMetrics and he has measured the Gamma Exposure of the market with an index called GEX

and yes that’s right about Citadel

although the added way to make money is to know when to take a bit of prop risk alongside

Of course

so when to hold on to some of the risk you’ve been given rather than clearing it all completely

and because they see so much flow, they tend to know which way the market is

etc etc

but the reason this all became so important is because of explosion of interest in volatility trading itself

so look at open interest on the VIX, it exploded after 2008

so now it’s “tail wagging the dog”

people are trading zero day to expiry options

and it’s all adding up to having a big impact on day to day trading

anyway I know we are almost out of time!!!

Helen, we have three more minutes, though I could go on talking to you for much longer… is there anything you want to highlight from Blonde Money that we NEED to read/listen to https://blondemoney.co.uk/

March 6th 2020 I wrote “It All Comes To Nought” – deliberate pun because of interest rates going to zero just as economy going to zero

that’s where I introduce impairment in the velocity of people, that’s still ongoing

Then this week

I will release our Rishi Ratings

where we have analysed all Conservative MPs to quantify how much support there is for the PM

Rishi ratings, I like it

It is not pretty for Rishi

😀

When is that going to be published?

Tomorrow

Follow me on Twitter

or LinkedIn

Brilliant

@MarketBlondes on twitter

We will show the support for Rishi in one chart

nice and easy

Well on that note, thank you so much for joining us today, I hope you enjoyed it and will come back soon !

Thanks Anjuli! It’s been great and I hope everyone enjoyed watching

Have a great day!

Ciao for now

bibibi