Good morning, aloha and greetings, fellow market wizards

Once again I’m joined by Dario down there in the south of Spain which is where someone who spent three decades in the city should be but isn’t

morning dario

Aloha!

before we beging, please accept my apologies in advance for the explected tsunami of typos this morning as I’m on a tiny screen in the back of my wine shop, awaiting the delivery of a pallet of wine any moment

nunc tempus loquendi. It is crisp autumnal days of singular beauty like this which inspired the great exponents of the Japanese haiku

i’m talking basho, issa, kyoshi, shiki and wishiwashi here

ok i made the last one up

????

this is the kind of morning which would have inspired them to wax lyrical about lambent leaves and pale moons but of course, climate change had to ruin all of that and it is wreaking havoc on the modern writers of haiku.

like me

I welcome climate change – I get to tan every day now

i have a viking’s pigmentation and burn even watching an ad for a beach holiday on the telly

We shall not discuss yesterday’s excellent CPI datum (an example of the rhetorical device apophasis) because our nomenclature – the blind spot – demands that we plough the lonely furrow, ramble the untrodden ways, sail uncharted waters and frankly CPI is just too obvious to discuss.

We’re allowed to meme about it though, aren’t we?

i can’t believe we are using the noun meme as a verb

me irl:

(grammatical terminology is anthimeria)

me irlirl:

here’s a big word for you, Dario

the correct term for a bullfighter is tauromach

so, I guess those who fight bears are ‘ursomach’

fascinating

cool word!

I’ve also found some contrarian tidbits on CPI, courtesy of Marc Ostwald

He reminded us that headline and Core inflation is still at 3.2% y/y and 4.0% y/y, and services CPI rising 5.1% y/y and at 5.2% 3-month annualised

“it basically suggests that rates are ‘sufficiently restrictive’, but is a far cry from suggesting the inflation battle has largely been won.”

the key determinant for whether the battle against inflation is won is probably not monetary policy, sadly, but geopolitics, especially in Gaza

And speaking of

any update on that, Dario

Well, did you know that this summer the Israeli government greenlit the development of 32bn cubic metres of gas in the Gaza Marine gas field?

i think i had a vague knowledge of that

but fill me in

Well, it’s not really Israel’s to parcel out. and as you can imagine, there’s a whole kerfuffle online around it

With a lot of fake news – and the number 500bn. The 500bn estimate of gas reserves are for the WHOLE levant region, rather than the relatively small reserves in Gaza’s territorial waters

Regardless, Israel greenlit this development on June 2023 – rather unfortunate timing – and with Hamas backing to boot.

hamas backed it?

Development had been blocked for almost 20 years, in part because of its relatively small size, and especially since the Hamas takeover of Gaza in 2007.

The PA’s presence on the field would have been nominal – shared revenues

I wonder if that was all part of the strategy of hamas to make israel feel like relations were improving

De-facto, Israeli operation, adjudication and control over the gas field was assumed

Shell gave up on it in 2018

My guess is that if Israel takes control over the Gaza strip, the Gaza Marine revenues will come with it

And in other marine geopolitical news

China continues to harass philippino sailors on the Second Thomas Shoal, a submerged mini-reef within UN-recognised Philippine waters which are disputed by China

This i did hear about. Chinese behaviour in their eponymous sea is appalling

They’ve been harassing the Philippino base with water cannons and lasers, as the US continues to proclaim its standing by its ally

But the clue to the conflicts winner is in the map – it is the South China Sea after all

It’s a matter of time…

On that basis when I worked at Barings we could have taken control of the sea north of Russia.

You mean the Arctic?!

ok, it’s spelled Bering

(graveyard of the russian submarine fleet)

And lastly, Exxon Mobil has just begun flowing oil from its third project in offshore Guyana

Their FPSO started producing yesterday ahead of schedule

The vessel is expected to reach initial production of approx 220,000 barrels of oil per day – bringing the US giant close to around 1.2mn barrels per day on the Guyanese block by year-end 2027.

This coincided with representatives from Venezuela and Guyana fighting it out in the Hague yesterday in their historic fight over Essequibo sovereignty

why is that in the Hague?

Guyana brought it there after Venezuela started a referendum on whether it should annex the region

hopefully, their representatives will see Putin arriving there shortly on the back of a flatbed truck with his hands bound

Speaking of shorts – Michael Burry has just closed his shorts on the SPDR S&P 500 ETF and Invesco QQQ Trust, which tracks the Nasdaq 100 at the end of September

The bearish bets amounted to around $1.6bn with everything indicating he made a couple hunny millies on the trade

And now he’s hungry for more

Scion isn’t the first hedgie to get a semi for betting against semiconductors

burry a victim of ursomachy

A large number of shorts came in after Biden signed the CHIPS act in Aug 2022 which gave $39bn to the industry in the US

And it hasn’t been going great.

Short sellers have lost 92% of every dollar in their bet against chip stocks, as semiconductor short paper losses top $18bn in 2023.

Fascinating John !!!

yesterday, Goldmans most-shorted index spike 6% in the aftermath of that cpi release

Speaking of bubbles

Do you mean michael jackson’s monkey?

Ummmmmmm

Americans have $1.8tn in student loan debt, 92% of which is Federal

Apparently student loan service providers are filled to the brim with web crashes and failures – such as Nelnet’s ($NNI)

These crashes are so common there are even websites about how to handle the stress

This is alongside loads of incorrect billings, falling profits and cash flow for loan service providers

I presume if one has a student loan and needs to repay it but the website goes down then one has an inbuilt excuse ready

kinda like dog ate my homework?

Well, students have been emboldened by Biden’s loan forgiveness

Now, 50-60% of students state they don’t intend to repay their loans – seeing as they didn’t have to for 3 years – and still won’t even if loan forgiveness was ccancelled

On a related story – I hadn’t heard of Student Loan Asset Backed Securities. had you Julian?

Yes, of course, I’m very familiar with them (he says typing SLABs into a search engine) I dont think I’ve paid back my student loan yet so this is material to me.

Student loans are packaged, marketed and sold as asset-backed securities known as SLABS

SLABS lower lending risk by pooling and packaging loans into securities and selling them to investors

I know squat about economics. But that sounds like a CDS to me

i would say that sounds like one of those toxic collateralised bond obligations FAbulous Fabio at Goldmansd was trading back in 2008 which caused all the trouble back then

Now, the SLABS market is much, MUCH smaller than CDS – posing much less systemic risk to the economy. Plus. Federal loans to students without a credit check can’t be securitised.

But Federal Family Education Loan Program loans were federally guaranteed loans made by private lenders (which CAN be securitised – even though the FFELP was ended in 2010) do carry some risk – and are precisely what encouraged SLABS for securitisation in the first place.

“I saw the parallels and it really freaked me out because I realized that this cycle was only going to repeat,” said Allison Pyburn, an asset-backed securitization expert and former editor-in-chief at Debtwire ABS. She continued, “I think one of the key ways to uncover the similarities between student loans and mortgages is to look at the affordability issue.”

“The national cohort default rate for student loans has plummeted, according to the U.S. Department of Education, boosted by the payment pause during the Covid-19 pandemic. But the Consumer Financial Protection Bureau estimates that one in five student loan borrowers have risk factors that could cause them to struggle when federal student loan payments resume in October.”

“I think what’s scary about it and what was scary about 2008 was the tremendous uncertainty that everyone had about what valuation even was,” said Pyburn.

changing the direction of travel somewhat

i’m not one for gossip generally

mostly because i dont know whats going on

but front page of the FT this morning…, an article informing us that the head of trading at Elliott (rememeber we discussed this fund yesterday) has resigned after twenty years

james bayliss

and for once, i know someone in the news

elliott were my biggest client for many years as a salestrader

and in fact, a very large unsolicited discretionary order from them in 2010

when i was working as a self-employed broker

actually paid for the sauna i had installed in my garden shed

i have a brass plaque

on which is engraved

This sauna was bestowed by the munificence of Elliott Advisers

sadly, james then took over trading, he and I didnt get on and I never dealth with theem again

From the FT: As head trader, Bayliss would typically focus on executing trades on behalf of the firm and oversee relationships with brokers and bank trading desks’

i cant tell you what he was like as a trader but I would say he struggled with the second half of of his job responsibility

and of course, as my grandfather repeatedly advised

i hold my grudges

another departure (this one may be lamented by some people|)

was the retirement of the Emerging Market specialist Mark Mobius

who at the age of 87 appears to be hanging up his headset

he was thee only person I knew who had been in Emerging Markets longer than me

but he was not the only person I knew who had made a lot more money from Emerging Markets than me

I met him properly once where he was the speaker at an event my wife hosted

and my only role that day was to greet him at the 4 seaosn hotel lobby and bring him up to the event where he was the guest speaker

as he arrived i hesitated inside the revolving doors, he came in, as i went out, i got stuck, i lost him, he went AWOL for a good fifteen minutes

after that my wife sacked me as meeter and greeter and front of house for her events

????????????????????????

that is what passes for gossip at the blind spot

JP Morgan Global Data Watch

I’m thrilled and on the edge of my seat

yes, it’s the kind of title which makes everyone put down their knitting, sit up and take notice.

but, of course, it’s the heavy lifting/ necessary reading that must be completed if you want to know what’s going on

and it’s satisfying ehen they start off by telling you what they got wrong this year

JPM hugely underestimated global gdp this yr. Their estimate of 1.7% way too conservative and 1H ended up at 2.7% and 2H looks like will show 3.5%.

trend growth is 2.2% so central banks the world over havent done too bad a job in dealing with the first inflation shock in forty years

in fact, the global economy(this is me btw, not JPM) coped very well with the biggest demand boom in history during the pandemic

considering how subdued inflation has actually been compared to previous shocks

JPM: ”As we entered 2023, the US was the only large economy that had returned to its pre-pandemic potential growth path. At the same time, a shortfall of more than 2%-pts had opened for China, Europe, and most of EM. Although we anticipated a sluggish US to narrow this gap, it has widened further as the US delivered strong absolute and relative performance”

this for me, underscores why it’s probably still too early to dismount the Big Tech nag in the US

It all comes down to the consumer: Several factors are contributing to the US-Europe growth gap, including fiscal, COVID, and energy price dynamics but I think it’s the longer mortgages available in the US where 30yr deals are the norm as opposed to the 3-5 yrs in Europe which means interest rates are biting already.

Europe is clearly struggling in comparison

i read Aurora’s strategy update last night

they note

Eurozone not in recession but it is stagnating, growth estimates for 2023 @ 0.7% by IMF/ ECB etc way too optimistic and 0.1% FY23 most likely with ~1% in 2024.

that’s pretty anaemic

it’s not technically a recession but very much feeling like one.

(question for self: there is a reason I pay attention to Aurora but I cant remember what it is. check later)

So Izzy tells me it’s a spin out from Niall Ferguson’s Greenmantle – two analysts from there who started their own shop

aha. i’m a Ferguson fanboy so that’s why I attach credence to it

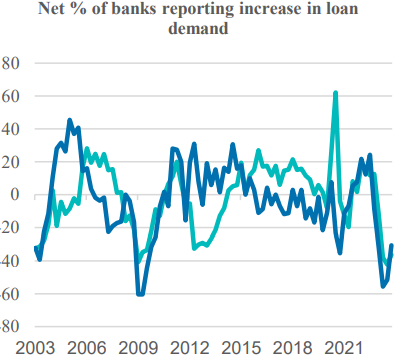

they observed that loan demand in the Eurozone has fallen to levels comparable with the GFC

it’s clear monetary transmission is working well, perhaps too well

as an analyst I respect, tech guru, Harvey Robinson @ Panmure wrily observed…

the BOE tried to break the uk economy to kill inflation and they broke the economy

Speaking of analysts – Rabble: what are your picks for best/worst analysts in your opinions?!

Demand for loans to enterprises is now near an all-time low, with a net percentage of 36% of banks reporting lower demand for credit. And it’s not just higher rates but also less corporate demand for fixed investment.i

In this context, our present base case is one where Eurozone stagflation continues well into next year, and eventually forces the ECB to cut rates. • The market is currently pricing 44bps of cuts between now and July 2024 for an implied rate of 3.45% (from a current 3.9%)

that’s Aurora also

it looks to me like Europen equities have priced this in, though

At a12X trailing P/E ratio, the SX5E is trading near an all-time high discount to the SP 500’s 21.2X—around 45%.

so that pair trade isnt one to put on here

Well – the trouble goes further than a shallow recession for Europe

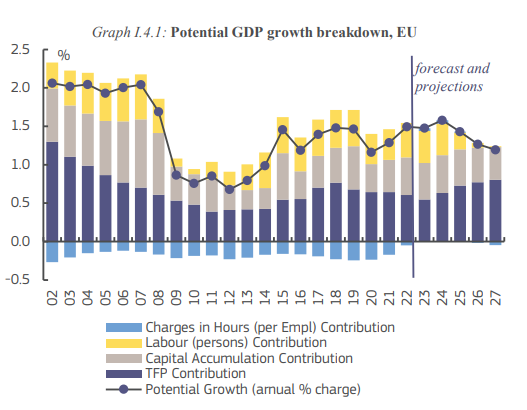

As Eurozone potential growth continues to be predicted to drop over the next few years

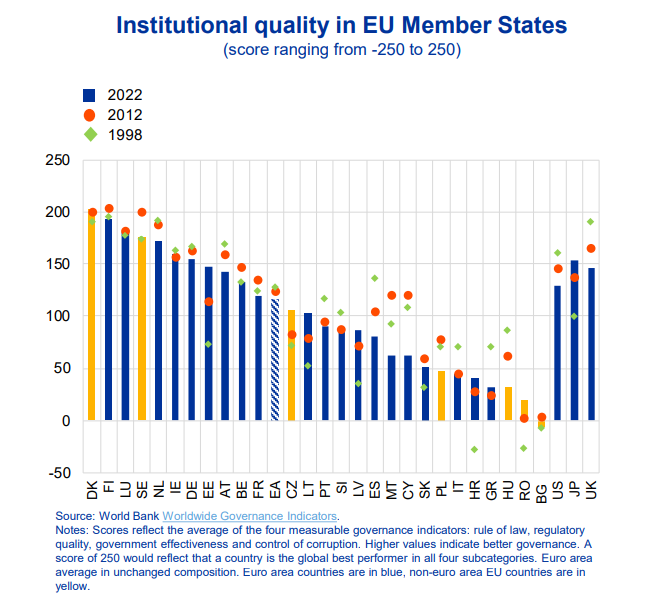

This coincides with a perceived crisis in governance, as the quality of institutions in EU member states has been consistently dropping in most EU countries since 1998

According to the World Bank’s Worldwide Governance Indicators:

i’m interested to know if the same criteria were applied to Asia and America whether their relative performance would be much improved?

You can actually see on the right hand bit there – only Japan has improved (and Ireland!)

You obv cant see it on your tiny screen even my Zoomer eyes were struggling

everyone likes to beat up on the EU to point out its failings but I think it’s always salutary to note, people still die trying to get there into the arms of these institutions

Speaking of worsening european institutions

Siemens Energy was just granted €15bn rescue package that was underwritten by the German govt to sustain a planned portfolio of €110bn clean energy projects.

I hate wind turbine projects personally. Their damage on the environment in formerly beautiful sea-side plains of Cadiz is a disaster. From the most pristine spot in Spain to a horrible ‘hum’ that murders flocks of birds

Bring back coal! I’d rather burn dinosaurs than kill birds and good views

that’s obviously what Glencore were thinking when they announced their purchase of Teck Coal yesterday

On things Hispanic…

chapeaux, dario, for your exegesis on Spanish politics yesterday

because I noted last night Aurora also taking a dim view of developments there

Markets have stayed relatively quiet amidst the fiscal largesse, though Spanish 10-year benchmarks have sold off and are now trading at ~105bps above equivalent bunds. • But in our view, the concentration of political risks weighs heavily over the longer run. • Against a backdrop of rising polarization in Spanish society, increasingly chaotic politics (Spain has had 5 general elections in the last 8 years), domestic risks are liable to worsen— especially given renewed national focus on the Catalan issue. • As a result, we are strategically underweight Spanish bonds relative to Eurozone peers.

apres vous le deluge

the mention of Sapnish politics was something WB Yeats |(my second favourite poet) wrote about, I think in his very final poem

How can I, that girl standing there,

My attention fix

On Roman or on Russian

Or on Spanish politics,

Yet here’s a travelled man that knows

What he talks about,

And there’s a politician

That has both read and thought,

And maybe what they say is true

Of war and war’s alarms,

But O that I were young again

And held her in my arms.

so he wasn’t so keen on Sapnish politics

I’m never keen on my home country’s politics. Tragedy after another

actually WB Yeats is my favourite poet when I’m happy and Philip Larkin when I’m depressed. Hence Larkin is generally my favourite poet

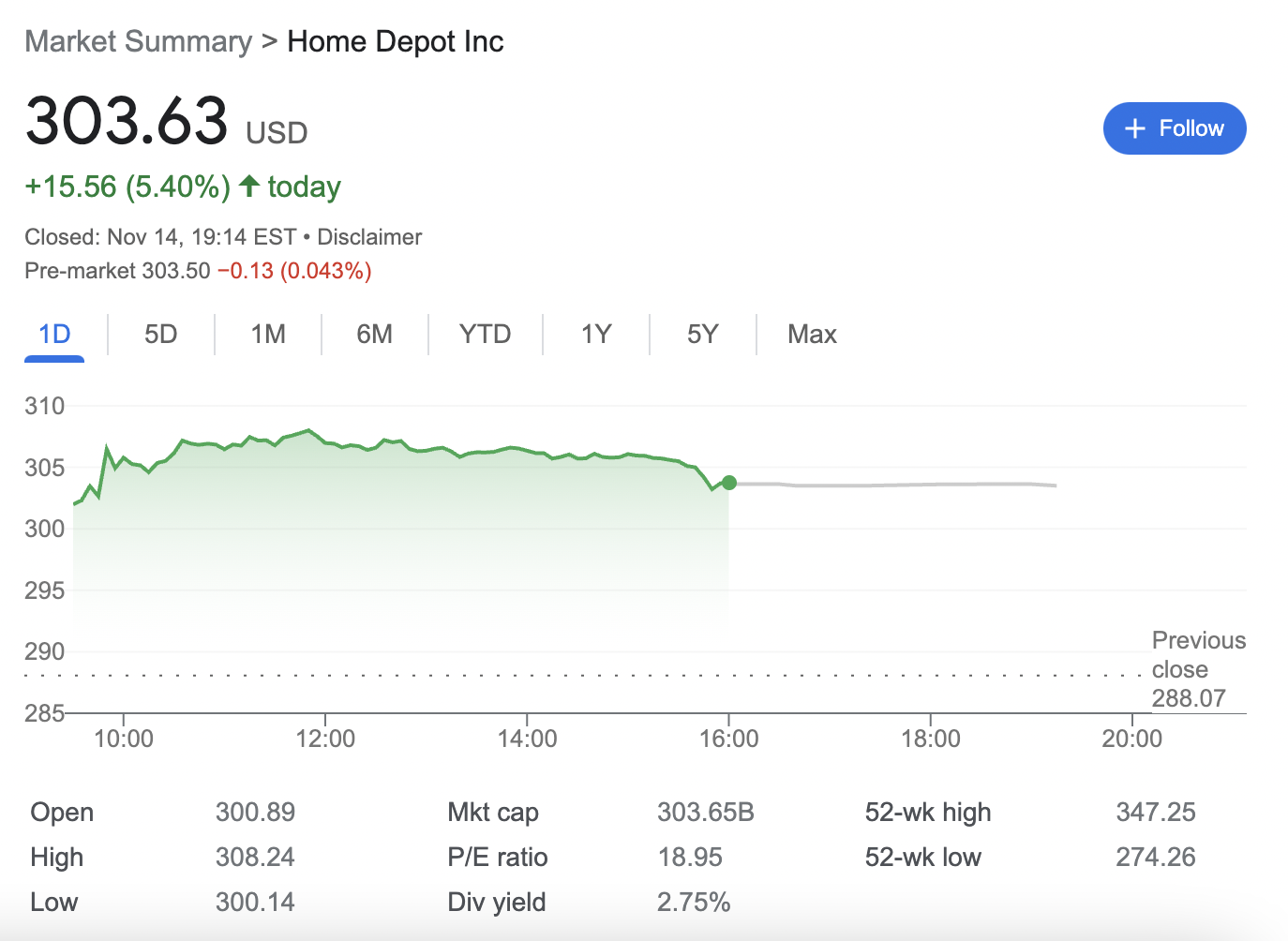

Speaking of homes – Home Depot’s earnings just came in hot

Rounding off a broadly positive week for markets, their Q3 earnings and revenues beat expectations – though its full year guidance indicated caution

While Home Depot’s quarterly sales declined 3% from the year-ago period, it still topped expectations

- Earnings per share: $3.81 vs. $3.76 expected

- Revenue: $37.71 billion vs. $37.6 billion expected

“The company indicated caution about the coming months and narrowed its full-year outlook. It said it now anticipates sales will fall by 3% to 4% from the prior year, compared with a previous expectation of a 2% to 5% decline. Home Depot expects earnings per share to slide by 9% to 11%, compared with prior guidance of a 7% to 13% drop.”

Home Depot reported a net income of $3.81bn or $3.81 per share, down from $4.34 billion, or $4.24 per share, a year earlier. Revenue fell from $38.87 billion in the year-ago period.

this illustrates a general theme here: especially in America… govt data seems to be much better than corporate data!

Naturally, Home Depot has reported that customers are opting for more budget-conscious solutions for home remodelling – partial remodellings rather than full, for instance – and have pulled back on pricier projects and items.

Let’s end on a positive note

Or, let’s look at Albert Edwards latest note instead

he’s renowned as a perma-bear but this week he’s gone maximum bullish and is exhibiting startling amounts of irrational financial exuberance

really?!

No, he’s worse than ever. It’s like spending a night with an insurance salesman reading him

reminds me of woody allen “There are worse things in life than death. Have you ever spent an evening with an insurance salesman?”

Sounds like a punishment fit for the worst behaved of prisoners

Albert is trying to time the bottom in US bond markets, citing the contraction in M2 as a harbinger of hard recession, as it was in the 1930s

(ideally, Albert would have lived in the 1930s)

That’s interesting because Motley Fool wrote an article that was roundly mocked on Reddit on precisely the risks of M2 contraction

He’s using this for timing, and he may be right (|I add charitably) given how the rate cycle is shaping up

i very rarely agree with Albert (about which I’m sure he’s relieved) but there’s a note of harmony on which to conclude today’s depatch from the back of the wine merchants.

nunc tempus taciendi

Aloha!