")

Good morning, aloha and greetings fellow market wizards

Apologies for airwave silence yesterday but technological problems and a race against time defeated us.

Nonetheless, here we are this morning, postively brimming with vim and information

And greetings, Dario

Greetings Julian, hello rabble!

I’m in the News Building in an unfamiliar environment this morning, hence, a slight sense of disorientation. I presume you are on the beach in Marbella, lying in hammock, sipping a piña colada?

Well, I’m not exactly at the beach, but anywhere is better than the horrible wind funnel created by the News/Shard buildings

Terrible place to be an addicted smoker

Yes, some miserable people standing outside pulling on a crafty fag and shivering while the security people outside are wearing the big Russian furry shapha hats

shapka*

AI was not responsible for the downtime yesterday but it is responsible for everything else, including a monopoly on business newsflow

But some things never change

“Hey, I’m Jim Cramer, welcome to Mad Money, welcome to Cramerica, some people want to make friends. I just want to make you money.’

You may prefer that intro?

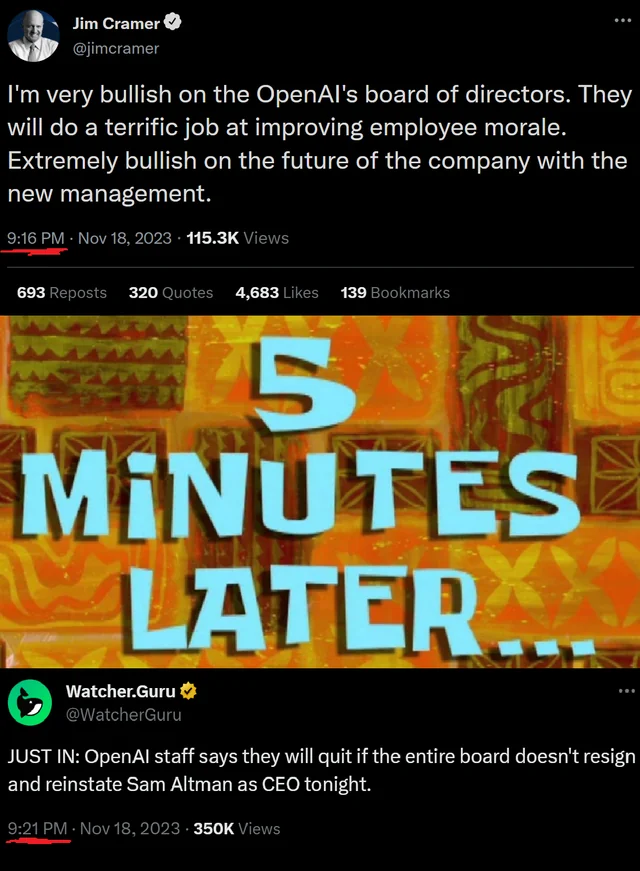

Since Emmett Shear has been appointed Replacement CEO, we’re all still in the dark as to why Altman was fired

The official announcement was he was let go ’cause he lied to the board – though we’ve had no details about those allegations

Another possibility is that Altman’s aggressive push to keep openAI ahead of the AI arms race sparked suspicion from an influential group at OpenAI under its Chief Scientist and co-Founder, Ilya Sutskever

Who has claimed in the past his preference to tread very carefully due to the threat posed by sentient AI

But since yesterday, we’ve seen Ilya has signed the famous letter to the OpenAI Board, which asked them to quit.

So it’s unclear what side Ilya is on. Or generally, what the heck is going on

Did a robot send the dismissal email?

Maybe ChatGPT did

I never doubted it

We will have more news for you tomorrow regarding rumours we’ve received concerning suspicions about Altman’s loyalties, which were running amok in the American national security circus

I don’t know if you saw but the Word of the Year according to the Cambridge English dictionary is ‘hallucinate’, but a new sense of the word to describe how ChatGPT goes rogue or if it has the wrong inputs writes inappropriate stuff.

Could this be an example of hallucination?

Interesting new sense to the word

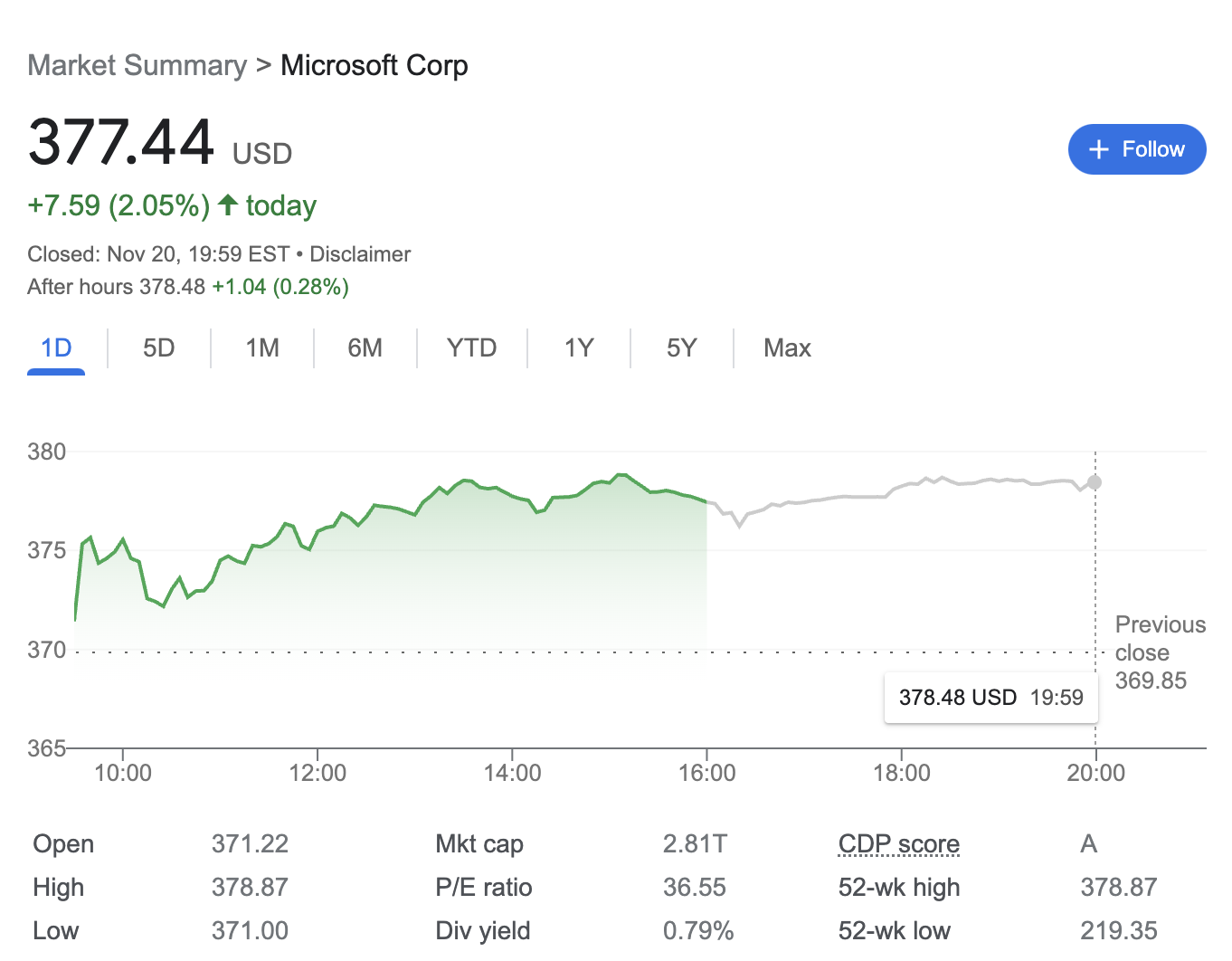

The firing caused a crash at MSFT stock, at least for a little bit

But now the tech giant seems back on the road again after hiring Altman

Now, their stock is at an all-time high.

If they keep it up, I can see them becoming the next Microsoft.

There’s an excellent thread on why the kerfuffle is so bullish for Microsoft, which is too long to post here, by Reed albergotti

Now, I think the news is obvious AI-bullish

If the comments stating that Altman had been fired due to his overzealous attitude towards the development of AGI are correct, it means the entire conflict is about the OpenAI Board’s worry that AGI will become too big to handle.

But others think differnetly

Writing on the offering of AI investment deals, newscaster and hedge fund manager David Dorr claimed he “wouldn’t touch any of them at any price” because of AI-led disruption’s velocity

“The billion $ AI business of today will be replicated and improved by another AI for $20 tomorrow. No business is immune especially one built on AI. What’s Microsoft’s investment in OpenAI worth in 90 days as free copies of itself are being spawned out in the wild with zero guardrails and full internet access?

I would suggest that not only is their investment blown but that their liability is very cheap. Personal view not investment advice – puts on MSFT look cheap.”

Remember gents – we’re in a hype cycle!

UBS wrote in their weekly equity outlook

Our view: The media attention is unsurprising, given the central role of unlisted OpenAI in bringing generative AI to the mainstream. But regardless of how it shakes out, and without taking any single name views, we think the structural growth story for AI beneficiaries remains intact. We forecast global AI demand will grow from USD 28bn in 2022 to USD 300bn in 2027— a 61% compound annual growth rate, a view which factors into our recent upgrade of US information technology to most preferred. Within tech, we anticipate the large getting larger in this late-stage of the cycle, and suggest investors diversify exposure across industry leaders to avoid single-name risk. Investors with a long-term lens can position in leaders from disruption, from AI to the energy transition and healthcare.

However, from a stock market perspective the AI theme is unlikely to alter the emphasis on the Magnificent 7 going into year-end because PMs and retail traders will stick with their winners and people who have avoided all year will be nervous about showing no weightings in these names at year-end if they’ve underperformed

Another CEO set to leave? Linda Yaccarino of X? After the anti-Semitic tweet highlighted here last Weds led to a wave of withdrawals from Twitter’s (X’s) biggest advertisers. Interesting to see one of the ways they intend to plug the gap is

I think calling that tweet antisemitic is reaching – if so, we should revisit all sorts of content online for anti-Islamic, anti-white hatred which is just as bad (or just as banal) depending on your POV

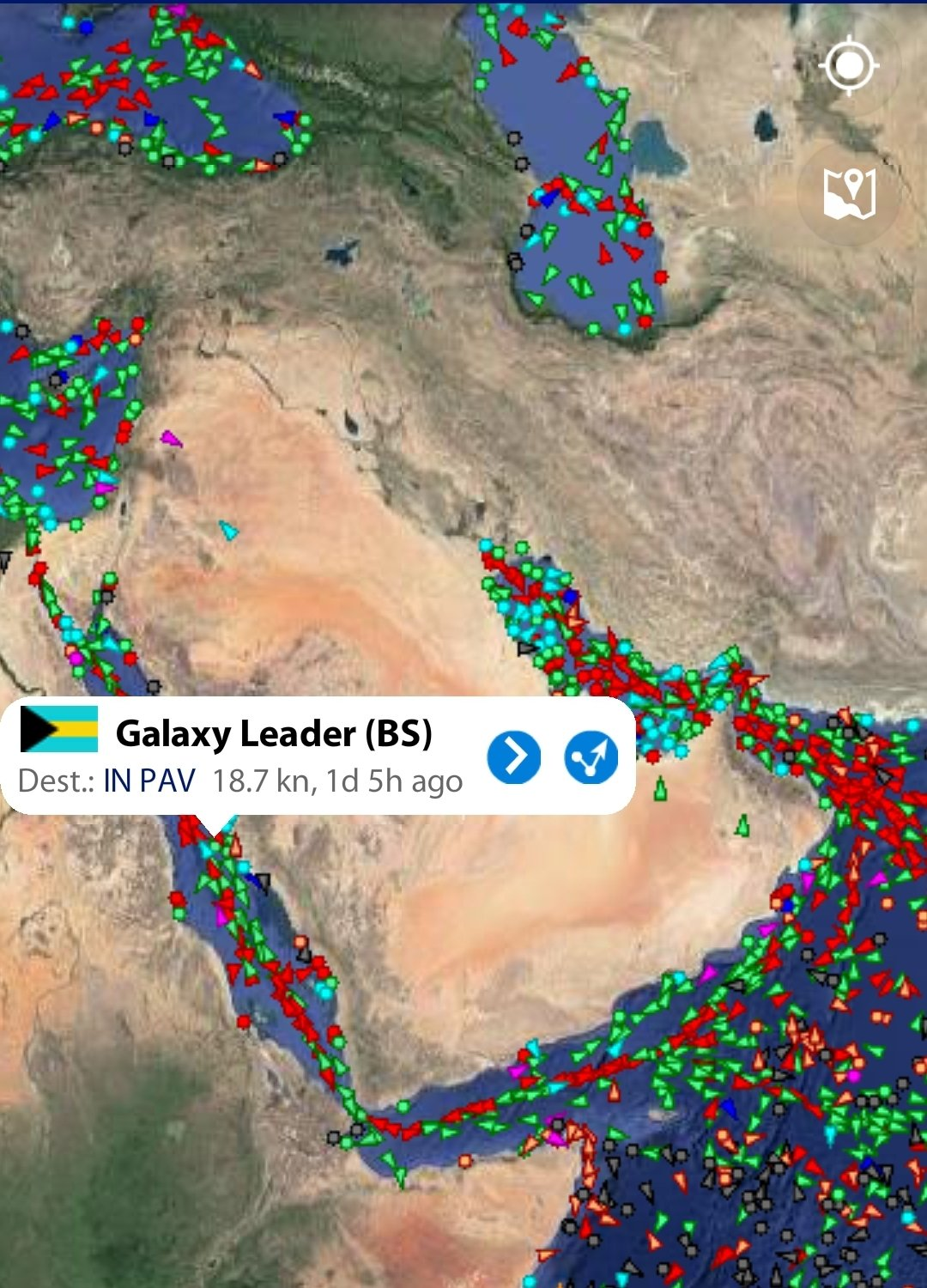

But speaking of reaching and Jewish people – the Yemenis reached the Galaxy Leader ship this weekend

Amazing segue

Israel refuted the ship had any relation to the state of Israel – it’s a Bahamian-flagged shipper, operated by Japan’s NYK Group, and has an international crew of 22 mariners on voyage to Turkey from India

But the tie is that the ship is owned by Isle of Man company Ray Car Carriers owned by one of Israel’s richest men

It’s also not the first of Rami Ungar’s boats to have been hijacked from Yemen

The consequences of this move are obvious:

Look at the amount of shipping in the region. No amount of policing will ever be able to adequately protect all those ships

This has led the International Maritime Security Construct and the Coalition Task Force Sentinel releasing a joint letter regarding the increased threat level to shipping in the Red Sea near Yemen.

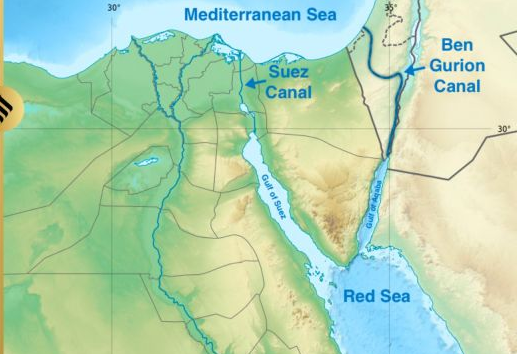

It also calls into question our discussion on the Ben Gurion canal

And on whether this would only serve to increase vulnerabilities of intl shipping to the vagaries of Houthi militiamen by tying their shipping and commercial trade routes through the Israeli state

Following on from Israel, we posed the question last month about the motivations for Hamas’ Oct 7th attack: cui bono?

and made the supposition at the time that Russia stood to benefit the most

Look how this played out

According to a report by the GDELT Analysis Service, about 8% of all daily news on CNN was devoted to Ukraine.

After the outbreak of the war between Hamas and Israel, the number dropped to less than 1%. CNN writes about this after analysing the data of media analysts.

Speaking of unlikely figures – why don’t we have a little chat about Milei

Dont cry for Milei Argentina

You know it’s bad when the only foreign leader who endorses your election victory is Donald Tramp

He congratulated the libertarian outsider. “I am very proud of you. You will turn your Country around and truly Make Argentina Great Again!” Possibly the most inauspicious start to a presidency a libertarian outsider could hope to have, an endorsement coming as it does from the five-times bankrupted, thrice-married, five-times indicted, twice-impeached Mar-a-Lago Ripper.

As my father said yday morning ‘this was a choice between Guatemala and Guatepeor” (between guatebad or guateworse)

Spanish paronomasia

Or to quote an argy friend of ours; ‘an exciting choice between being drowned or burned alive”

The promises for radical economic and financial changes etc etc but mostly about ‘owning the libs’, Milei’s victory shows how desperate Argentines were for putting behind them extremely high inflation, sputtering growth and endless economic crises.

Hope to realisation, however, will be challenging for Milei given the economy he inherits, the country’s fragile finances, and his policy proposals and the fact that the establishment and the civil service will be working and conspiring against him

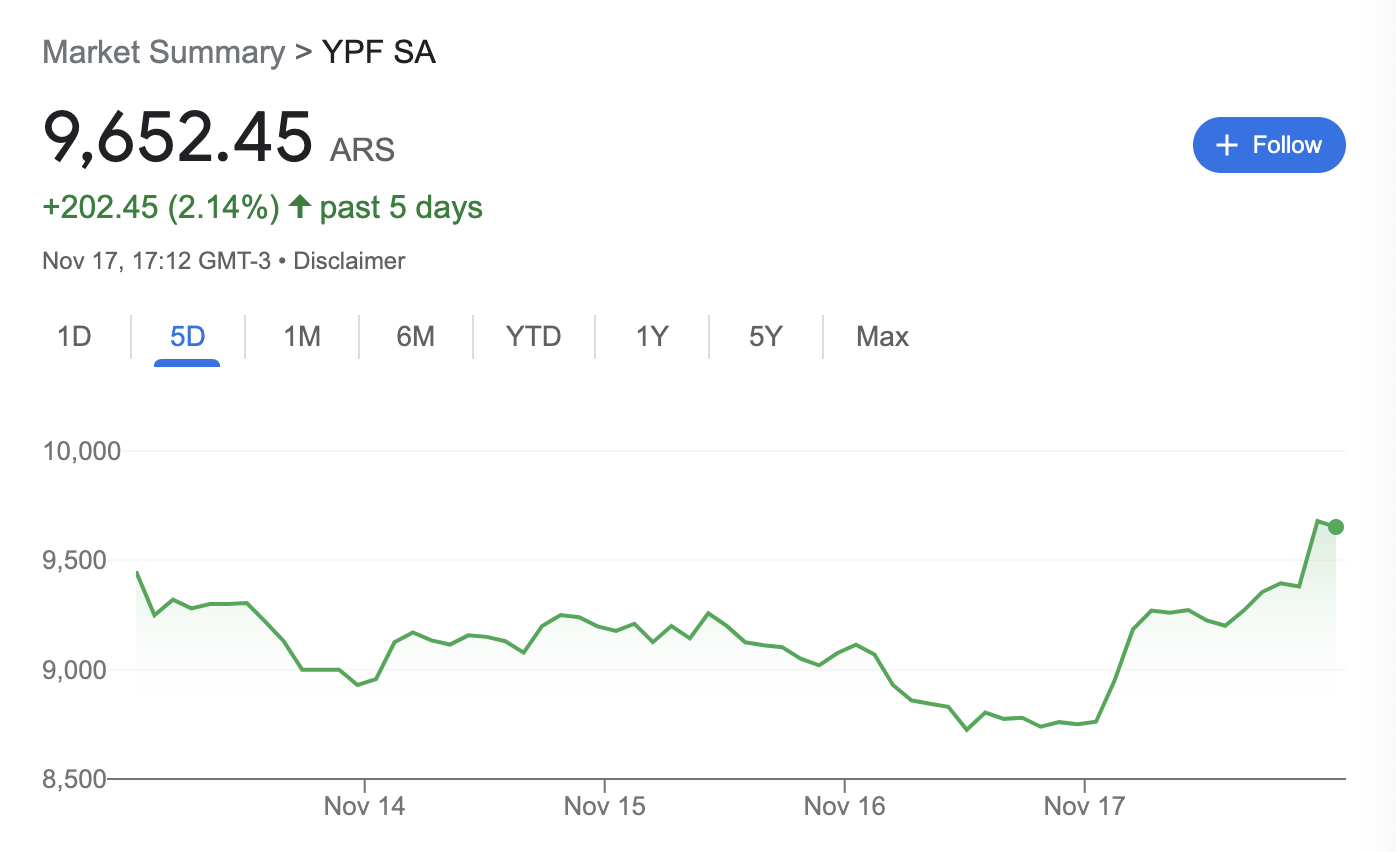

One stock worth looking at however is Argentine-state-owned oil manufacturer YPF SA

and it’s been growing what seems like an absurd amount recently

JR; can you explain for an economic noob like me?

Well, if it exports anything and earns hard currency, that would explain it but I don’t know the company, but also, I suppose, perceived reduction in corruption, improvements in efficiency and cost mgmt, accountability, more professional management?

Milei said he was interested in privatising YPF!

Milei also showed an interest in selling off ownership of the Vaca Muerta shale reservoir – which means Dead Cow

All 30,000 square km of it

Though 12 companies are operating there, Chevron being the first investor and YPF are the primary exploiters of the reservoir

They would be my first bet on buyers of the reservoir

We were once sued by a neighbour of our house in Turkey who allowed his cow to graze without our permission on our field and the cow promptly keeled over and died

That’s my dead cow story

That’s hilarious

I have a story for most farm animals

The goat is my best

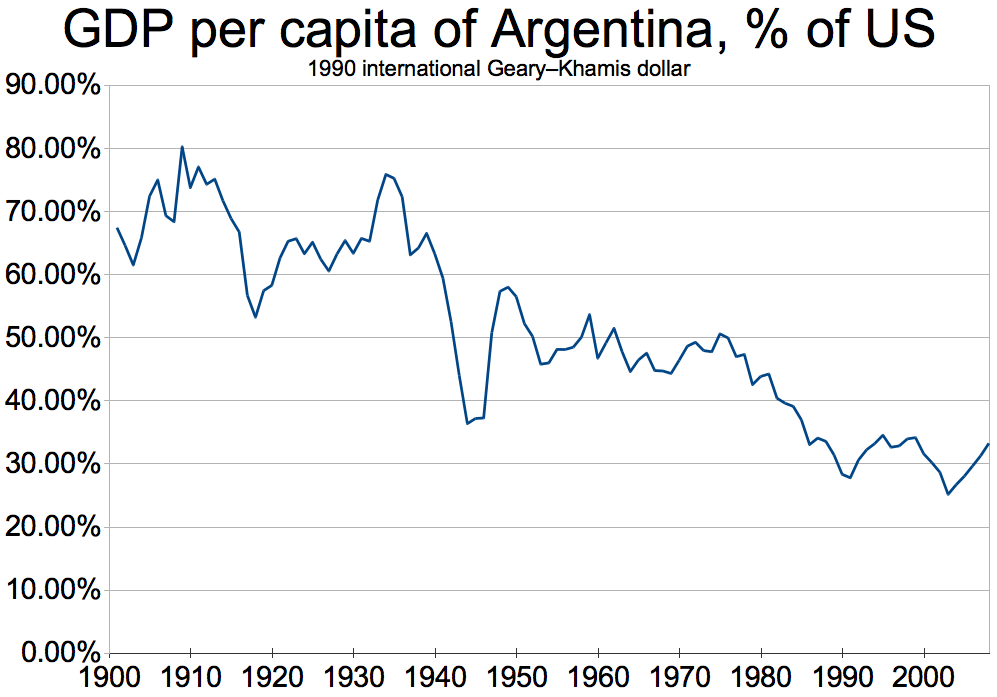

I sat pondering the unlikely trajectory of Argentina this morning. I can’t think of another country which has deteriorated more (aside from Lebanon): it has a higher GDP per capita than Europe in the mid-1930s and look at it now.

And the internet’s been awash with memes:

That meme is incomprehensible to this boomer

Aurora’s view:

Milei will assume the presidency on 10 December with a significantly stronger popular mandate than any non-incumbent president in living memory, potentially straining key alliances he will still need to legislate and govern. 3. In the short term we expect Milei’s victory to be better received by bondholders than by currency markets. 4. Further out we expect Argentine assets to stage a gradual recovery over the next quarter, but doubt Milei will ultimately prove any more successful than his predecessors in solving Argentina’s longstanding economic policy problems.

A bit of market miscellany now

Earnings from Nvidia (+45% ytd) are scheduled for later today. The stock is up almost 50% ytd and the whisper number above (e)

And tomorrow we have the most important of autumn statements from Jeremy Hunt, the Chancellor

He was scheduled to receive economic forecasts from the OBR before finalising his speech which is expected to include tax cuts for business and welfare reform

The most eyecatching reform would be a change in IHT

Red meat for Tory voters but actually, in the grand scheme of things, numerically irrelevant because the last year for which records are available – ie 2021

Only 27,000 estates were liable for IHT

Nonetheless, at this juncture the Tories need to thrown a Hail Mary

As they’re 20 points down in the polls

Hunt’s hands are tied, though because the mkt will take a very dim view of any unfunded tax cuts anywhere else so perhaps NI is reduced slightly but really, there’s so little he can do at this juncture

Waiting till April for tax cuts may be too late, especially after a damaging week like last, showcased by the Braverman sacking. Promising a tax cut soon, a tactic the Tories have tried in the past, may not be enough at this stage.

Other policies Hunt is due to announce Wednesday include

- Extending the so-called “full expensing” tax break for businesses, which gives firms 100% tax relief on capital spending to encourage investment and was due to expire in 2026

A plan to speed up connections to Britain’s electricity grid and compensate people for having grid infrastructure built near their homes

- Extending support to hospitality firms and small businesses through business rates relief, but imposing higher tax bills on larger retailers and supermarkets

- £4.5 billion of funding for eight manufacturing sectors including cars and green industries

Key issues will be :

Do triple lock pensions go up in line 2.5% w CPI or with wages?

And b) do benefits go up in line with September CPI (6.7%) (as they are supposed to) or Oct CPI 4.7% which makes a huge difference to one’s monthly payment

That’s a big difference and expect Labour to notice it if Hunt pulls a fast one

Govt has floated its limited range of tax cuts and observed that neither cable (up from 1.21 to 1.25 on the month) nor 10yr gilts (down from 4.6% to 4.12% mtd) reacted badly at all. Both rallied in fact. So long as Hunt does nothing to increase borrowing, things are ok from an economic standpoint, if not an electoral one. But gdp growth 23/24 only likely to be 0.5% and 25/26 no better than 1%. Hard to win elections on that performance

Now, while there’s not that much Hunt will be able to offer by way of substantive tax cuts due to the tiny fiscal headroom – Britain and Europe more widely may need just such a push

Flash PMI readings will be published over this week, widely expected to show Eurozone and UK readings in deep contraction, with services slipping more modestly, and performing fractionally better or unchanged since Oct

Contrariwise, US and Japanese manufacturing expected to flatline

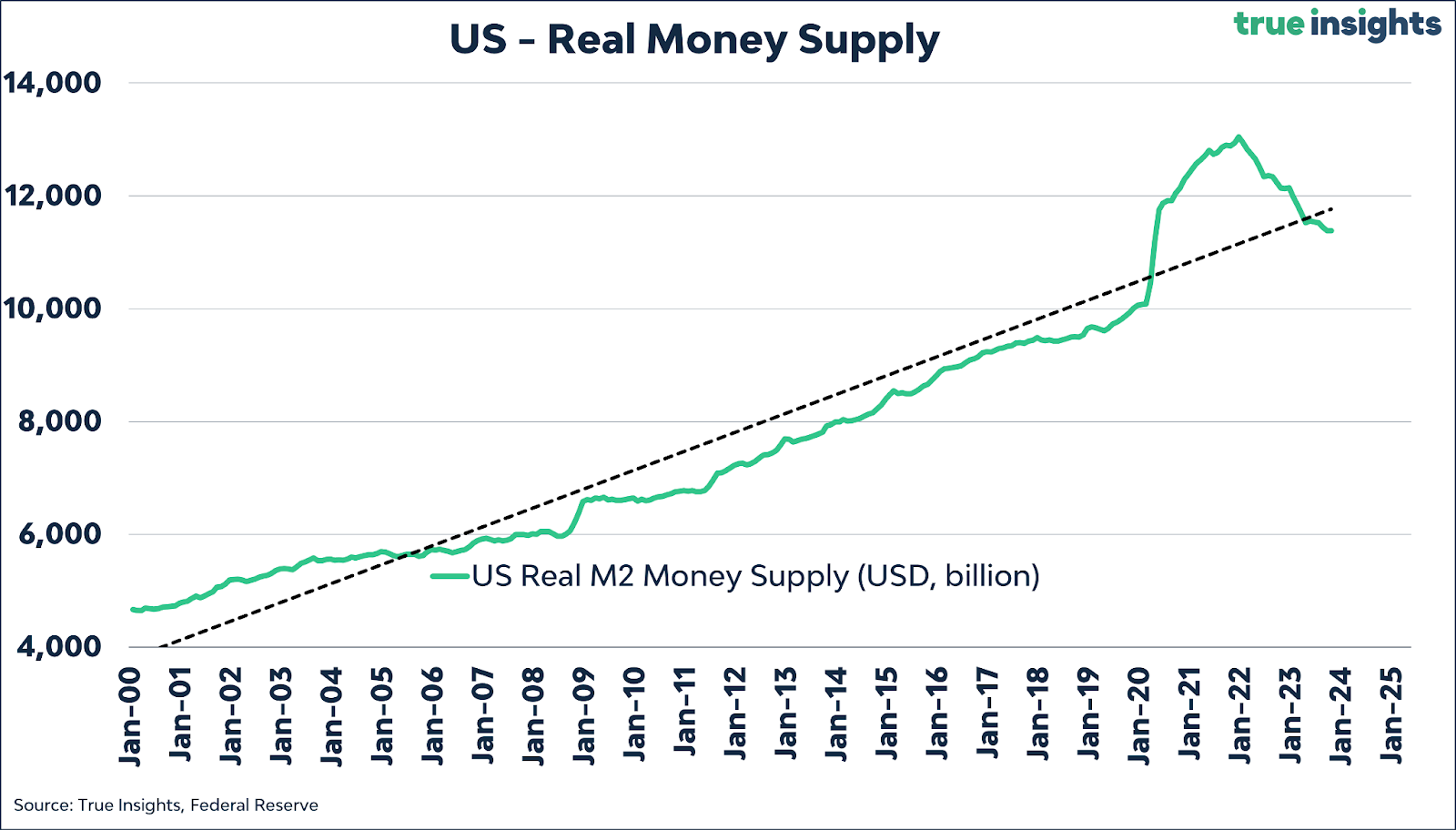

UST10YR yields now 4.4%. The fall in M2 is what’s driving inflation lower as demonstrated by this chart from Jeroen Blokland.

Last night the UST20YR auction went off well @ 4.78%

And there was plenty of demand so the mkyt is still comfortable with the trajectory of rates. the mkt things a 28% chance of a cut as early as March 24

In other forecasts, Marc Ostwald had the following to say;

“US Durable Goods are forecast to decline 3.2% m/m on the back of aircraft orders (reversing the aircraft orders led surge in September), but continue to post modest core Orders gains, while Existing Home Sales are seen declining a further 1.5% m/m, with low inventories still as much to blame as high mortgage rates.”

The S&P is now + 7.5% for Nov so roughly one third of this year’s entire index gain came last week

XAU broke $2000. It has done well this year despite DXY strength, mostly fuelled by central bank buying, and now falling UST yields are softening the dollar, gold is breaking resistance.

Little thing on Bitcoin, which is still also doing well these past few days

Still waiting on that ETF

I’m compulsively checking my Revolut app for the promised day my ‘investment’ in bitcoin goes green (it never will)

DXY dropped from 107 high to 103 which reflects US rate expectations and which affords relief – as we discussed last friday – for EM currencies and of course, commodities

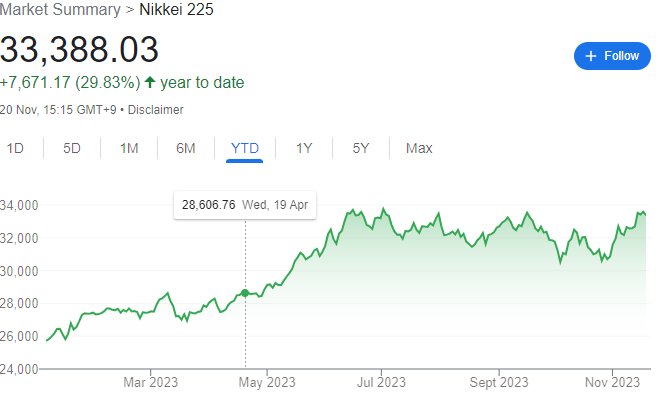

Another darling theme of ours has been the rejuvenation of the Japanese mkt and business landscape

Nikkei225 + 30% ytd now

We continue to highlight the changing dynamics of Japan’s corporate world, no change to bond mkt/ YCC dynamics any time soon fuelling momo

@richard – hadn’t seen owing to chaotic am but thanks

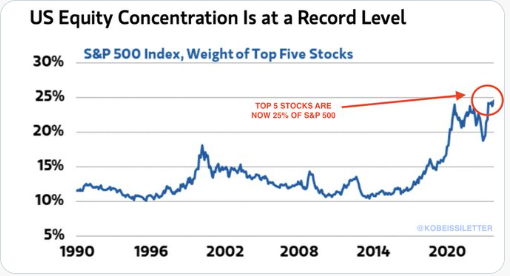

And regarding US equities…

Look at this continued in fact increasing concentration in the mkt

Something we’ve been highlighting for a while is the likely continuation of this theme of the Big Tech maintaining favour and those PMs who are UW being forced to chase into year-end

We did see the Russell 2000, the US small cap index rally 5% last week, though. 40% of the companies in it are loss-making. This asset class has shorter duration debt and more leverage generally. This group attracted $1.7bn in Nov thus far, first inflows in months

Russell 2000 “lured nearly $1.7 billion to US small-cap funds so far in November, EPFR Global data showed, the first inflow in four months. And history bodes well — since the late-1980s, US small caps have typically gained 16.5% in the average of nine months between the last rate hike and the first cut, according to CFRA Research. The S&P 500, meanwhile, has risen 13.2%.” according to bberg

Small caps are also testing resistance levels

Key determinant for equities will be this weekend’s Black Friday and Cyber Monday sales.

I’m not sure how relevant the metrics for these shopping holidays are

Their establishment as conventional dates for discounts means families may simply be saving up to spend on Black Friday or Cyber Monday, meaning record sales figures could just as easily be considered bearish, no? But then again, what does this zoomer know about the economy…

@richard – you mean $ down = equity weakness? US investors dont care, though?

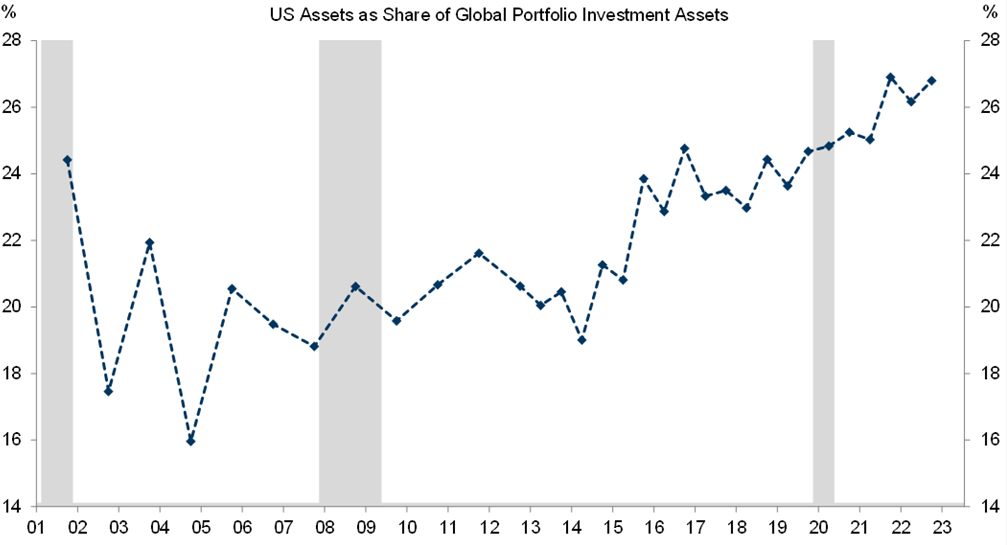

The following chart from GS shows how US equities make up 28% of global positioning (stocks and bonds). This chart has been updated since the end of 2022 but I can only imagine it’s increased since then.

The world’s reserve currency yields 5%, gdp growth in 2024 of 2.1% so the dollar weakness will be contained IMHO

Big week for the US consumer with Thanksgiving/ Black Friday/ Cyber Monday trifecta. Corporate buybacks, momentum, window dressing all inform ongoing strength in equities even if systematic trading community has largely covered its shorts.

In terms of CB decisions this week

Sweden’s Riksbank is debating a further hike of 25bps to 4.25%

Turkey’s CBRT expected for a further aggressive rate hike of 250 bps

Nigeria’s CBN hike forecast ranging from 75 to 200bps

Hungary, however, is expected to cut a further 75bps

At this juncture, your humble correspondent has to bow out and retire his innings early and I leave you in Dario’s hands until tomorrow

Adios

Speaking of irrecoverable losses

(I feel so excited being here all alone, I could tank Izzy’s entire business and there’s nobody to stop me)

So, speaking of losses

Snoop Dog – whose real name is Calvin Barkus

(joke – it’s Broadus)

Created a bear market in weed focused stocks yesterday after he claimed he’d ‘quit the smoke’

Turns out it was all a marketing stunt for smokeless stoves

For instance, Global X Cannabis ETF opened 1.5% lower on Friday

But more interestingly

The news comes amidst a series of generally poor business years for large legal marijuana companies – most have become straddled with debt and unable to focus on business dev

But

Senator Kirsten Gillibrand may be coming to the rescue – calling on the DEA to reschedule marijuana

The Senator asked cannabis to be moved to a Schedule III drug which will alleviate difficulties with prescriptions and medical research

Though a Schedule III recommendation falls short of descheduling, such a move would bring the drug closer to being legally available via prescription, and would enable greater liquidity to find its way into the industry as it searches for more medical uses.

Considering the general momentum of marijuana legalisation worldwide and in the US in particular, the words of a former FDA official, ring very true. He claimed he’d be ‘shocked’ if the DEA didn’t reschedule marijuana by next years presidential election

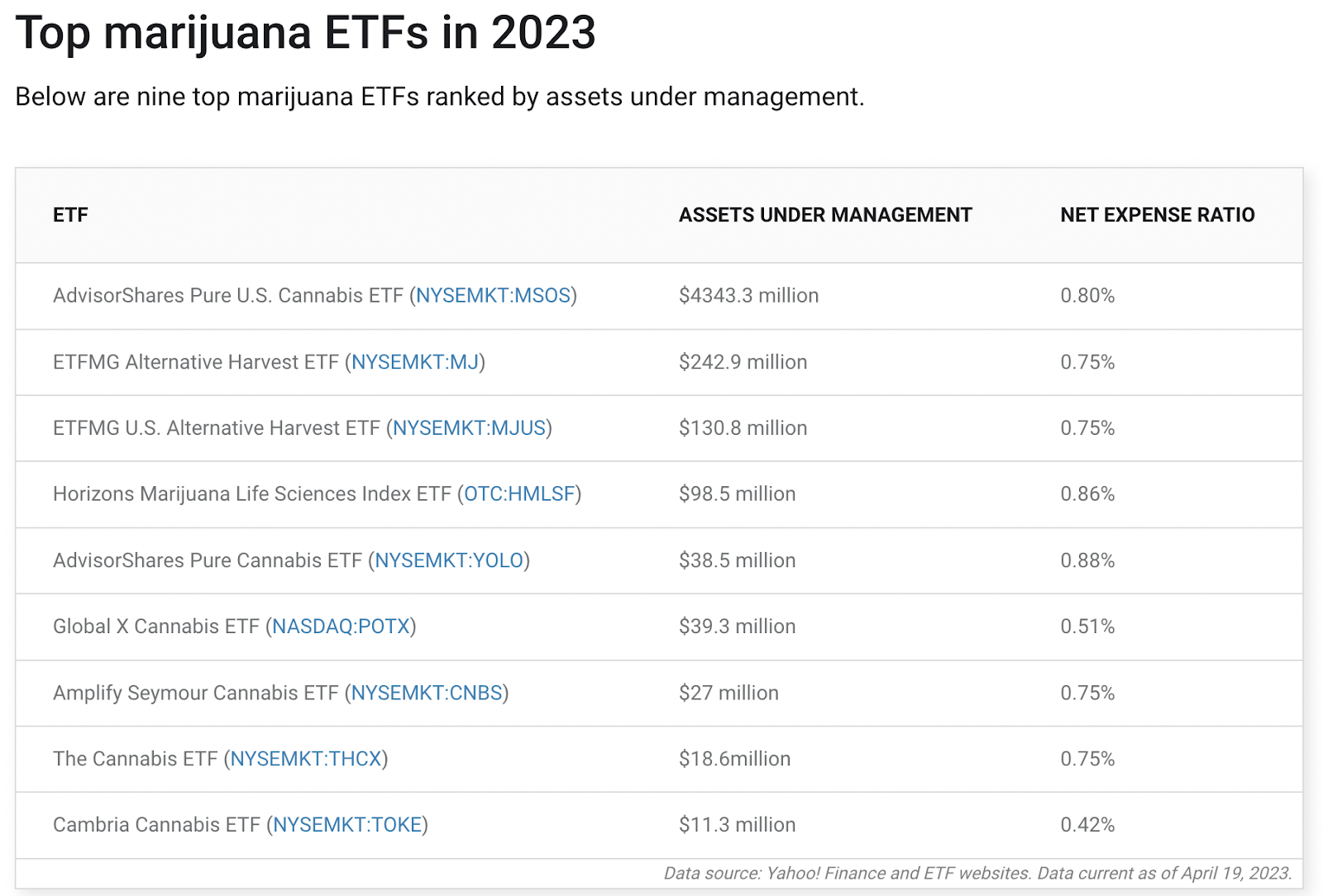

And here’s a list of investable ETFs to regale your investment munchies

One final thing that’s non markets related for y’all

I bet you didn’t know that in the 1950s Argentina’s Peron had claimed to discover cold fusion

This was fruit of a Nazi scientist who was building this secretive project on a mysterious island

Huemul Island

Where most of the infrastructure – including radioactive buckets of radioactive-ey stuff – are still there

The whole online world is filled with scorn at this project but I beg to differ

I think the scientist was funded by Peron but protected by the local Nazi international, meaning he was actually probably NOT researching cold fusion but something else entirely

This is borne out by the very strange behaviour the nazi scientist exhibited during a visit by international scientists

Including leaving a geiger counter behind a anti radiation screen during tests to see if his inventions could produce radioactivity

The scientist – Ronald Richter – was alternatively called either a great genius, or an absolute idiot

His nervousness and sweat, and very very strange mistakes, strikes me as typical of a man caught between a rock and a hard place.

And was caught out by peron’s announcement

On this nuclear note, I wish you all a merry Tuesday!

Thank you for reading 🙂

Tschuss, shatzies!