How are you, whatcha been up to?

10:32 JR: In recent days I’ve listened to podcasts on Napoleon, from The Rest is History and from Dan Snow who persuaded the historian Andrew Roberts to come on his show and tell us why.

In the face of all evidence to the contrary, he was a great man and didnt in fact suffer from the eponymous complex with which he’s commonly associated.

Napoleon’s letters to Josephine were perhaps the most interesting part.

Apart from James Joyce’s letters to Nora Barnacle I don’t think I’ve read billets d’amour to compare.

He apparently never said ‘not tonight, Josephine, nor did he instruct her not to wash.

Nunc tempus loquendi (aka The Time is Now)

10:35 DGG: Meme of the day:

The Houthis have taken to social media to provide the world with military action teasers.

This was posted on November 25, one day before unknown gunmen attempted to board the Israeli-linked ZIM Central Park tanker before a nearby American gunship came to the rescue.

ZIM – alongside most of Israel’s linked maritime industry, are being forced to divert their routes outside of the red sea, and around Africa.

Quite the nuisance – but to be honest, fixable with more creative corporate registrations in secrecy jurisdictions.

One of my customers in the wine shop is a former marine who spent years fending off pirates off that coast.

They’re essentially a state-backed marine militia

10:38 JR: (He now has a drink problem, because the job was so boring.)

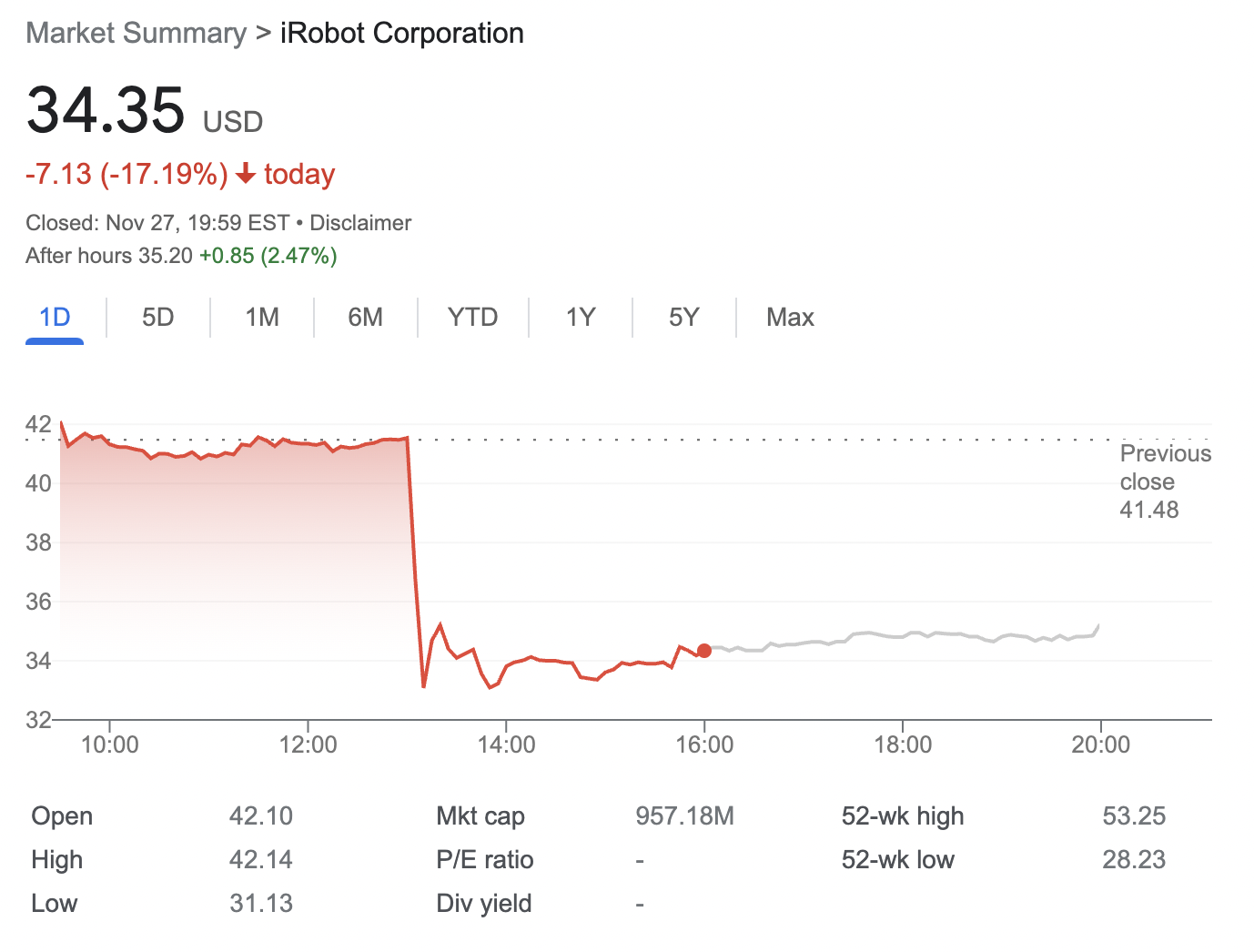

The planned cost of the merger was $1.7bn for the European robotics hardware manufacturer and seller.

Concerns were that Amazon dominates the marketplace for future iRobot competitors, meaning they could easily create anti-competition conditions.

The news comes amid headlines that Amazon has now delivered more packages than FedEx and UPS in the US by volume combined.

Retailer was last valued at $66bn and is vying to start trading on public markets by 2024.

Shein’s fast fashion has been doing well but it’s now facing a lot of accusations about using forced uyghur labour in its supply chains.1

She opined ‘very very cheap clothes and homeware items, comes from china in about 2 weeks.’

‘Can basically buy anything for a couple of quid. Obviously from dodgy warehouses though. She added: ‘always having crazy discounts and deals, very hectic website as well’.

So two things:

1) My daughter’s not that woe bvs.

2) This is v simplistic but that’s how young people assess the brand – cost

Several online posts positively compare Eli Lilly’s weight-loss Mounjaro to Ozempic.

Supposedly real-world studies claim the diabetes drug is an even more effective treatment for weight loss than Ozempic

“Researchers found that patients taking Mounjaro were three times more likely to lose 15% of their weight than those on Ozempic. Patients on Mounjaro were also 2.6 times more likely to achieve 10% weight loss and 1.8 times more likely to lose 5% of their weight.”

“But Monday’s study confirms Mounjaro’s edge over Ozempic in a real-world setting, specifically among adults who are overweight or obese. Notably, head-to-head clinical trials in that population are not yet available, according to Truveta Research.

And now it’s pitted against Wegovy.

Eli Lilly is pitting Mounjaro against Wegovy, a higher dose version of Ozempic approved for weight loss, in an ongoing clinical trial in obese or overweight patients. But results won’t be released until next year.”

News which rounds off a seemingly fantastic year for Eli Lilly.

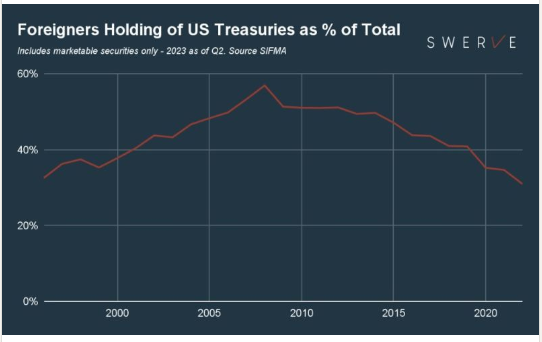

Last night we had a fairly flimsy 2 yr auction in the US but a very robust 5yr auction which dragged down yields across the whole curve.

However, the recently concluded fy2023 budget had a planned deficit of $1.154 trillion, or 4.5% of GDP, which was already significant.

The actual deficit reached $1.695 trillion, marking a 47% overage. Looking ahead, the budget for FY 2024 is set at $1.877 trillion, an 11% increase vs. the already staggering 2023 figures.

The problem this is causing is illustrated by this chart:

And this isn’t just the Chinese selling UST to accumulate gold reserves to back the putative RIC currency.

This is also US institutions unhappy with fundamentals and supply.

The only feasible solutions to rein in the deficit would be to either raise taxes or cut spending. Given the dynamics of U.S. politics, neither of these actions seems likely in the foreseeable future.

Powell speaking this week… like many central bankers at present, he’ll be having to talk financial conditions tighter otherwise all the hard work of raising rates will have been for naught.

I saw a fascinating (and I must confess, satisfying) article in the SCMP yesterday.

Construction of the Power of Siberia 2 natural gas pipeline is likely to be slower than expected despite the ‘no limit’ strategic partnership between Beijing and Moscow.

Which discusses how China is demanding a 40% discount on natl gas prices from the Russians.

As the former British ambassador to Minsk, Nigel Gould-Davis sarcastically put it: this demonstrates ‘The economics of a friendship without limits’

Which is how Xi and the Kremlin Ripper describe their relationship.

China has refused to invest in the Power of Siberia 2 gas pipeline and demanded more gas discounts, The South China Morning Post writes.

Next year, China’s discount rises to 46%: gas from the Power of Siberia will cost $271.6 1000/cm3 and for Turkey / Europe $481.7. China wants more, though. It “can demand deep discounts,” the source says.

“In terms of construction, [Beijing] wants to make sure that they have no risks and no costs. Russia is the side that foots the entire bill,” says the source.

So much for Russia’s pivot east.

This serves as a reminder that the only place you ever find free cheese is in a mousetrap.

Putin’s options are limited.

In fact he has none.

The Russian president is “under enormous pressure” because without the pipeline where else can Russia flog its enormous gas reserves?

It’s lost the European market, the destination for 150mill/cm3 before the war. Gazprom was obliged to cut production 25%, the most on record.

And here are natl gas prices:

The Kremlin Ripper’s going to have to start another war. 30% of Russian budget is now going on the military.

The irony, of course, as I type, is that just as the Russian army has restarted its winter drone offensive, hoping to take down , power heating and water supplies to the capital, Kyiv, the worst storm in 100 yrs, Storm Bettina, has struck the Crimea and left the 500,000 occupiers there bereft of power, electricity, heating, water etc etc.

We saw it here last week, the importance of comparing economies’ military potential with GDP adjusted for PPP, which raises Russia from an Italy-level middling power to a supra-French and German power

“Renowned French economist Jacques Sapir has pointed out the inadequacy of this metric, arguing that Russia’s GDP, when measured in PPP ($3.74 trillion in 2013, $4.81 trillion in 2021), is closer to Germany’s ($3.63 trillion in 2013, $4.85 trillion in 2021) than Italy’s ($2.19 trillion in 2013, $2.74 trillion in 2021). This is a crucial distinction, and it is both puzzling and troubling that so many continue to parrot the Russia-Italy comparison.”

The article also appreciates that despite this already positive change for russia if we measure for PPP, it still underappreciates the strategic weight of Russia’s economy by another weight; wartime resilience:

“Sapir notes that, over the past fifty years, Western economies have become increasingly dominated by service sectors, which, while contributing to GDP calculations, lose their importance during times of conflict. In such situations, it is the production of physical goods that matters, and by this measure, Russia’s economy is not only stronger than Germany’s but also more than twice as robust as France’s.”

“Furthermore, Russia’s dominant position in the global energy and commodities trade—as it is a key producer of oil, gas, platinum, cobalt, gold, nickel, phosphates, iron, wheat, barley, buckwheat, oats, and more—provides it with substantial leverage over markets and economies, making it less susceptible to sanctions and less easily cowed by Western pressure.”

10:59 JR: I‘m not sure how relevant PPP is in a country like Russia where wealth distribution is so highly concentrated.

10:59 JR: Is that the Gini coefficient? Must be close to 1 in Russia?

10:59 DGG: I think the thrust of these analyses is more about trying to judge power-on-power comparisons rather than the welfare of citizens – which is evidently better anywhere in the west

“This love for service sectors results in a tendency to view the labor-intensive industries of the past—energy, agriculture, resource extraction, manufacturing—as antiquated relics. But this skewed perspective has left us unprepared for a world in which tangible goods are once again of vital importance, as evidenced by our struggles in the face of the war in Ukraine.”

“The conflict has “exposed a worrisome lack of production capacity in the United States.” In Europe, the United Kingdom has noted that “it will take 10 years to replace weapon stocks gifted to Ukraine and rebuild British weapon numbers to an acceptable level.” The EU, for its part, now cut off from cheap Russian energy, faces the terrifying possible prospect of rapid deindustrialization.”

What does that tell us here at SML?

That maybe it’s time to start looking at European defence majors?

BAE Systems plc, Rheinmetall AG, General Dynamics Corporation, Nexter Group.

It also tells us Ukraine has done us all a favour in demonstrating how inadequately protected we were/are.

Sounds like we have a little bit to celebrate

As they say, a broken clock is right thrice a day.

Sorry – twice

(I really wanna see the hunger games prequel!)

(or marvels)

The suspect company in question? Sheikh Tahnoon bin Zayed’s G42. (Named after the number 42 in Hitchhiker’s Guide.)

And unlike what we discussed here, references to Microsoft and openAI were only in passing. While they outline that G42 signed agreements with American companies like Microsoft and Dell, all three companies refused to comment on the New York Times’ story.

However – the story is OBVIOUSLY about Altman and OpenAI.

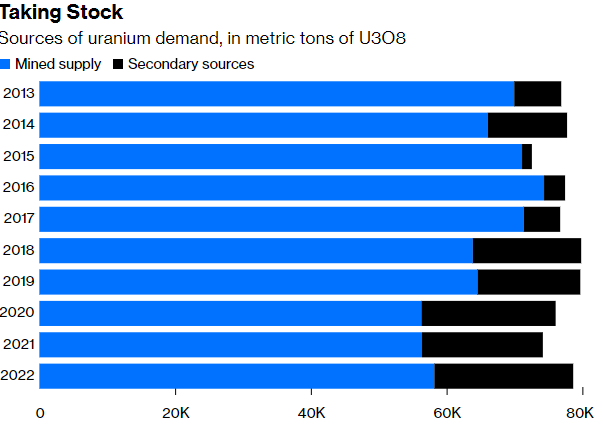

Yellowcake

Great article on bberg, albeit almost two months after SML highlighted the very same.

The most interesting chart in the piece was this:

Uranium best-performing cmdty in 2023, French nuclear plant outages are over, the US is increasing the number of plants, Japan restarting some and China also expanding rapidly.

Nuclear capacity is rising 50 percent in Asia through 2050.

On top of all this, the US may ban Russian fuel, which provided ⅛ of all US purchases last year.

And lastly there is the outsized influence on the market of new financial investors in the asset class..

‘Financial markets have injected some animal spirits into all this. Uranium is a relatively small, illiquid market — think about it, it’s best that way — worth only a nominal $14 billion a year even at the current spot price, making it smaller than the relatively nascent lithium market. So it doesn’t take much in the way of speculation to move the price. There are three listed investment funds physically backed by uranium of which the largest, the Sprott Physical Uranium Trust, just surpassed $5 billion in net asset value. Altogether, they added about 50 million pounds to their stockpiles between 2020 and 2022 as money flooded in, an amount equivalent to almost 30% of annual regular demand for uranium, supercharging the initial rally in prices.’

The bottom line remains the same: uranium is going up but the challenge for investors is to identify a suitable vehicle for exploiting this trend and for some light relief (thank God, I hear the listener sigh).

The next pandemic?

There’s a cheery thought

Have you ever eaten a hairy crab, Dario?

The Hong Kongese are dealing with price rises by exploiting newly reopened border with mainland by travelling there to do shopping and bringing back a delicacy called ‘hairy crabs’ that sound – and look – disgusting.

This, however, is one way for the islanders to defeat inflation because they are prized far above rubies apparently.

I went out with a woman of singular, blood-carbonating beauty in HFK in the early 90s.

11:14 DGG: What is HFK?

11:15 JR: I always called it Hong ****ing Kong when I lived there. Anyway, and everything went swimmingly well until we went out for lunch and she ordered chicken’s feet, which she then proceeded to gnaw on for the next fifteen minutes, thereby ending a beautiful relationship because I could never look at her in the same way again.

But look what it does for travel:

The border reopened properly in Jan this yr.

This may be good for food price inflation but it’s only a matter of time before there’s some kind of crab flu spreading zoonotically and what chance the hairy crab of joining the pangolin and the Wuhan Bat in the halls of gastronomic infamy?

Quite high, I suggest.

Chaynaaa.

I seem to talk about it more than Donald Tramp

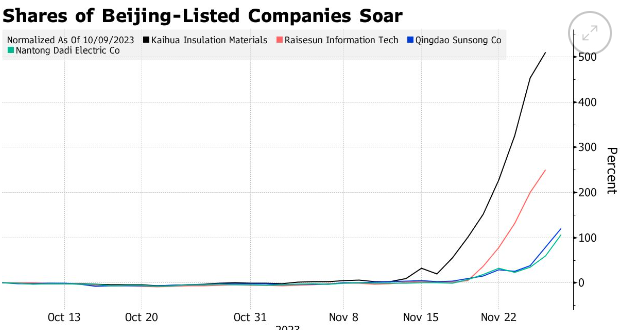

11:18 JR: There’s one corner of the Chinese stock market that is rampant at present and that’s the smallcap index of fifty tech/ innovative industries.

The Beijing 50.

Anyway the Beijing 50 has confounded the bearish sentiment prevalent in Shanghai. It’s up 50% (do not adjust your TV sets, you read correctly) since Oct 23rd.

Of course, the CCP cannot have their citizens enjoying themselves, gambling recklessly and making illegitimate gains without their say-so and so it’s only a matter of time before control is reasserted here and the fun stops.

Unsurprisingly, the index is a febrile rumour mill and fantastically speculative but this frivolity won’t last.

When I worked in HFK in the 1990s I was once interviewed by a local radio company for a news bulletin about the stockmarket.

A friend had suggested they call me for commentary on the trading frenzy taking place in H-shares and had introduced me to them as Julian Moktau which I heard as went on air.

I assumed it meant trader or was some kind of honorific for a gweilo but in fact it meant ‘blockhead’ or ‘head made of wood’ in Cantonese.

Asked about the wild trading patterns I told listeners that the Chinese authorities were about to ban rumours on the exchange and after a suitable pause added that it was only a rumour, though.

‘Thank you, Julian Woodenhead’ said the interviewer.

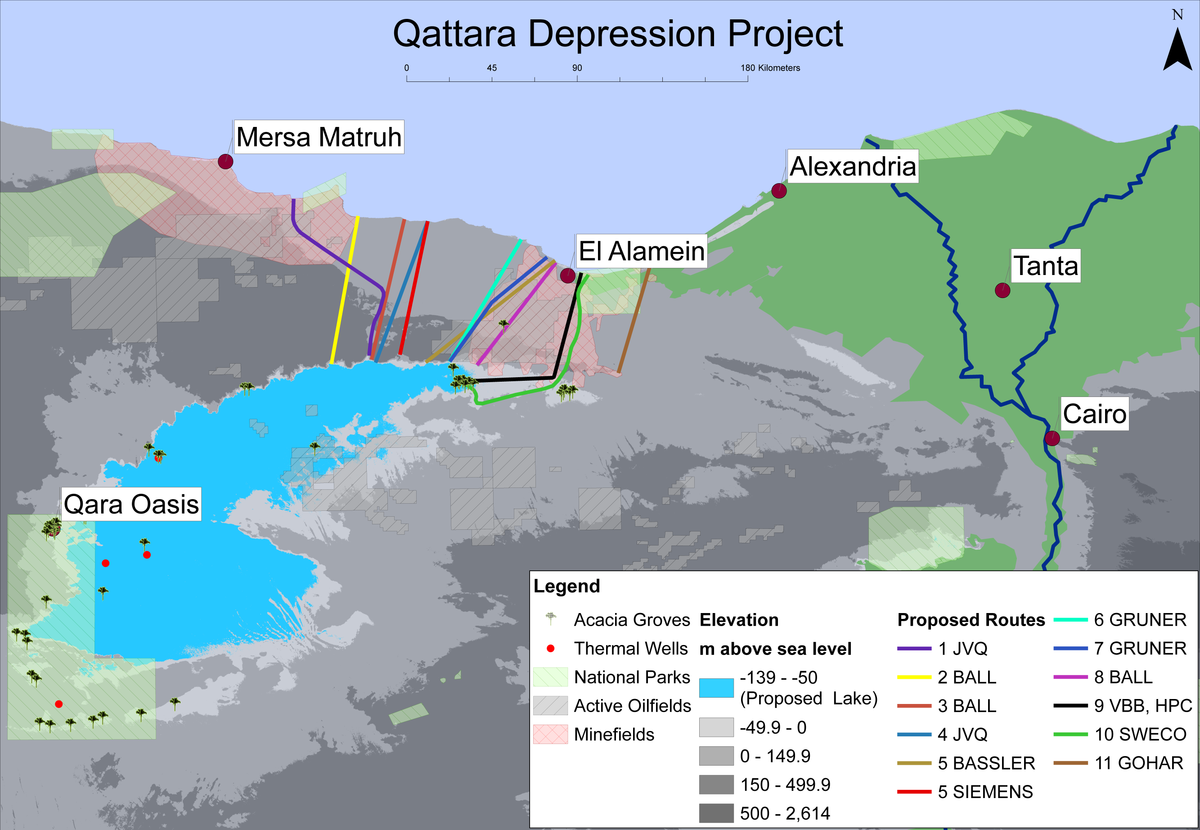

Continuing on from SML’s series on canals and infrastructure projects, let’s overview some Egyptian developments that are rumoured to be heating up again

“The Qattara Depression is a treacherous lowland covering 7,500 square miles in area near the Egyptian-Libyan border. It’s shaped roughly like a huge footprint, as if a giant had stepped from the Mediterranean into the Sahara, and left a big squishy mess. (“Qattara,” appropriately, is Arabic for “dripping.”)”

The layer in blue is actually the second most depressed place in the entire African continent.

Sounds like we should live there, Julian.

This would slowly fill up the lake over centuries due to the high amount of evaporation in the Depression, allowing for continual hydroelectric power use.

Interest in the project was revived in 2023 by the Egyptian Group for International Trade and Consulting, a consortium of international companies which develop projects related to import & export and construction in Egypt, which signed an agreement for a new feasibility study for the Qattara Depression project.

It reminds me of that bonkers nazi project to make the Mediterranean landlocked:

Would have been called Atlantropa.

And just a quick one on Cairo’s New Administrative Capital.

Many people – and practically every single Egyptian I’ve met – have lambasted the project as an evident side-effect of the new military leadership’s megalomania.

As a keen fan of Egyptian history, I beg to differ.

While the problematic specificities of the projects – their gigantic sizes, the fact that most of the projects are run by the military and allegedly (and obviously) involve significant sums of graft money sloshing around – I can only agree with Sisi’s thrust.

While Egypt has faced off a number of regional rivals in the last millenia, and hosted a variety of powerful dynasties like the Mamluks or the Ayyubids, its most significant battleground has always been its traffic-filled capital city and governing Citadel.

The concentration of population, resources, and power in Cairo means Egyptian governments are always in tow to the vagaries of international prices for wheat.

The history books are stacked to the brim with bread-pricing riots toppling successive Mamluk administrations.

Just see how el-Sisi’s government came to be!

Egypt was the Arab uprising’s first victim.

This concentration means there is no other Middle Eastern nation – as far as I can tell – where riots in the capital can so effectively threaten its governing infrastructure.

Though, again, who am I to debate nationals?

One could argue the accountability provided by the closeness to the Cairene rabble makes for better governance.

But looking at the recent history of Egypt, maybe it’s time to try something different.

Egypt will transition to be a much more stable power, methinks

Nunc tempus taciendi