FRANCES COPPOLA10:59

FRANCES COPPOLA10:59..

11:00Morning everyone

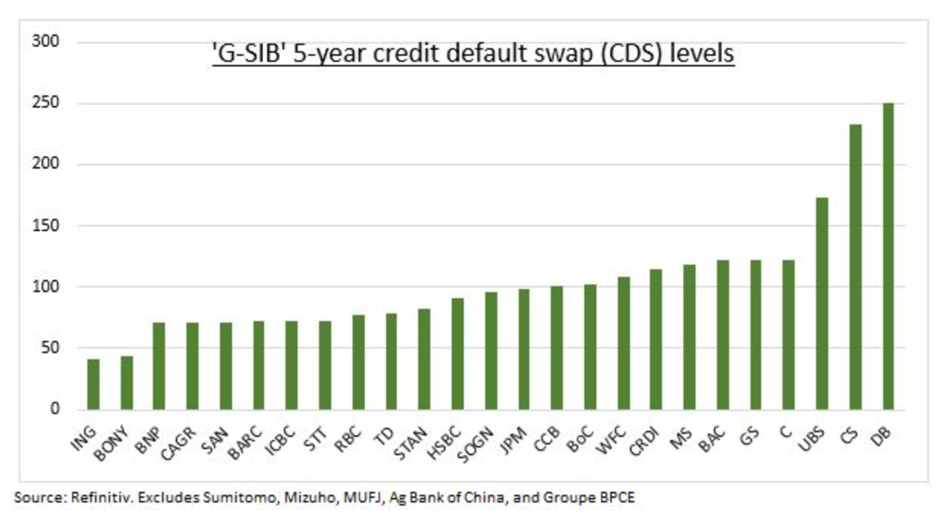

That’s Bank CDS today, from Ben Laidler at eToro, Credit Suisse and UBS are up as expected, and everyone still hates Deutsche Bank.

Stock price has fallen slightly today though it’s still up compared to its value five days ago. Its rival Commerzbank is green, as are other big European banks.

US banks mostly green today. Charles Schwab took a beating last week but is up 0.55 per cent pre-market today. US Bancorp is down, but some analysts are saying it is undervalued.

First Citizens Bank’s decision to acquire most of SVB was well-received by the markets. Its share price jumped by 53.74 per cent yesterday. However, SVB is a very large mouthful for First Citizens Bank to swallow, with assets totalling some two-thirds of First Citizens’ existing asset base, and it is only a year since First Citizens took on CIT group. First Citizens Bank has grown very fast through acquisition, but I’m concerned about management overstretch. I would like to see less M&A and more organic growth.

SVB fallout

FDIC has said it will be left with a loss of about $20bn from the sale of SVB. This will (presumably) be recovered from other banks through a “special assistance” levy.

As we speak, the Bank of England is defending the terms of SVB UK’s sale to HSBC to the Treasury Select Committee.

They said they had multiple bids but lots of them set “impossible” terms. I’m not sure why HSBC’s demand that the ring fence be relaxed to allow the ring-fenced bank to take on SVB UK wasn’t impossible.

They also said they didn’t finalise the HSBC until 4 am. Those who remember the Cyprus bank bailout of 2013 may recall that this wasn’t decided until 3 am and was then rejected by the Cypriot parliament. Tired people make bad decisions.

Sam Woods, deputy governor for prudential regulation, said that HSBC demanded a permanent “puncturing” of the ring fence to allow the ring-fenced bank to take on SVB. Apparently, Woods said this was because SVB dealt with subscription finance, which a ring-fenced bank can’t usually provide.

Here’s what Woods said when asked how much of the business SVB provided can’t be provided by ring-fenced banks (via Izzy who is following proceedings):

I can’t give you a precise percentage, but it would be quite significant for the reason that a certain amount of the lending – quite a significant portion of the book actually — is in the form of subscription finance, which is basically to bridge the investors in venture funds between making the commitment to put money in and actually having the money available. Those clients in that case will often be, I think, well known financial institutions for the purposes of ring fencing which means retail banks can’t normally lend to them. So I think it’d be quite significant, which is why it was a red line for HSBC.

The Skeoch review into ring-fencing and proprietary trading said that the ring-fence should be relaxed in some respects, and the Government agreed to this in the Edinburgh reforms. So is the PRA’s decision to relax the ring-fence for SVB just a prelude to a more general relaxation?

Skeoch review final report is here https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1060994/CCS0821108226-006_RFPT_Web_Accessible.pdf

At the risk of turning this into a live-tweeting of the Bank of England’s evidence to the TSC…

Bailey has confirmed that the Bank of England would not follow the Swiss regulators’ example and treat AT1s as junior to equity.

He also says it should not be “the norm” that all deposits are guaranteed.

Dave Ramsden, deputy governor for markets and banking, emphasises the importance of the bank solvency regime. I wonder if they are thinking of tweaking it to ensure that banks can’t hide fair value losses on securities used to back runnable deposits.

@Graham I agree that the Bank of England probably wanted a too-big-to-fail bank to take on SVB UK. Not just to make depositors comfortable and reduce pressure for unlimited deposit insurance, but also because a TBTF bank is much more closely supervised than a smaller bank.

Bailey says that SVB’s collapse was “fastest since Barings”. Which is somewhat entertaining given Nick Leeson’s new role as a corporate investigator… https://www.theguardian.com/business/2023/mar/22/former-rogue-trader-nick-leeson-joins-corporate-private-eye-firm

Former ‘rogue trader’ Nick Leeson joins corporate private eye firm

Red Mist Market Enforcement Unit advertises financial investigation services to investors seeking compensation

Nick Leeson, the former rogue trader who caused the collapse of Barings Bank 28 years ago, has joined a firm of corporate private investigators.

The firm, Red Mist Market Enforcement Unit, advertises financial investigation services to investors seeking compensation in court cases, according to an interview with Leeson published by Bloomberg.

Nick Leeson is the ultimate in poacher-turned-gamekeeper

Anyway, Bailey unsurprisingly emphasises the strength and stability of the UK’s banking system.

The question is whether it will remain strong and stable when the Edinburgh reforms are implemented. Reminder – On 9 December, the Chancellor of the Exchequer announced a set of reforms to drive growth and competitiveness in the financial services sector.

Despite the failure of Credit Suisse, Jim Reid at Deutsche Bank is upbeat about big banks:

“Large banks in the US and Europe are completely different entities than they were going into the GFC. For large US banks for example, securities and loans/leases on their balance sheets as a % of deposits are lower than when our data starts in 1985 and at below 100% are massively down from their GFC peaks of over 150%. We don’t have the same long term data for Europe, but the declines since the GFC are of similar magnitudes.”

Reid thinks corporate defaults are a bigger risk:

“In contrast corporates are more levered now than during the GFC and this cycle could ultimately be more corporate default focused vs financials as per say 2001-2002 rather than 2008-2009”.

So, dot com crisis rather than shadow banking. Corporates are the customers of banks, so defaults in the corporate sector inevitably affect the solvency of banks. However, I agree with Reid that big banks are pretty well firewalled. Including his own outfit, Deutsche Bank, which in my view is mainly suffering from a long-standing credibility problem known as “it’s always Deutsche”. This is what we might call “Mary Bennet” fragility:

“Loss of virtue in a female is irretrievable; that one false step involves her in endless ruin; that her reputation is no less brittle than it is beautiful; and that she cannot be too much guarded in her behaviour towards the undeserving of the other sex.”

(Jane Austen, Pride and Prejudice)

DB has put an immense amount of effort into repairing its balance sheet and improving its culture, but mud unfortunately sticks.

I’m not sure what the solution to this is. Merger with Commerzbank? Nationalisation? We’ve discussed both of these repeatedly over the last decade.

Over in the US, Bloomberg reported that the Fed is considering providing more liquidity support to banks, particularly the troubled First Republic Bank. First Republic Bank’s shares were up yesterday and in pre-market trading today. But its underlying problem is that it needs more capital, and the Fed can’t provide that. It is still looking for a buyer. Presumably First Citizens Bank is not in the running.

Report just out from Bloomberg that France is investigating five banks for tax fraud.

According to Le Monde, the banks involved include Societe Generale, HSBC, BNP Paribas and Natixis.

Izabella Kaminska11:29

Izabella Kaminska11:29What a time to do that!?

This is like the DoJ deciding to investigate CS and UBS now too.

FRANCES COPPOLA11:29Anyone would think they want to cause a banking meltdown

Izabella Kaminska11:31Andrew Bailey, Dave Ramsden and Sam Woods pointing out the UK system is strong, safe and stable btw

And that if there is an issue with credit conditions the first thing they will do is release the countercyclical buffers.

Which is a sign that they plan to keep raising rates IMHO

FRANCES COPPOLA11:31I agree, and that is also consistent with the message being sent by the Fed

More liquidity support for banks and more rate rises

Izabella Kaminska11:32There was also a lot of talk about liquidity Coverage ratios having to be reviewed

But Sam Woods warned there is a trade off, because if they are too high they will hinder credit creations

FRANCES COPPOLA11:33Surely they need to look at the composition of HQLA in the light of what has happened in the US?

11:34SVB et all were doing “narrow banking”, using long-dated HQLA to back highly runnable deposits

They weren’t doing much in the way of lending to those customers. Loans were much lower than deposits and the difference was made up of “safe” securities. I would have thought they need to rethink the duration of HQLAs. But this also raises a fundamental point about banking – I’ve seen a lot of people calling for either full reserve banking or 100% deposit insurance on the grounds that banks are depository and payment institutions (which is true).

But banks are also lenders and money creators and the more you restrict their ability to leverage deposits to create loans, the more you limit their ability to provide liquidity and purchasing power in the economy.

As crypto has illustrated, a financial system with no fractional reserve lending is about as liquid as the surface of Mars. Hence the proliferation of crypto shadow banks doing fractional reserve lending without the safeguards we impose on traditional (“fiat”) banks. And they have all collapsed like dominos. Just as the shadow banks did in 2008.

Izabella Kaminska11:34

Though MMFs have the advantage right now in potentially sitting in only short-duration assets. But that introduces different risks.

11:42So Sam Woods has a point. There’s a trade-off between the safety of banks and their role in the wider economy.

11:44and I would argue that regulated banks must be allowed to take reasonable risks with deposits, otherwise the risk-taking that the economy needs disappears into the shadows where it is unregulated and open to scams, frauds, ponzi schemes and rug-pulls.

11:46Talking about the economy, the outlook is gloomy. EU monetary conditions tightened considerably in February – intentionally, since this is a result of ECB policy. The fall of Credit Suisse will cause credit tightening on top. ECB monetary policy committee appears split between hawks and doves.

In the US, Philly Fed survey shows a substantial contraction in manufacturing activity.

Services activity also declining though not so much

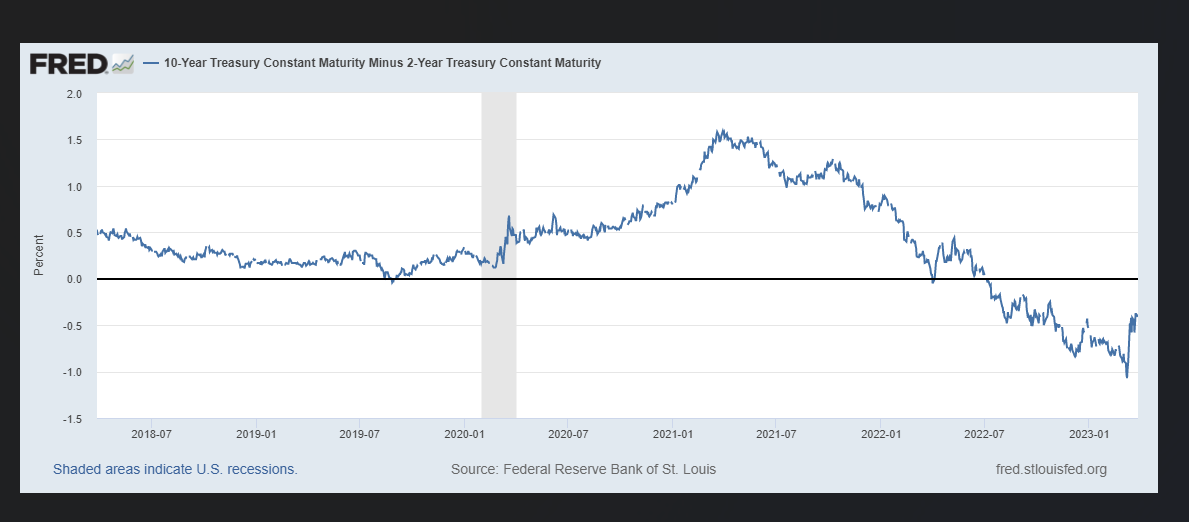

11:50also the 2 year vs 10 year curve is deeply inverted

(yeah I know, inverted yield curves have predicted 10 of the last 6 recessions)

11:53Unicredit economist Erik Nielsen has issued a call for central banks to cut rates to prevent another financial crisis. https://www.bloomberg.com/news/articles/2023-03-27/fed-and-peers-must-halt-rate-hikes-to-avert-crisis-nielsen-says?sref=3roVJZZ4

Global central banks from the US to the euro zone should jointly commit to avoid further interest-rate hikes until market stability has been assured, UniCredit economist Erik Nielsen wrote on Sunday.

“A litany of policy mistakes has brought the western world to the brink of yet another financial crisis,” he said in a report. “Economic fundamentals, including macro balance sheets, as well as the banking system as a whole, are all in good shape, so the repair is well within grasp. But it requires clear, forceful and urgent communication now by key policymakers.”

11:55The present calmness makes this look a bit overblown, but financial crises can blow up out of nowhere, as we know. Are central banks going too far, too fast with the rate rises, and is the financial system really sufficiently protected?

11:56 In the last five minutes I’d also like to return briefly to that question of whether the accord between China and Russia about paying for oil signals the end of the dollar system. George Magnus, China expert, says this is nonsense.

In a thread on Twitter he said that this displays ignorance of the way the international monetary system works, and pointed to the strength of the narrow and broad dollar indices as evidence:

Magnus gives two reasons why the accounting is wrong:

- he says people “mistake the fx redenomination of sino-Russian trade and repricing of some of China’s oil as a dump of the $ which it isn’t because the receivers of yuan still have a demand for $.”

- He says it is the $’s prominence and the investments of surplus nations like China that leads to the US accommodating that demand including by running deficits and chalking up debt. Michael Pettis, also a China expert, makes similar points.

He also points out that China’s alternative payments system to SWIFT, actually relies on SWIFT.

Izabella Kaminska12:00

Though Michael Pettis has shifted his argument slightly on this, saying that even if the US dollar lost its status as the global reserve currency it would be no bad thing.

FRANCES COPPOLA11:33

I think the non-convertibility of the yuan and the fact that neither China nor Russia has a credible safe asset to use as collateral is also a negative for the “yuan will replace dollar” case. However, some seem to be arguing that commodity futures will replace USTs as safe assets.

12:01 This isn’t to say that the Global South, or Global East, or some combination of the two, won’t switch away from using dollars for settlement. But the point is that if they do, the transactions will still ultimately be underpinned by dollars.

12:03 I think of this as a bit like the crypto claim that offshore trading doesn’t use or need dollars. This is true, but the whole ecosystem is still underpinned by dollars, because ultimately people want to realise their gains in dollar terms, and they would really, really like their losses to be borne by the Fed.

12:04We’re coming to an end for today. I don’t think we’ve seen the last of the banking wobbles, but perhaps we should be paying more attention to what is going on outside the regulated sector – as Anjuli said yesterday.

So thanks for today, everyone. See you all tomorrow at 11 am and it won’t just be me tomorrow.