Good morning, aloha and greetings, fellow market wizards.

Welcome to the 25th of October and of course, English patriots among us will know this is St Crispin’s Day

The anniversary of the Battle of Agincourt

and, of course, the battle of Balaclava 1854 which was notable for the charge of the light brigade, a bloody awful, jingoistic, pile of tripe written by Tennyson

I’m joined again this morning by our resident geopolitical zoomer, Dario

Good moaning.

Dario Garcia Giner 10:32

Hola Julian!

Are you inspired by Henry V?

And gentlemen in England now-a-bed

Shall think themselves accurs’d they were not here,

And hold their manhoods cheap whiles any speaks

That fought with us upon Saint Crispin’s day.

Dario Garcia Giner 10:33

The young king will always have my respect.

We shall feel his spirit walking among us as we explore financial markets together.

Warning, this SML contains faint traces of nuts.

So, Dario, following on from your dazzling exegesis of things Venezuelan yesterday I gather there was some big news overnight?

Dario Garcia Giner 10:34

That’s right

If you can read Spanish, this document should make your skin crawl (if you care about northern Latin America, at least.)

It’s a Venezuelan referendum on the question of whether Venezuela should effectively move to annex the Esquibo region of Guyana.

that was prophetic. However, I think readers have had quite enough of Maduro for the time being.

And we should explore more conventional subjects before once again we inevitably veer off towards the wilder shores of asset markets.

Dario Garcia Giner 10:36

Take us along, captain

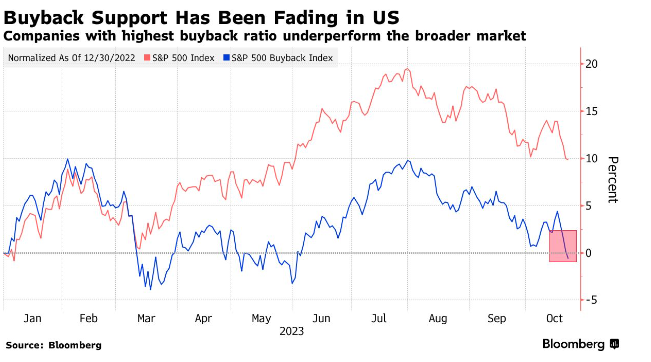

Big week for tech earnings in the US and very fortunately, because they are all priced for perfection, they are not disappointing so far.

Big tech is the most crowded trade. Nearly all of this year’s S&P return of ~10% accrues from the top half-dozen or so names, all of which reporting this week or next.

Where is the new marginal buyer of NVDA MSFT AMZN AAPL? If this cohort cannot provide gains, which constituency can?

(and good morning, Neil, City legend)

One of the main pillars of the mkt support in the US is fading. Buyback momentum is fading for US stocks, though

Buybacks -3% 3Q, -26% 2Q. S&P spent $923mill last year on stock purchases but now the repricing of money and taxes imposed by the Democrats have made them less appealing.

Dollar strength has been one major attraction for the marginal international buyer of US equities, and Emerging Markets, my old stomping ground, have lost out as a consequence.

EM equities have underperformed DM so far this year by around 10%. The dollar looks and feels overbought but periods of geopolitical instability and the continued upward mobility in bond yields are propelling DXY index higher, 106 last.

Emerging Markets tend to struggle when the dollar is strong like it has been this last year.

Why is that?

A stronger dollar tends to impact commodity prices on which many EMs depend, EMs traditionally tended to be heavily indebted in hard currency and a stronger USD tends to discourage foreign capital and investment.

Money invested overseas returns to safer confines of USD.

I was reading JPM’s recently published global equity outlook last night.

Almost always in the past, when USD is strengthening, global equities have been under pressure. Our FX team bullish on the USD next 3-6 months driven by US exceptionalism.. Further, the wide interest rate differential suggests USD could remain well bid. If that comes to pass, equities in general could stay under pressure. A stronger USD typically meant the outperformance of Japan, Switzerland and the UK, in local currency given large export exposures. On the other hand, and again when measuring in local currency, EM and US equities have underperformed. US equities moved to the top in times of USD strength, even with a headwind to the exporters, and Japan stayed the outperformer, in the regional context.

Focusing on EM, mostly tended to come under pressure during episodes of USD strength, both in local and in common FX. EM lagging DM this year by 10%+, and from our equity strategy perspective, we remain cautious on EM. Within this, while there is a risk of further CNY depreciation, we have a short-term more positive stance on China, just as a relative value trade, given an already large underperformance, as well as stimulus coming through, as seen in the latest data. Commodities generally show an inverse correlation to USD direction but we are more constructive this time around, given supply constraints, geopolitics, as well as low inventories. Thematically, we maintain our longstanding preference for FTSE100 over FTSE250, consistent with our preference for exporters.

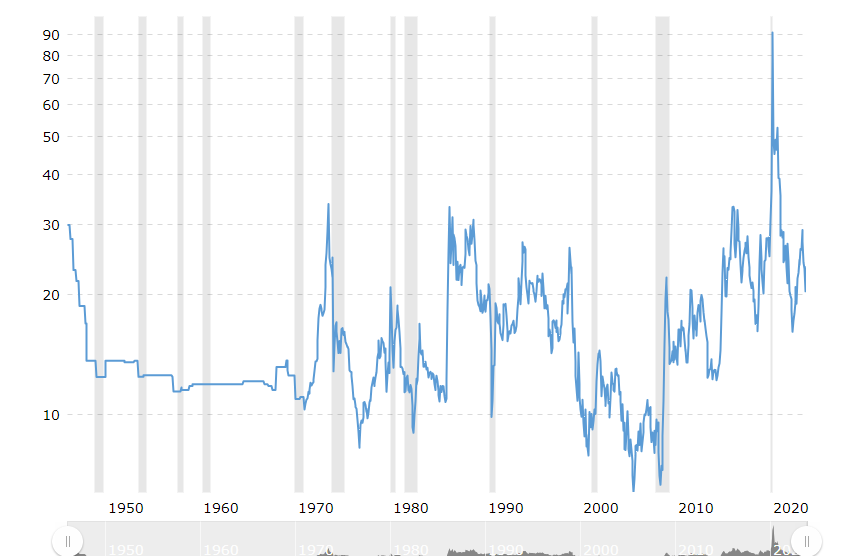

This chart demonstrates what EM investors are up against:

What does that show?

A lot depends on your view of the dollar from here.

Overdone?

I can’t see it weakening when global politics is so miserable.

‘Dollar exceptionalism’

The dollar is where everyone runs when things look bleak – in a crisis the exchange rate is not very relevant to the buyers.

Obviously, the dollar exerts downward pressure on commodities in general but recent events have curtailed that trend. look at uranium, for example, a recent favourite of mine

We’ve discussed uranium of late and it’s still holding at elevated levels, as per this chart below. It’s becoming clear to market participants that this recent spike is the start of something more long-lasting, that future projects for additional capacity are several years off and the price needs to reflect this. Minimum = Inflation + Some is the formula to use.

Geopolitics is the kerosene on fire, especially with recent events in Niger, which is about 4-5% of global production.

Dario Garcia Giner 10:48

And speaking of Niger, we have some quite consequential news this week

The American government has effectively legitimised the military junta in charge of the country, just as the last French troops have been finally, and with great reticence, kicked out

French*

how have they legitimised them?

Dario Garcia Giner 10:50

So they signalled an intention to engage – while accepting it isn’t ‘business as usual’ – they are clear in their intention to continue working with the junta.

Julian Rimmer11:50Does this sound like one of your holiday destinations, Dario?

Dario Garcia Giner 10:50

Unfortunately, a little too unsafe even for me.

Doubt it. I know only one thing about commodities.

The old adage: today’s shortage is tomorrow’s glut.

Dario Garcia Giner 10:51

Now, there’s another player in Niger – wouldn’t you know it – Iran. I wonder why (uraniumuraniumuranium)

Ah, this prompts me for my quote of the day from the Iranians:

Dario Garcia Giner 10:52

The current trajectory of West Africa and the Sahel region has been one of a French exit from the region and an American shift from a die-hard support of pro-Western governments to a more pragmatic and non-aligned position in the continent – a covert admission that the past few decades of Western involvement in the region have been a disastrous mess which opened the door to Chinese and Russian involvement in what was once a solely Western backyard.

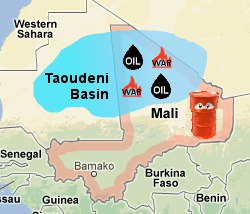

But these have obscured FAR MORE dramatic moves in neighbouring Mali

It’ll be studied as a prime example of disastrous Western meddling.

The French operation Barkhane against Sahelian jihadists was once viewed as a key anti-extremism influence.

But since the rise of the fiercely anti-french Malian junta in 2021, western observers have been going ‘je ne sais pas’ at what in the world the French mucked up so royally.

The Malian President didn’t mince his words at the UN – the French have consistently supported armed terrorist factions in the country.

And he’s not entirely wrong

Why dat?

Dario Garcia Giner 10:54

Well, the entry of France was done with the support of Tuareg rebels in the country’s north and east, which were initially allies with Islamist, pro al-qaeda movements in the region.

France helped legitimise these rebels after they helped drive out the jihadists from Mali with the 2015 Algiers Accords, their way of definitively splitting the Tuaregs from their Islamist allies and aligning them with the Malian government for the foreseeable future.

But it all went tits up since the rise of the Malian junta and the kicking out of French troops.

2023 has seen a brutal revival of the conflict, completely overshadowed by glitzier, media-attracting events in the Middle East and Europe.

is Russia, the congenital malefactors behind all this?

Dario Garcia Giner 10:56

Well, it’s far too easy to blame Russia. I’d call their involvement a red herring.

They’re essentially stepping into a power vacuum left behind by a French military policy that seemed to have become totally oblivious to shifting political grounds in Mali.

And the US ignoring it because it was distracted elsewhere in the ME and Asia?

Dario Garcia Giner 10:57

They certainly were – and it explains perhaps why their policy has recently become much more pragmatic in the region. It’s an admission of being on the back foot.

Now, all the Tuareg militants in the North and East, former French allies, have since allied into a single movement since February – the Coordination of Azawad Movements (or CMA).

The war has kicked off properly since September 2023, with the CMA re-taking arms to violently defend their ancestral lands from incursions from the Wagner-supported Malian army.

Now – none of the sides have admitted to breaking up the 2015 Algiers Accords

But these are now effectively wet paper.

More worryingly still!

And this one’s a kicker…

France’s former allies have now allied with the local al-Qaeda affiliate

The newly rebranded al-Qaeda affiliate, Group de Soutien a L’Islam et aux Musulmans (GSIM).

Nothing wrong with hypocrisy and inconsistency when it comes to the imperatives of realpolitik.

As we discussed yesterday.

Dario Garcia Giner 10:59

Indeed! My only vengeful target is Western journalists who fail to add 2+2

But this is the Blind Spot – so what are the hidden resource conflicts underpinning this war?

Well – many are tempted to say Gold – it’s Mali’s main export after all almost 70%

But most of the gold mines – and gold discoveries – are deep in the country’s south.

One of my very last conference calls when I was a city broker was with an Australian miner operating in Mali.

That was 2 years ago, maybe more.

I must check that share price

Dario Garcia Giner 11:01

Interesting.

The client was not persuaded.

Dario Garcia Giner 11:01

But there is a resource angle to the conflict, which is more concealed

The most critical is the dramatic discoveries of 2015, with potential petroleum reserves on par with Algeria being found in the country’s Taoudeni Basin.

And take a wild guess at where the basin is.

on the beachfront?

Dario Garcia Giner 11:02

Not exactly. Slap bang in the northern region of Mali – precisely an area submerged in hostilities

God is a cosmic sadist.

Dario Garcia Giner 11:02

But the sharp-eyed among you will note this doesn’t explain the full story.

Because ultimately the real epicentre is in the Kidali region of Mali – to the north-east:

And can anyone take a wild guess at what the value of this barren Sahelian terrain is?

Julian Rimmer 11:03Zero

Dario Garcia Giner 11:03

Interestingly enough, the region is the central drug trafficking route for West African produce moving northwards towards European markets.

Neil Collins 11:04

Never mind. The IPA says we won’t need any oil in a decade or two.

Dario Garcia Giner 11:04

Human trafficking routes also

This part of the equation has been below the radar on European policy for a while – but it’s no less central

The EU’s high representative of the Sahel, Angel Losada, gave this one away – “the Sahel is Europe’s new forward border”.

Though the main routes are in the northern regions of Niger, human trafficking from Western Africa towards Europe presumably follows the same routes as the drugs, joining the Sahelian route of Niger after transiting through Mali’s Kidal.

Well, France has always liked shiny things, so its focus on controlling an important European border for smuggling is no surprise.

Speaking of gold, what’s going on with that, Julian?

After its vertiginous 10% rally on the outbreak of hostilities in the ME, gold has struggled to break $2000 resistance.

JPM Morgan estimates there is $130 of geopolitical risk premium baked into the price here and, of course, higher bond yields are discouraging.

The relative hiatus in Gaza has taken some of the heat out of the market but who is buying?

How on earth can they know?

They have an FV based on supply and demand … but if supply/ demand were evenly matched before and now it’s jumped $150, then I think fair to say that’s a risk premium.

Well, some of that squeeze was caused by shorts placed after China imposed import restrictions on gold to protect the RMB but other constituencies are notable too:

I think the Japanese are very important – especially retail investors, who are looking to hedge the declining yen and cope with inflation for the first time in decades while the BoJ’s YCC represses interest rates.

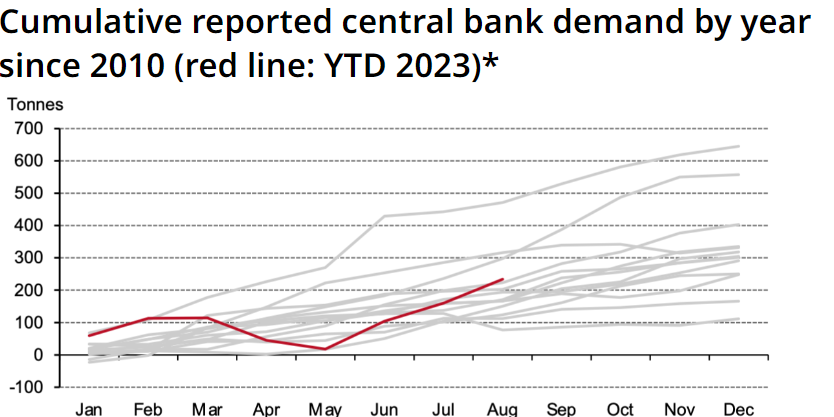

Secondly, and most importantly though it’s the central banks. The most recent month for which we have data from the World Gold Council is August, and that month, CBs bought 77t, their third consecutive increase in holdings.

On the long-term, 50-yr chart, it’s clear to see from a technical point of view how significant a definitive breakthrough $2000 would be.

The next unexpected outbreak of hostilities somewhere, anywhere, might do it.

I’m not a chartist, as it happens, unless it suits my agenda. I rarely had an agenda during my time in the city except the fundamental one of survival.

The chartists = the bendy ruler brigade.

A more astute observer of these things, however, tells me that plans by BRICs to end U$D hegemony and diversify currency trading away from the dollar, are dependent on having something to back that currency with.

And that can only realistically be gold

They may be exploring bitcoin or crypto but for now gold makes the most sense.

China is also well aware, that in the event of a Taiwanese invasion, their holdings in US treasuries would be worthless/ sequestered so they need to build up their holdings of gold.

So, the Chinese are big buyers apparently.

One other driver…

The gold-oil ratio:

Gold is cheap to oil and it reverts to the trend.

Now since it’s topical, the UK is scrapping the cap on bankers’ bonuses…

How do you think the politics of this play out?

It always seemed rather pointless to me to cap the bonuses.

The main impact was to raise the base salaries of the top bankers.

Which increased the risk to the bank, and decreased it for the banker.

The whole point was politics, I assume? Do you agree?

Politics is always a bad motivation. It was just a piece of crowd-pleasing

The cap was to please the crowd.

Dario Garcia Giner 11:19

Why is this coming out now?

It was an EU-wide measure

So it shows that we don’t have to comply any more

So there are still caps in Europe?

As far as I am aware

Astoundingly, since I left the City, I find this issue less emotive than I did.

Dario Garcia Giner 11:20

(Agreed John. Sounds more like back-scratching than electoral politics)

Although for the last decade of my career, it didn’t seem to matter there was a cap on my bonus because they were so low anyway, they had a natural cap.

The case for bonuses is that they can be clawed back if things go wrong later, while base salaries are gone for good.

Dario Garcia Giner 11:21

Isn’t this natural cap on now, once more?

The sector is certainly going through such a difficult time that salaries are falling anyway and the incongruous bonus is more a thing of the past now.

2023 has been a very tough year for investment banks.

Perhaps removing the cap is an attempt to get the sympathy vote for impecunious bankers.

Julian Rimmer12:23No deals, commission rates falling, electronic trading, higher cost of capital, bear mkts etc etc.

Dario Garcia Giner 11:23

Some interesting anecdotal evidence is that almost the entire alumni class of Economics at UCL in 2018 is no longer working at investment banks.

Says a lot about the declining interest from promising graduates in this sector.

the halcyon days are gone for sure.

What are they doing instead?

Dario Garcia Giner 11:24

The only one who was … was working at Credit Suisse

Hedge funds, private equity…

Oh good, really useful activities.

My last interview in the City was with Credit Suisse for a job in Emerging Markets.

It took place at the height of the pandemic, and I wasn’t actually allowed into the building.

So I had to stand outside the fire escape beside all the smokers and be interviewed while standing upright in my overcoat in temperatures just above zero.

I contracted tuberculosis.

But did not get the job.

Dario Garcia Giner 11:26

Well, it’s a good thing you didn’t clearly. Though you missed out on their canteen, which was apparently world-class

If you want to see why the market in new issues is broken, look at CAB Payments

This was one of the largest this year, valued at £851m, offered at £3.35 a share

First red flag: None of the proceeds went to the company

They went to the private equity vendors

The second red flag: enthusiastic endorsement from supporting brokers

Third red flag: price went to 10 per cent discount on day one.

remind us of your golden rule of investing, Neil?

Never buy a share which has not been listed for at least a year

For CAB, a cross-border payments company, it’s been downhill only.

-10% today ~ 55p

A mischievous piece by Bryce Elder at the FT yesterday reproduces all the glowing recommendations from various brokers. They are glowingly positive.

here’s Bryce’s piece:

On Monday CAB endured its own version of a cab crash. The price now is 55p.

A salutary tale to end the session. thank you one and all.

Dario Garcia Giner 11:35

Saludos!

Goodbye!