Good morning!

FRANCES COPPOLA10:58

FRANCES COPPOLA10:58Morning!

Anjuli Davies10:59

Anjuli Davies10:59Welcome back

Did you have a good Easter break?

I did. Northumberland is beautiful at this time of year.

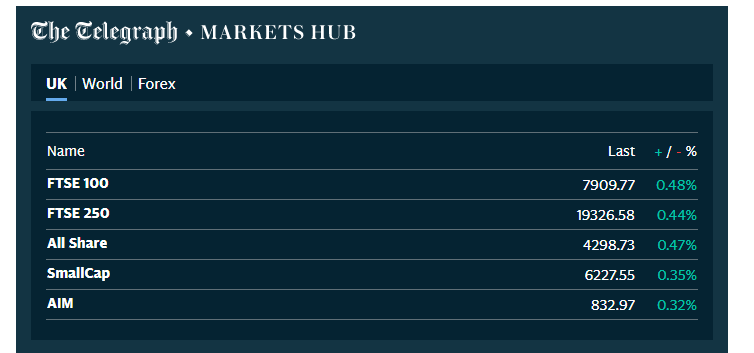

Anjuli Davies10:59Sun’s out, markets are up – what’s there to talk about?

Nicely green. Apart from Barclays .

Anjuli Davies11:01There’s been quite a few M&A announcements involving UK plc over the weekend and this morning

Barclays stock has slid because it just can’t rid itself of that Epstein problem.

Anjuli Davies11:01Also, reports its cutting 100 investment banking jobs

Does that include Jes Staley?

Anjuli Davies11:01Must say, I’m still waiting for all the IBs to follow Goldman with the job cuts

Apollo has been busy

Monday 17 April, 2023

Apollo Global Management, Inc.

Apollo Strengthens Presence in Europe With New, Expanded London Office

Relocation Reflects Apollo’s Commitment to Delivering Full Platform to Europe

LONDON and NEW YORK, April 17, 2023 (GLOBE NEWSWIRE) — Apollo (NYSE: APO) today announced the opening of a new office in London, United Kingdom, strengthening its presence in Europe and building on the firm’s successful track record in the region. The transition to a single, modern space in London reflects Apollo’s desire to offer a best-in-class workplace for its teams and expand its offering of leading, integrated asset management and retirement services capabilities on a global basis, including across European markets.

This as news leaked that they have made a bid for online retailer THG – shares of which have surged by 40 %

Also, that it is in discussions with John Wood Group

Share price up 19% this morning

But we need to talk about banks.

Anjuli Davies11:07Yes, we always do !

Andrew Bailey is considering a major reform of the UK’s deposit insurance scheme in the wake of SVB’s resolution

Anjuli Davies11:08Is this a good thing Frances?

Patrick Jenkins at the FT thinks so.

Anjuli Davies11:09Andrew Bailey has said the Bank of England is working on a reform of Britain’s bank deposit insurance guarantee scheme, raising the prospect of increased protection for customers. Speaking in response to high-profile bank failures on both sides of the Atlantic, the BoE governor suggested the UK might need to increase its limit for guaranteed deposits above the current £85,000 — which is far lower than the $250,000 level in the US. Bailey said the current UK scheme was unlikely to work as intended for smaller banks and questioned the rule that there was a clear dividing line between deposits that were guaranteed and ones that were not. “Practice, I would suggest, points to the difficulty of this principle,” he told the Institute of International Finance in Washington.

here’s the article

I think there’s a case to raise the limit, not least because inflation is eroding it so much. But we need to think more creatively.

For example, why not charge large depositors for in-excess deposit insurance?

Anjuli Davies11:11The free lunch is over

But the question is who should pay

Raising the limit considerably and increasing pre-funding of the insurance fund would hit customers of large banks

Anjuli Davies11:12I did get a random message from my aunt over the weekend who works at an American University in Grenada saying that all her colleagues were panicking about where to put their money..

Charging large bank customers more for deposit insurance would be fine if the risks were coming from large banks. But they aren’t.

They are coming from smaller banks that have inadequate capital and liquidity buffers

Anjuli Davies11:13This seems to question the whole viability of small banks

It’s not clear to me why the customers of large banks should subsidise large depositors in small banks

Anjuli Davies11:16Is it time to start charging for ATM withdrawals and other banking services

I’ve thought for a long time that free-while-in-credit banking had to end

Anjuli Davies11:18You’ve written an interesting commentary on the fractional reserve crisis Frances

Yes, it’s a keynote speech I gave at the University of Ghent last week. When you define “fractional reserve” to mean that an institution’s assets are less liquid than its liabilities, it’s surprising how many things are fractionally reserved.

Anjuli Davies11:21Now, of course, there’s a flurry of regulatory activity “to protect the public”. New rules for pension funds and their advisors; new rules for bank capital and liquidity; and above all, a raft of new rules to bring the crypto industry to heel. The stable doors are not only being shut, but reinforced, and an array of shiny new padlocks is being installed. But the horses have disappeared into the shadows, where they are already building the next generation of shadow banks.

The LDI crisis last September was a fractional reserve crisis. John Ralfe (pensions expert) said on Twitter this morning that leveraged LDI is effectively fractional reserve banking.

Anjuli Davies11:22The horse has already bolted

So the regulators will now clamp down on leveraged LDI but the risk will simply move somewhere else.

Exactly Anjuli.

Anjuli Davies11:23The like of JPMorgan, Citi last week show they are making a ton of money of paying people nothing in rates and lending people at high rates

There’s been a lot of stuff in the press about deposits fleeing banks for MMMFs

Anjuli Davies11:24Blackrock results seemed to solidify that view

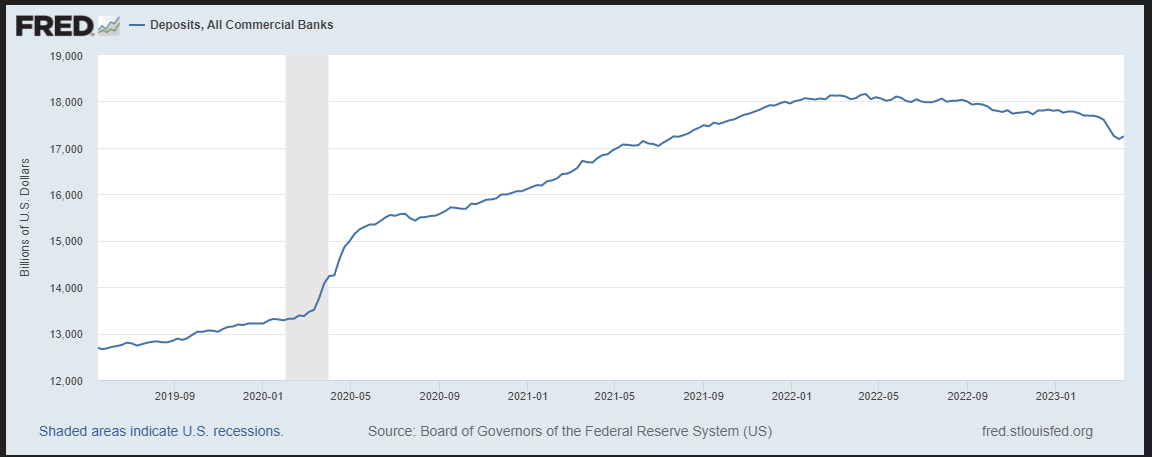

But here’s some perspective

Deposits in US commercial banks still far above what they were prior to the pandemic

Anjuli Davies11:25I guess the capital markets structure in Europe is so different

Much more dependent on banks.

US banks are now under pressure to raise rates for savers, but European banks feel no such pressure because there are no easy alternatives to bank accounts

Personally I would impose windfall taxes on banks that are juicing their NIM by failing to pass on interest rate rises to savers

Anjuli Davies11:29I wanted to raise an article by Reuters last week on “Significant Risk Transfers” (SRTs) that apparently are gaining traction with European banks to offload risks via synthetic securitisations

Sounds to me very risky and one that could be storing up a lot of dangers

European banks are increasingly turning to bespoke deals with investors such as hedge funds to offload some of the risk on multi-billion euro loan portfolios and improve their financial strength, several sources involved told Reuters.

Banks supervised by the European Central Bank (ECB), the biggest ones in the euro zone, completed a record 174 billion euros ($189 billion) of such deals last year, the regulator told Reuters.

Oh look, an opaque arms-length securitisation scheme to reduce capital. What could possibly go wrong?

Anjuli Davies11:31By offloading some of the risk on their loans, the banks can significantly reduce how much capital they need to set aside to cover potential losses, according to law firm Clifford Chance.

Unlike a traditional securitisation, in which a bank’s assets are moved to a separate entity that then sells securities to investors, SRTs are often “synthetic” and mimic a sale.

Same old jive.

The problem here is opacity, I would suggest. Offloading risk is not itself a problem.

Anjuli Davies11:32Add in some derivatives

Always

Also there is the thorny question of overdrafts – should the central bank allow ordinary households and businesses to go overdrawn?

it doesn’t allow banks to do so on any more than a daylight basis (and not all central banks even allow that)

I wonder how liquid such a system would be if overdrafts were not permitted

@Bruce that’s an interesting development. Wise seems to be on its way to becoming an actual bank.

Anjuli Davies11:46Should we mention a quick look at the week ahead?

Whether or not we have a public payments system, I think regulators need to be much clearer about the distinction between payment services and banking

Anjuli Davies11:46China watching obviously high up on the agenda

China GDP figures expected to be strong, which is good news for the world economy

Anjuli Davies11:47the release of China’s Q1 GDP growth, where our economists are expecting an above-consensus print of +4.5% year-on-year.

From Deutsche Bank

Otherwise, inflation will remain in the spotlight, with this week seeing the March CPI releases from Japan and the UK. In Japan, our economist expects core-core inflation excluding fresh food and energy to tick up slightly to 3.6%, up from 3.5% the previous month. And in the UK, we’re anticipating a decline to 9.7%, down from 10.4% in February.

Japan’s new BOJ chief has been speaking

WASHINGTON, April 16 (Reuters) – Japan’s new central bank Governor Kazuo Ueda gave a clear message to policymakers gathered for global finance meetings here over the last week: The country will remain a dovish outlier by keeping interest rates ultra-low – at least for now.

Since taking the helm a week ago, Ueda has dropped some hints the massive stimulus of his dovish predecessor Haruhiko Kuroda will eventually be phased out.

But discussions over when and how to shift away from the ultra-loose policy will take time, giving Ueda every reason to reassure the world any change won’t happen quickly.

@Graham payments processors always end up becoming some kind of bank. Revolut is quite far down that path.

we need Izzy to talk about float….

Anjuli Davies11:52Economists are now predicting a pause in rate hikes in May

Attention turning from inflation to growth

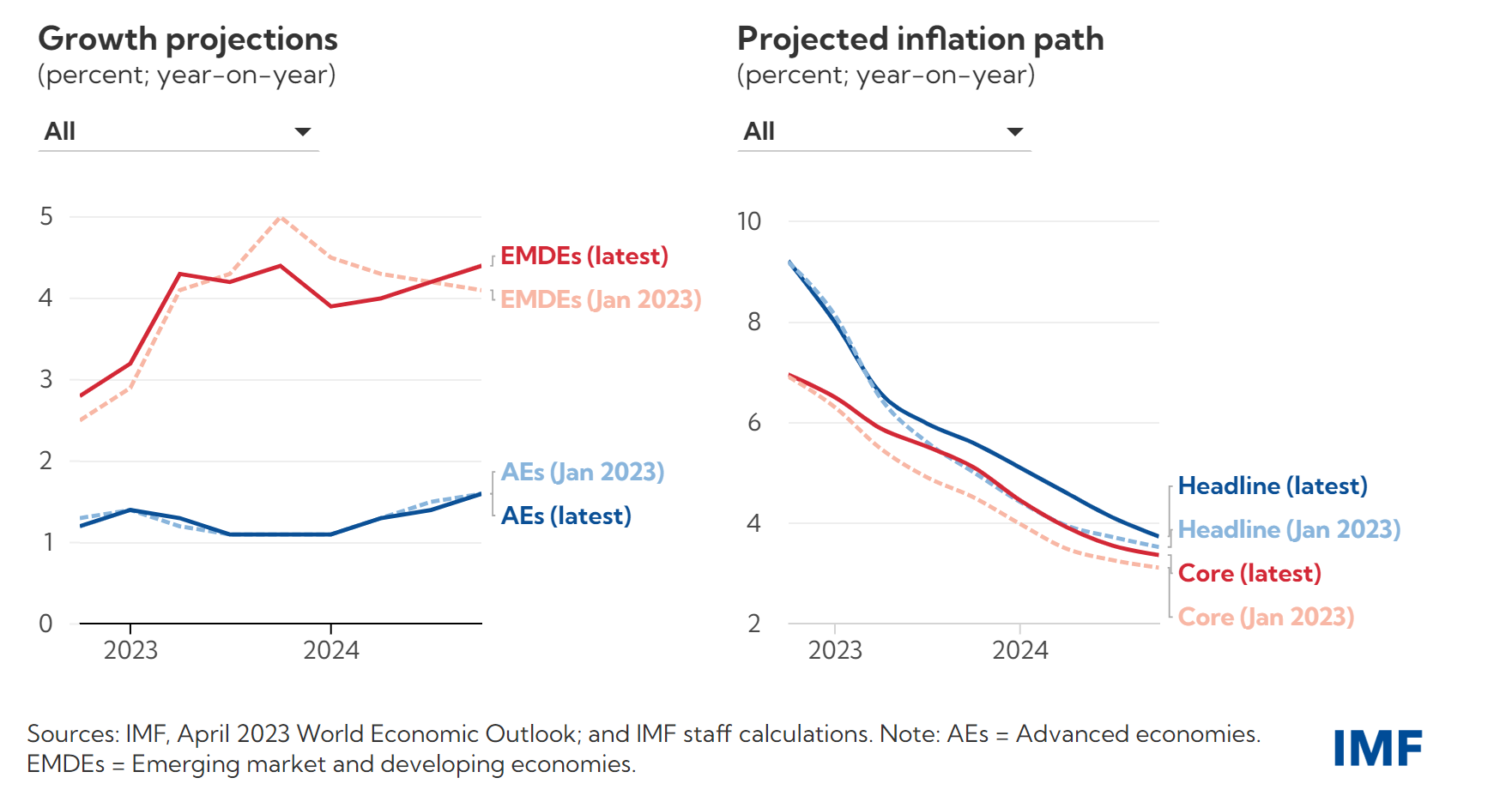

IMF forecasts poor growth, especially in advanced economies.

This year’s economic slowdown is concentrated in advanced economies, especially the euro area and the United Kingdom, where growth is expected to fall to 0.8 percent and -0.3 percent this year before rebounding to 1.4 and 1 percent respectively. By contrast, despite a 0.5 percentage point downward revision, many emerging market and developing economies are picking up, with year-end to year-end growth accelerating to 4.5 percent in 2023 from 2.8 percent in 2022.

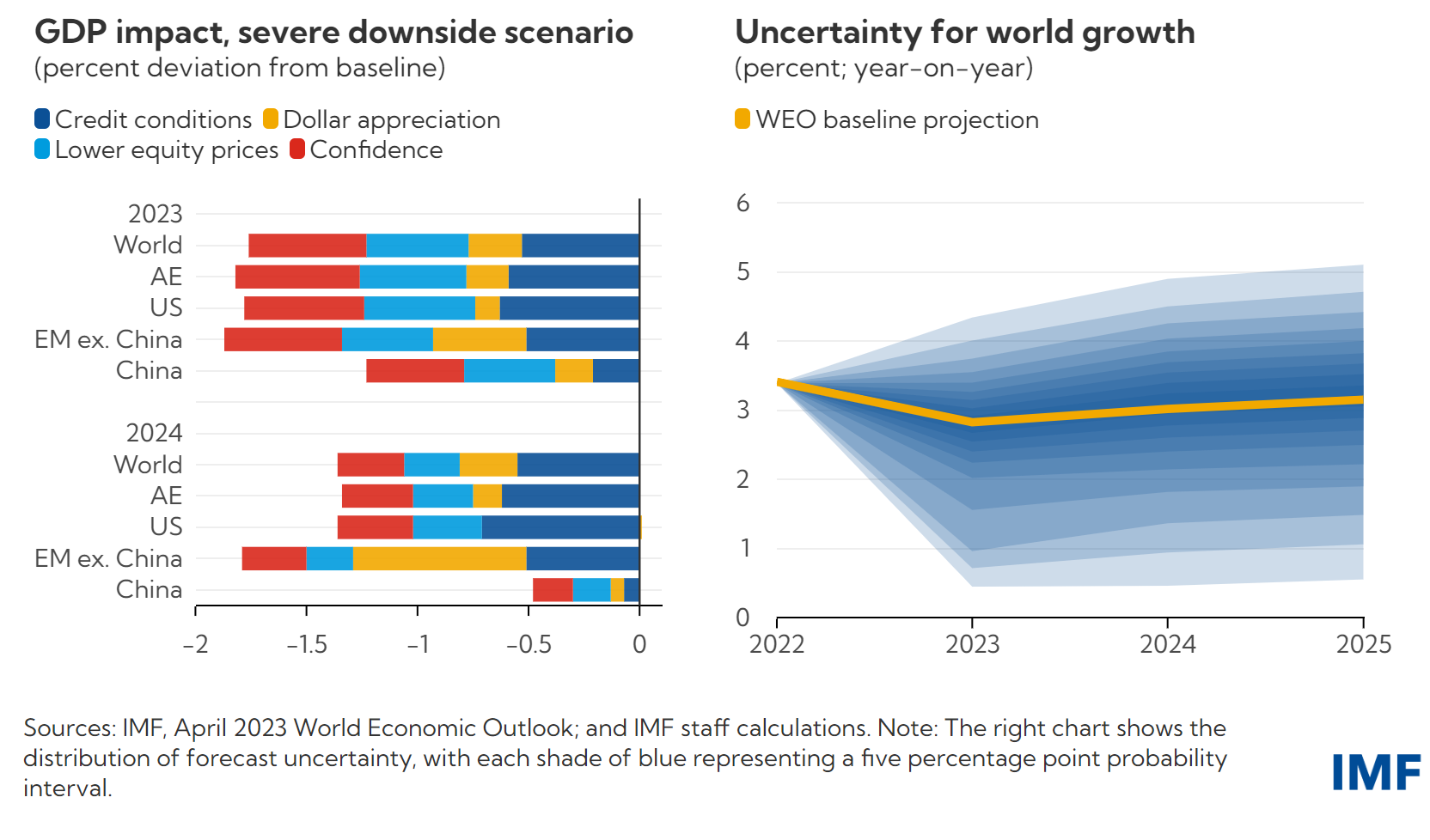

IMF also warns that credit tightening by banks might make the outlook even worse.

A sharp tightening of global financial conditions—a so-called ‘risk-off’ event—could have a dramatic impact on credit conditions and public finances, especially in emerging market and developing economies. It would precipitate large capital outflows, a sudden increase in risk premia, a dollar appreciation in a rush to safety, and major declines in global activity amid lower confidence, household spending and investment.

In such a severe downside scenario, global growth could slow to 1 percent this year, implying near stagnant income per capita. We estimate the probability of such an outcome at about 15 percent.

There are no official figures for the total scale of BRI lending over the past decade, but it is believed to total “somewhere in the ballpark of $1tn”, according to Brad Parks, executive director of AidData at William and Mary university in the US.

In addition, Beijing has extended an unprecedented volume of “rescue loans” to prevent sovereign defaults by big borrowers among about 150 countries that have signed up to the BRI.

Anjuli Davies11:59oh dear…

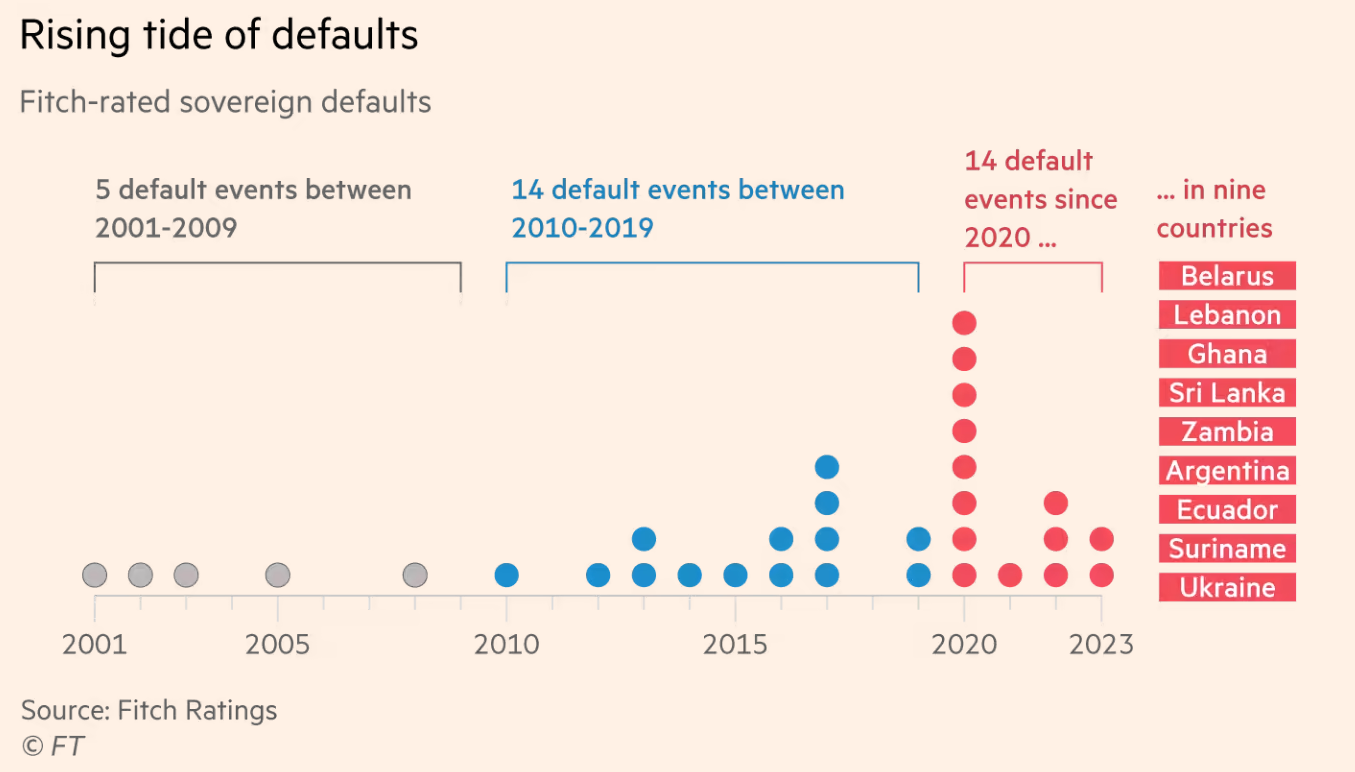

And just to frighten us all, the FT has a lovely chart on sovereign defaults.

May you live in interesting times.

Anjuli Davies12:00It started with sunny times and ended with…

Gloom. Sorry, everyone.

Anjuli Davies12:00On that note, it’s a wrap for today

Thanks Frances

I’ll try to be more positive next time!

Anjuli Davies12:01It’s hard to be at the moment

Bye for now, everyone.