And that includes you, Izzabella Kaminska with two Zs not one!

10:31 IK: Good morning VIETNAM.

10:31 JR: Wrong country

Waking up to scenes in Dublin this morning. A reactionary mob appears to have burned down half of the capital in response to a five-year-old girl and three others being somewhat brutally stabbed by an Algerian migrant.

Can you be gently stabbed?

Gently = stabbing someone with a crayon

There is a stabbing spectrum

Now I’m an Irish citizen (two fingers up to Brexit, etc.) so I’m especially disappointed

(i.e. I have a five year old)

10:34 JR: Thanks for clarifying that I don’t want Operation Yewtree knocking on my door

But back to the point: Which is to say, one man’s right-wing hooligan mob is another man’s reactionary liberation movement. And it takes two to make peace.

Speaking of oppressive occupying forces with no respect for the rights and cultures of indigenous populations, isn’t today BLACK FRIDAY?

So-called because it is the day everyone receives reparations for past wrongs and dispossessions via the mode of MASS RETAIL DISCOUNTING. Aren’t we lucky.

It was heartwarming to see the former POTUS’ Thanksgiving message last night, sent at 2.03am!

10:36 IK: What a sweet message filled with warmth and love.

DXY 103, 4% off highs

The only other thanksgiving message half so feelgoody was that from Rudy Giuliani

With the best zoom backdrop you’ll ever see

At some point around 50, he decided wearing a bowtie was a good idea.

His hair dye must surely melt

10:38 IK: Can we talk about markets now?

In the former category we find Javier Milei, a poor man’s Elvis

Because Argentinian assets haven’t done badly since his election victory

That’s the Merval and in $ terms too so all the more impressive

Is Milei tacking to the centre ground after hogging the right touchline all the way through the campaign?

10:40 IK: Well there you go. Markets like crazy libertarians who want to dollarise their economies. Who could have predicted?

By Matt Lynn

Which hinges on the line ‘If that continues, there is just a chance that Milei’s plan might work’.

Stating the bleeding obvious

If nan had wheels she’d be a wheelbarrow.

The currency also faring well

Milei had referred to his peso as excrement before the elections

He had also called the Chinese ‘assassins’ (fair cop, guv), insulted the Pope (nothing wrong with that), referred to Brazilians as communists (nothing wrong with that either, come to think of it) but is now being more diplomatic.

And inviting everyone to Dec 10th coronation, please God someone give him a short back and sides beforehand and basically acting like a politician.

Worryingly, though, Fat Donny has accepted the invitation too and will be jetting down to Buenos Aires in hair Force One.

Cant wait to see that photo

Argentina banks are very nervous and switching exposure to short-term notes.

10:43 IK: How short?

Tough call to be an Argie bank when the president has promised the abolition of the central bank.

I mean, banks without central banks are just crypto companies.

Quids in.

Milei will be heavily dependent on his predecessor-but-one Macri for support in congress and mkts generally had a constructive approach to Macri.

Hence the reaction of mkts toward Arg assets this week. There’s also the realisation most of the nutty stuff wont make it through congress.

Macri may push him to pursue the Mercosur trading bloc deal with the EU.

The law of averages , though, like with premiership football managers, is against him.

All careers end in failure (mine in the City started that way, ended that way and had a slump in the middle),

(except JFK who will be forever preserved in the aspic of perfection -(dying was a ‘good career move’ pace Gore Vidal) before he had to accept defeat in Vietnam and deal with America’s economic decline

So do give us some feedback

10:47 JR: Speak for yourself – I’m sticking to the script

10:47 JR: Euroclearing

10:47 IK: The world’s least thrilling subject, but actually super important.

10:47 JR: I disagree

You make it exciting

10:48 JR: What’s the scoop?

(sitting up on the edge of my seat)

10:48 JR: Bastards

Post Brexit this is no good. Europe wants to bring back euroclearing onshore.

10:49 IK: I think they’re called the euromoney awards

10:49 JR: More prosaic

How are they planning to pull that dread feat off?

10:50 JR: Sounds a bit repressive

10:50 IK: It sure is. It’s not dissimilar to the US trying to prevent its citizens from using foreign-based gambling platforms, which they do anyway by using VPNs. But actually it’s worse, because at least the principle behind the US gambling bans is that it’s banned everywhere. This is more like forcing U.S. citizens to only use U.S. platforms for their gambling, which some might say is a breach of WTO.

In fact there was a famous case which did exactly that

I’m not sure if the Europeans have considered the WTO implications. But hey.

In any case, here’s how our Politico’s FS newsletter broke down the latest demands from the EU:

PUSHING FOR A EURO CLEARING DEAL: Europe’s banks and investors with the biggest euro derivative portfolios must clear at least five trades a month on EU soil under draft measures that are up for debate in Council this morning.

The Spanish EU presidency circulated a draft on Wednesday, obtained by Morning FS, in the hopes of winning enough support from government officials.

It’s unclear at this point whether everyone will swallow the deal, which has been largely tailored to suit the views of France and Germany. An accord would, however, ease the pressure on the Council to move a post-Brexit initiative that the European Commission sees as vital to safeguarding Europe’s financial sovereignty.

SO WHAT? If accepted, Brussels will be one step closer to wrestling euro clearing out of the City of London’s hands to ensure the EU isn’t completely reliant on the U.K. for a market that’s worth trillions of dollars.

The City is home to some of the world’s largest clearinghouses — institutions that act as a middleman between companies that agree derivative contracts, a form of insurance against financial risk, such as interest rates.

The Spanish draft suggests a two-step process to force euro clearing south of the Channel. First, all European companies in the market would have to set up a basic EU account that does some clearing through the year but can be ramped up to do a lot at any point. The second step is about setting trading thresholds.

And here’s where it gets increasingly mafia-esque absurd:

The text states that companies with a derivative portfolio worth more than €100 billion must carry out five different trades a month through a European clearinghouse. The EU’s securities regulator would decide what these trades actually entail.

Companies with a portfolio worth less than €100 billion would only have to carry out a maximum of five trades over a period of six months. A trader that handles under €6 billion in derivates would be exempt from these specific demands.

Madrid is hoping there’ll be minimal pushback today so that EU ambassadors can rubber-stamp the deal and begin legislative negotiations with the European Parliament to deliver a final piece of law. But there’s a risk that smaller countries will protest a process that’s catered too much to the demands coming from Paris and Berlin.

THE BOTTOM LINE: Madrid is trying to hurry a hugely consequential and contentious bill through Council before year-end. The question is whether it’s won enough countries over to avoid further delays.

Clearly, anyone who actually believes in globalised and open markets should consider this nuts. It’s one thing to prohibit U.K. financial firms from servicing European clients without established European subsidiaries. It’s another thing entirely stopping the de facto flow of capital abroad and your own citizens from choosing how and where to spend their money.

10:53 IK: Which is why I equate this to a type of soft capital control return. One that’s only going to go badly for the Europeans. It’s like the UK deciding that the only way it can rescue LSE listings is by legislating that companies MUST by law list in the UK, as opposed to actually competing in international markets by making conditions more desirable domestically and wooing companies on merit.

What do you think Jules?

10:54 IK: Funnily enough, I’m glad you mentioned that.

10:54 JR: (doesn’t happen often to me)

10:55 IK: This all also ties into the fact that the ECB is also currently considering upping the minimum (unremunerated) reserve requirement.

If it goes ahead with that, financial conditions in the eurozone will get even more onerous with likely flighty consequences for capital. The risk here is that eurofirms will abandon onshore euro deposits altogether, and put their money in U.K. domiciled euro-tracking stablecoins, which will then fund all their business and clearing activity.

Like when regulation Q in the U.S. inadvertently sparked the makings of the offshore eurodollar markets.

Except this time it will be euro-denominated offshore markets that flourish, which the EU will only be able to direct and control via FX or FX swap interventions.

10:57 IK: For sure, but the only way they can realistically do so is with overt capital controls on the flow of euros. And do they really want to become the new China?

10:57 JR: I cant see them going that way

10:57 IK: At the moment, no-one has really squared this with de facto European capital controls. But it’s moving slowly in that direction. Just to spite BRITAIN.

@colin – i guess you’re referring to the pension reforms?

I haven’t looked at this too closely, but i did do a quick google the other day, because as we discussed here last week, Andrew Griffith (no longer Economic Secretary to the Treasury) had told me that the reason pension reform had not made it into the King’s speech is because they didn’t have to legislate for it.

He said there would be more info at the Autumn statement, and yet… not so much.

What exactly is going on?

What we did have was this instead:

11:00Chancellor to offer workers ‘pot for life’ in pension reforms – FTAdviser

11:00Chancellor to offer workers ‘pot for life’ in pension reforms – FTAdviser

11:00 JR: For smoking?

11:00 IK: We’re getting pot for life

Yeah yeah. Funny.

But yes, not exactly the sweeping reform we were expecting

11:01 IK:

In the Autumn Statement today (November 21), Hunt said: “I will consult on giving savers a legal right to require a new employer to pay contributions into their existing pot.

“This would give savers one pot for life.”

Currently, employers are required to enrol eligible new staff into a retirement scheme, chosen by the company.

This has led to employees ending up with multiple small pension pots as they move jobs and switch to their new employer’s scheme.

However, today, Hunt announced that workers will be given the right to nominate the pension scheme that their employer pays contributions to.a

11:02 So, if you’re anything like me, and you have about a dozen pension accounts from legacy employers (okay I have two), and you don’t have the bandwidth to bundle them together and wouldn’t know how to start, this is the initiative for you.

As per other European countries, you just have one pot

It is a good idea.

11:03 IK: But, this is just a fraction of the stuff that was supposed to be coming. Radio silence on all the other stuff, unless I’ve missed it somehow. But i confess I did not read the budget from beginning to an end.

11:03 JR: I did and I don’t recall seeing very much. certainly nothing that sticks

11:03 IK: Let’s have a quick look

BTW – did you know, you can order your own copy of the Autumn Statement?

Find out how to buy print copies of official documents (command, House of Commons and un-numbered act papers) and how to be listed as a supplier of print copies.

@johnk – 100% agree but makes for bad politics. gives Labour a free swing on that subject

Looking after millionaires etc., etc.

It would galvanise UK equity mkt very quickly

To ensure that the UK’s world-leading financial system invests the

capital companies need to grow, the government is bringing forward a

comprehensive package of pension reform and driving private investment

from insurers into infrastructure by legislating for key reforms to

Solvency II.

There was also this:

Pension reforms, as described below, have the potential to make more pension

scheme funding available to finance business investment. This could result in an

additional £75 billion of financing for unlisted equity investment. Some of this

would flow overseas or to secondary investments. But this additional finance

could also address the current mismatch between the supply and demand

for equity finance by smaller firms in the UK (an “equity gap”), thereby raising

business investment.9 The insurance industry may similarly increase investment

in productive assets due to reform to Solvency II.10 Taken together, these reforms

could support an increase in business investment of around £2 billion per year

in the long run.

11:07 JR: I can see why he didn’t say this during his speech

11:09 JR: From one economic powerhouse to another

Ahem

German 3Q GDP this morning -0.1% qoq, -0.8% yoy in line with estimates

Drop in household spending held accountable.

Whatever happened to Europe’s manufacturing dynamo?

The absence of cheap Russian natural gas/ energy is clearly one major reason for this, higher rates took a toll (but they did everywhere)

But China’s slowdown, glacial re-emergence from its pandemic, was the biggest contributor, especially since it’s Germany’s largest export market.

OECD reckons Germany 2nd worst performer in OECD, only ahead of Argentina. Last week Germany’s top court rejected an attempt by the govt to repurpose €60 billion ($65.6 billion) of pandemic aid to finance climate protection, ruling that it contravened the constitution.

11:11 IK: surprising about Argentina

11:12 IK: [HOLD THAT THOUGHT FOR JUST ONE SEC: The FT seems to have had the scoop on the Pension story just before the Autumn statement.]

https://www.ft.com/content/51dd6da0-7a92-449e-8414-24182a2257ad

Seems the UK govt was getting a lot of pushback, because guess what, illiquid investing would up costs. Who could have possibly predicted! Via the FT:

A UK government push to unlock £50bn in capital from the country’s biggest pension funds is running into roadblocks as retirement funds balk at shifting savers’ investments into costlier and riskier assets. Pension funds have been seeking to align with the UK’s ambition to fuel economic growth through pension fund finance dubbed the “Mansion House” reforms announced in July. The voluntary “Mansion House” compact signed by nine pension funds, with about £400bn in combined assets, aims to invest at least 5 per cent of members’ “default” funds into unlisted assets, such as private equity, or early-stage companies by 2030.

But some signatories said they had encountered challenges as they seek to implement the agreement that requires investment in higher-cost assets. Aviva, one of the UK’s largest pension providers, said one important issue was the question of how to introduce unlisted, also known as “illiquid” assets — which are typically more expensive than public assets — to existing “default” funds used by millions of savers.

But back to Germany…

The world needs productivity innovation to generate the growth to extricate it from current crisis

Because otherwise we all have five years ahead of almost zero growth

‘The bottom line is that the fiscal position of too many countries is not well positioned for the end of the “low for long” regime for global interest rates.

This results in a further loss of policy flexibility at a time when monetary policy is also constrained.

Indeed, as illustrated by the net impact of yesterday’s UK fiscal announcements, governments can easily end up in the muddled middle when pursuing their higher growth, lower inflation and debt containment objectives.

Most importantly, it highlights the need to do a lot more to promote productivity gains and durable inclusive growth that respects our planet.’

11:15 Before Izzy engages with the rabble, descends into the crowd to kiss babies and shahands etc

A quick look at South Arica

Africa

Most of my career was wasted I mean spent in Emerging Markets, primarily an asset class I called RATS. I was hoping RATS would do for me what BRICS did for Jim O Neill

11:16 JR: Erm, no

Did much better out of bricks than i did from rats

11:17 IK: What the hell was rats?

RATS, of course, stood for Russia and Turkey South Africa, which obviously didn’t quite work.

11:17 IK: Haha

If one wanted to discuss these markets with an investor one was obliged to ring the leper’s bell before doing so.

Declining currencies meant by the end of my time as a broker one had to write twice as much business to earn the same commission as a decade earlier.

Russia and Turkey were often at war and on one occasion in 2016, I think, with each other.

this is an unfavourable backdrop for broking an equity market and lord knows I was a broker who really needed a bull market

I look back on my career as one unfulfilled potential but perhaps I’m being too hard on myself; it was just the markets in which I specialised.

SA was generally slightly better in that it had periods of relative rationality and many of its companies had world-class managers

But, like the other two, most of the potential remained unlocked simply owing to extremely dysfunctional government and political systems.

The dysfunctional govt remains even if on a corporate level many SA companies have world-class mgmt. However, next year, the forecast decline in global inflation and bond yields may give SA an outsized return relative to many developed markets and an opportunity for investors struggling to find some performance

A note from Investec this week posited that a 50bp reduction in SA govt bond yields could provide a 15% total return next year and equities could deliver 20%.

12m fwd PE is 11x, a tad below MSCI EM and a div yield of 4.5% isn’t to be sniffed at. If DXY has peaked for the time being, ZAR is one of the high-yielding currencies that usually benefits, esp in period of cmdty px strength

This chart shows ZAR tends to appreciate by 5% 12mths from the peak of FF

Part of the investment case rests on China’s economy bottoming out, giving cmdty prices support

Scope for a 10% rerating in SA equities.

And the sectors to be in according to this

Are chemical, banks, retail and property. Constraints on SA remain energy and transport inefficiencies.

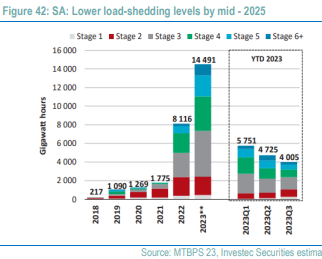

Loadshedding is declining but the train network operates poorly and SA’s two main ports, container terminals at Durban and Ngqura were ranked 365 and 361 respectively out of 370 ports worldwide by the World Bank in 2022.

The wild card remains elections next year. ANC will remain in power aough their share of the vote is seen as crucial. Ramaphosa needs to win >50% to avoid having to enter into compromising coalitions with minority parties. The ANC is a clown car on fire but they seem positively statesmanlike compared to the alternatives on offer.

11:24 IK: Any other requests from the rabble in the last 5 min?

11:24 IK: Otherwise I wanted to point out there’s some Nvidia news.

Delay in its China chips

11:25 JR: You think this may explain the stock’s underwhelming response to the good numbers this week?

Also, worth highlighting the chaos in oil markets.

The OPEC meeting was unexpectedly delayed, because of some conflict with Nigeria, and now apparently it will only be happening online.

I know everyone thinks, especially after the autumn statement, Britain is a rubbish country

But did you know, Izzy, we are the world litter-picking champions?

Yes, we may be a country in irreversible decline, however

11:28Britain wins the world cup — for litter-picking

11:28Britain wins the world cup — for litter-picking

Whereas I reckon I can only talk or write half of that

There’s a reason to fly the union jack

I’ve just a quick look at the data on

letsrecycle.com

11:29 IK: And we are, at least in the paper trash world, back in positive territory. So I guess someone wants our rubbish.

11:30 JR: @colinc

You’re right

11:30 IK: Right on that note, it’s goodbye from me.

Nunc tempus taciendi

Adios