Izabella Kaminska 11:59

Izabella Kaminska 11:59

Hello and welcome to Spot Markets Live.

The weekly chat that takes stock of what’s going on in the market.

I’m joined today by Helmholtz, a former sell-side pro with nearly 40 years worth of experience running rates desks at various investment banks. Hello Mr H.

Helmholtz 11:59

Helmholtz 11:59Good morning and thanks for inviting me to join you all again.

Izabella Kaminska 11:59It’s been another eventful week.

But I’ve also been at a Bitcoin conference in Amsterdam, so am a little bit out of the loop.

Do you know who else was there?

But before I set off for that, I did sit down with two informed CIO invoices at the ALFIFunds conference on Wednesday, an organisation “leading industry efforts to make Luxembourg the most attractive international centre for investment.”

Have you ever been to Luxembourg, Helmholtz?

Helmholtz 12:01I have several times

Mainly on business at Clearstream.

Beautiful forests roundabout, but a bit soulless and small for me.

Izabella Kaminska 12:02I went for the very first time this year, as we were passing through on our way to the Alpbach conference.

We had schnitzel and the castle was very nice, but it is tiny.

But anyway I was joined on the panel by Johanna Kyrklund, the group chief investment officer at Schroders, so I simply had to ask her about LDI. And actually, she was quite obliging.

She acknowledged Schroders had exposure, but that with the BoE intervention it was mainly a liquidity issue.

She seemed confident that the doom loop might be squared within a couple of weeks.

What do you make of that?

Helmholtz 12:03After yesterday I think (hope?) she may be correct;

The lack of a significant fall in the gilt market after Andrew Bailey’s comments about closing the purchase facility tonight, and then the incredible rally yesterday and today after the US CPI print makes me much more comfortable that the gilt market has found a clearing level.

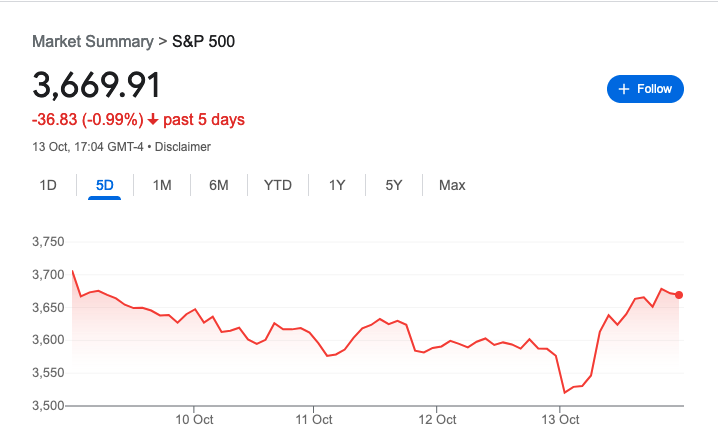

Izabella Kaminska 12:03Yes, US CORE CPI rose 6.6 percent on an annual basis last month despite the decreases we have seen in energy prices.

The more general measure rose by 8.3 percent.

Also worth noting China’s CPI has jumped this morning the most in more than two years, increasing by 2.8% in September.

Here’s Marc Ostwald of ADMSi this morning on the inflation news:

After yesterday’s upside surprise on CPI, the focus shifts to activity and sentiment data, given that the expected fall in Import Prices will again be a function of lower commodity and energy prices, a strong USD and softer goods demand, which has all been well documented. Retail Sales are expected to post a headline gain of 0.2% m/m, with a drag from gasoline prices (-4.9% m/m) on sales, expected to be offset by a boost from Auto Sales (up 2.4% m/m), as evidenced by a forecast of -0.1% m/m for the ex-Autos metric, with the core ‘Control Group’ measure also seen up 0.2%. As the attached chart attests, the nominal changes in Retail Sales offer a deceptive picture, with inflation adjusted sales increasing at a modest pace in 2022, as consumers switch back to increased spending on Services, which are not captured in Retail Sales outside of Restaurant sales. Michigan Sentiment is expected to remain very depressed and barely changed at 58.8 (Sep 68.6) for a second month, after recovering somewhat from the record lows of June and July. The risks are somewhat skewed to the downside of the consensus given the pick-up in gasoline prices and sky-rocketing mortgage rates.

Also worth noting is the huge spike in US equities.

Helmholtz 12:05

Helmholtz 12:05Hat tip to Bruce – that was my next comment

I liked the piece from Catherine Wood that you highlighted on Wednesday – there are lots of cross currents in the inflation universe and things can change very quickly.

The potential for policy mistakes is huge.

Just looking at the UK we seem to have gone from tens of billions of fiscal easing last weekend to potential tightening this weekend….

Izabella Kaminska 12:06The Bitcoiners tend to be big fans of Cathie.

Although her fund has had an absolute nightmare.

She’s obviously in the paradigm shift space…

This segways nicely to the fact that I was also joined on the panel by Wei Li, the global chief investment strategist at Blackrock.

She wouldn’t be drawn on the topic of LDI…

Instead, she was keen to focus on the idea of a market regime change that we are going to be experiencing.

She’s underweight equities actually.

Both Kyrklund and Wei Li seemed to agree that the regime change meant adding “security” to the ESG umbrella, but when pushed on whether all the government intervention was compromising laissez-faire, they said it wasn’t.

This is just a new flavour of capitalism focused on being more inclusive and focused on addressing the areas pure laissez-faire could not address.

I have to say, for me, having just started the new Adam Curtis opus Traumazone last night, it really does feel very perestroika. But Western edition.

Are you a fan of Adam Curtis Helmholtz?

Helmholtz 12:09I am – loved his earlier films.

Izabella Kaminska 12:09We were lucky enough to host Adam at the FTAV Vaudeville show in 2019. And I think it is striking that so far, this is a voiceover-lacking series!!

Which feels all wrong.

But I’m only on the third episode. Excellent opening shots of the Ms. Polonia pageant in the 1980s… that’s all I will say.

Going back to LDI though…

I didn’t appreciate until after the conference that one of the issues is not just the leverage, as you have very well explained earlier this week, but the fact that the cash freed through derivatives (which obviously only need to be margin funded) was then reallocated into the investment of OTHER assets.

For some reason, this had not quite resonated until now.

That’s the contagion concern, right?

Helmholtz 12:11Yes – that’s where the issue becomes that the PFs have to sell these (less liquid) assets to fund LDI margin calls.

Izabella Kaminska 12:11I saw an estimate yesterday that we are looking somewhere in the order of a £200bn exposure for the pension funds. Can this be right???

Helmholtz 12:12Yes, it can.

This is why the BoE made the collateral schedule so flexible earlier this week.

To take account of these assets.

I don’t think we get the details of what was posted until next month, but it’ll be an interesting piece of hindsight information.

Roger – the leverage is both in the cash and NOT invested in gilts

And the leverage inherent in the LDI instruments themselves

Izabella Kaminska 12:13Can you catch me up on what happened this week with the BoE?

Helmholtz 12:14The Bank announced three measures on Monday – the link is here:

- A potential increase in the size of the daily auctions to purchase gilts (up to 10bn per day) – in fact the actual volume was much smaller (I think total is still less than 10bn)

- A Temporary Expanded Collateral Repo Facility (TECRF) – a short term funding facility that accepts a much wider range of collateral

This is the one targeted to the PF assets mentioned above.

- An increase in the regular Indexed Long Term Repo operations to banks (which intermediate the flows from LDI funds).

Hats off to the BoE – their actions do seem to have smoothed the transfer of risk.

Izabella Kaminska 12:15Yeah hats off.

Though CNBC seems to think today is the moment of truth.

ARGHHHARHRHHRHR

- The central bank announced the two-week intervention in the long-dated bond market on Sep. 28, having been informed that a number of liability-driven investment (LDI) funds — held by pension schemes — were hours from collapse.

- Finance Minister Kwasi Kwarteng will now deliver an updated medium-term fiscal plan on Oct. 31, the same day the Bank of England has earmarked to commence selling gilts as part of its wider monetary tightening efforts.

- Kwarteng cut short a visit to the International Monetary Fund in Washington Thursday, flying back to the U.K. as the government convened to address the country’s economic crisis.

But you seem to think this is now just a process or might there still be a wobble?

Helmholtz 12:16Well, the price action today is very positive so it seems that Armageddon has been avoided…or postponed to Halloween!

Izabella Kaminska 12:16Yep, just in time.

This was the CNBC link FYI

Meanwhile, there are noises about the ECB starting its QE unwinds in Q2.

That seems very far away no?

Helmholtz 12:18It is. Seems like the ECB is talking to calm market sentiment but who knows where we will be in six months.

I guess they learned from KK’s messaging?

Izabella Kaminska 12:18@john – that baillie gifford thing is from Feb right?

I heard they weren’t too bad. Not exposed in any direct investment way to LDI at least, but only because of outflows to post more collateral. Tho that’s kind of the same thing I guess that we’ve already been hearing about.

Helmholtz 12:20Graham – yes. I have to check, but I think they postponed details of the collateral posted until next month. It is a wide schedule.

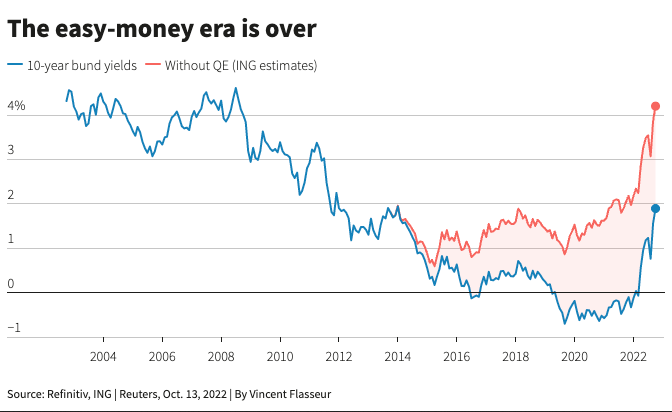

Izabella Kaminska 12:20Here’s an interesting chart from ING (h/t Marc)

Helmholtz 12:20

Helmholtz 12:20And that’s nominal yields – the move in real yields is even more striking (particularly in the UK).

Izabella Kaminska 12:21Yeah. I’m still of the opinion that Germany is the one we really need to be paying attention to.

Helmholtz 12:21@colin – I think that is really a LDI effect

I have seen estimates of up to £ 1.5 tn IL exposure was held by pension funds in LDI format

Izabella Kaminska 12:22wow.

good insight

Speaking of which

The standwithGBP campaign is still ongoing here.

Though it’s been a choppy few days for the Pound on the back of expectations that Liz will roll back the unfunded section of the mini-budget.

Though here’s something even more extraordinary. A really rare sighting…

A ‘sterling and gilts rally’ story in the FT.

And what about the yen? It just keeps weakening:

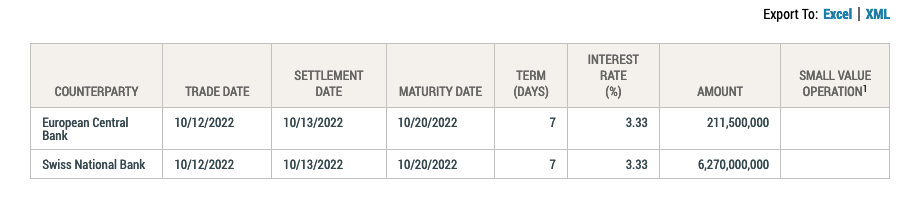

Meanwhile, the US dollar swap line use by the SNB keeps getting larger:

I don’t know if you can see that but we are on 6,270,000,000

Credit Suisse is the likely suspect in need of dollar liquidity. And it does seem the bank is in the midst of fire-selling itself.

The latest news is that the bank is considering selling its stake in Madrid-based tech company Allfunds to raise cash, according to the Spanish press.

And Bloomberg reported that Goldman thinks the bank could be facing as much as an $8bn capital shortfall. The concern remains an incapacity to generate capital. Which I think is a theme that extends beyond Credit Suisse.

But CS is definitely first in the firing line it seems.

But I was reminded last week that Credit Suisse also got itself in hot water for securitisating the yachts and other assets of Russian oligarchs to help maintain access to the Russian market.

Is there anything the Swiss won’t securitise?

Helmholtz 12:26Probably have to plead the fifth…

Izabella Kaminska 12:26Gaha

But also, it is now facing a trial on investors’ currency rigging claims. Can the bad news for the bank ever stop?

Helmholtz, what do you make of this story?

Helmholtz 12:27I’ve known a lot of good people who have worked at CS, and it feels to me a bit like the problems in 2007-09 – small out-of-control sections in a big institution result in problems that overwhelm the whole place.

The FX conspiracy accusations are the latest in a series – there were the accusations about price rigging in government bonds, and then SSA bonds; I am sure there are some very silly comments written in these chatrooms, but I wonder how large the actual quantum of loss to the plaintiffs really is.

It’s awful PR though.

Izabella Kaminska 12:27I have to say, I kind of feel for traders these days that they can’t make silly quips in any electronic form.

It can’t be a very nice atmosphere to work in, and you must feel constantly on your guard.

Who really wants to work at a bank these days?

(Tho that’s why the salaries are so enormous now)

Helmholtz 12:28It’s difficult to see how CS survives in its current form; perhaps RBS in 2009 is a good comparison with the SNB protecting the domestic franchise and allowing everything else to go.

Izabella Kaminska 12:28Btw – if you want a good read on bank salaries, I think this is one of my favourite’s by former colleague Tom Hale.

The poor performance of Deutsche Bank shares is often cited as evidence of a failing business model. But this raises a simple question: failing for whom? From the perspective of shareholders (or global capital, as it were), the failure is clear. But from the perspective of staff, the business is providing extremely high returns.

The use of profit as a metric to gauge investment banking performance misses the possibility that businesses of this kind have been somehow captured by their own labour forces, extracting resources that would otherwise flow to shareholders.

Also here’s the FX conspiracy CS link btw

Credit Suisse Group AG was part of a “conspiracy network” focused on rigging the foreign exchange market, a lawyer said in opening arguments in an antitrust suit against the bank.

Christopher Burke, who is representing a group of plaintiff pension funds and other investors, told jurors on Tuesday that Credit Suisse and 15 other banks participated in online chatrooms in which they colluded on spreads for currency pairs from late 2007 through 2013.

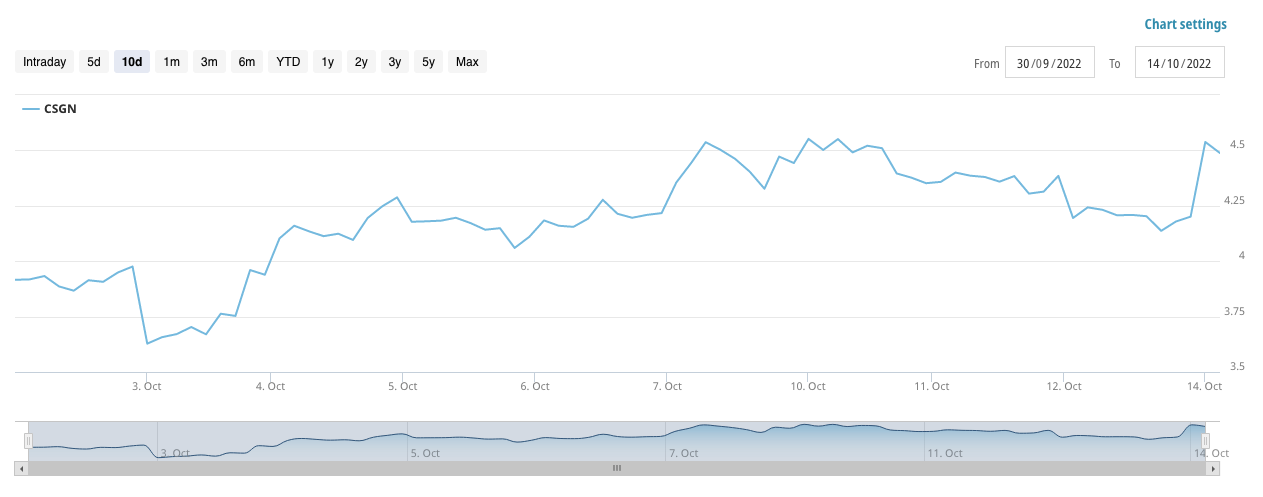

The stock price tho is staying sturdy the last few days:

In other bad bank news, the Italian bank that refuses to die Monte Dei Paschi di Siena is set for a €2.5bn rights issue according to the FT.

Helmholtz 12:31It will never die. It’s a perpetual bank.

Izabella Kaminska 12:32Yep. Like Alitalia is a perpetual airline.

Helmholtz 12:32There’s a theme…

European banks have -and have had since 2008/09 – a structural problem. Too little capital, too many disguised bad loans, too much capacity, and economies that are only growing slowly. Japan 30 years on?

@user007 – but PFs have to consider liabilities as well – it’s the mismatch with assets that’s more important

And that has improved hugely in the last two months

Having said that – the unknown is the inflation exposure mismatch.

So pressure to sell assets that match liabilities will not be huge, and at these levels (nominal and real) many funds may be in a position to look at potential “buyouts”

Izabella Kaminska 12:36@bp it really is. And lol about the years. And even funnier was hearing Tom argue the case very loudly in the FT newsroom that Deutsche Bank was now a communist collective.

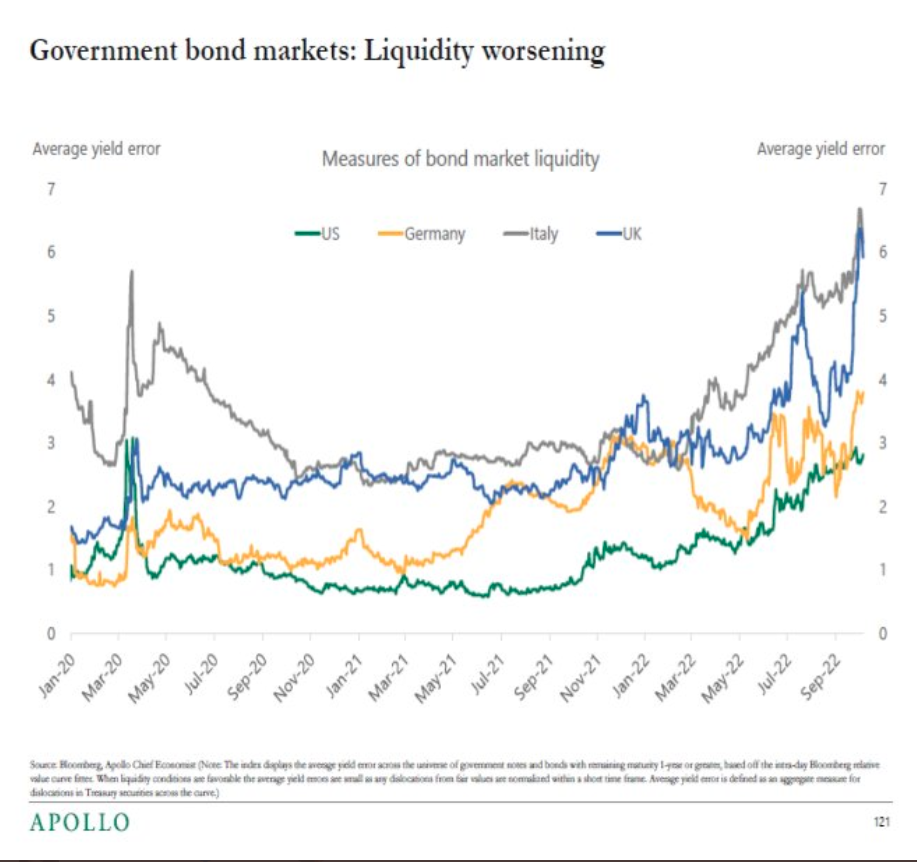

Speaking of liquidity, apparently, Apollo Partners is concerned about it worsening even more in Gov bond markets

Someone stuck this chart Tweet into our Discord today:

This green one seems most interesting though:

Though I’m not sure how they calculate market depth.

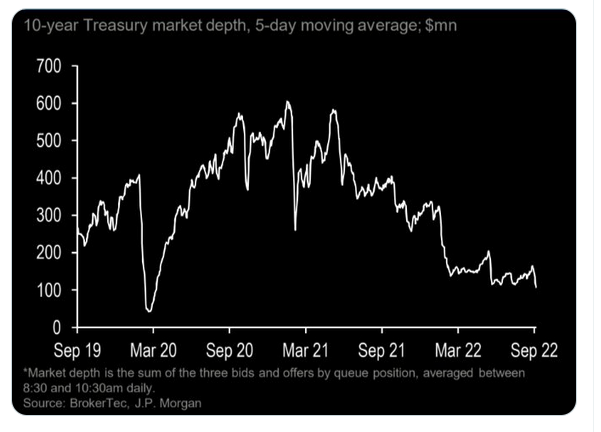

This is the accompanying one for the Treasury market:

I guess it’s an analysis of the market order books?

Helmholtz 12:37Or similar

TBH the analysis of market depth is always a bit in the eye of the beholder.

So very subjective.

For instance, in government bond markets and FX there’s the problem of circular quotes with electronic market systems –

I rely on the quote from trader B who relies on trader C who relies on me…..

Izabella Kaminska 12:39That’s fascinating. Feels like something to look into more deeply.

But let’s change tack

FRENCH FUEL STRIKES

Is anyone going to France for half term?

I mean I know that France loves a strike, but this is getting extreme now.

The striking french oil workers have voted to maintain their industrial action according to BBC today.

I heard from friends in Chamonix, that the shortages have hit them.

Though they’re at least lucky as they can pick up fuel from the other side of Mont Blanc. (As long as it doesn’t get mysteriously closed).

Six out of seven oil refineries are shut.

It again feels very fall of communism to me.

According to the BBC:

Unions want pay increases for their workers, which they say should take account of the huge profits being made at the moment by the oil companies.

They are seeking a 10% pay rise – 7% to cover inflation and 3% for what they call “wealth-sharing”.

The government’s latest move to head off the impact of the action is to requisition key staff at a refinery in Normandy, threatening prosecution unless they allow some lorry tankers to fill up.

They should consider working for Deutsche Bank 😜

Could you imagine bankers ever going on strike?

But looks like Macron is still aiming to have it all sorted within a week.

Meanwhile, French cuisine is at risk because of soaring egg prices apparently:

PARIS (Reuters) – A more than doubling in egg prices in France due to soaring feed and energy costs and a lack of supplies after the worst ever bird flu crisis has prompted some food companies to lower output or change recipes, egg producers said on Wednesday.

Both the European Union and the United States have experienced one of their worst bird flu crises ever this year with tens of millions of poultry culled in each region.

In turn world egg production, which hit 1,500 billion in 2021, was expected to fall for the first time in history this year, following a 4.6% drop in the United States, a 3% decline in the EU and an 8% slump in France, the bloc’s largest egg producer, French industry group CNPO said.

Noted on Kwarteng, but I feel firing him would be a bit self-sabotage for Liz. [Jeremy Hunt has since been appointed]

Also, there’s just been so much turning and flip-flopping. We need a backbone somewhere no?

Helmholtz 12:45Agree with that; I’m not clear that firing KK does anything more than increase the confusion.

Izabella Kaminska 12:45Imagine if Gorbachev had resigned at the first factory strike after announcing Perestroika.

Helmholtz 12:45So who does she pick now? J R-M ?

Izabella Kaminska 12:45Who is left?

We are going to end with Jacob Rees Mogg as the chancellor at this rate.

Anyway… in other slightly exclusive news.

I have a little medium scoopette on ███████. The below is going around as something that ███████team is ██████████ out there via ██████████for ██████████ for the ███████ deal.

Apparently, that’s making a few people giggle. It is legit, even tho people, at first sight, didn’t think it was.

I like additional notes especially.

███████ Russell Brand show soon.

But yeah, looks like it could be one to watch. Russell did drop into one of his other broadcasts that there is a chance (or speculation at least) that Elon might also look to merge in the alternative to YouTube, Rumble, into his new Twitter empire.

Russell had a video de-platformed from YouTube and is now prioritising content on Rumble as a result.

I think that’s about it though… anything else caught your eye?

We’ve got 10 mins left, and I’ve just spotted a bunch of flashes from Wells Fargo and JP Morgan

Izabella Kaminska 12:53

Izabella Kaminska 12:53Here’s a bunch of flashes

So yeah, in 5 mins we have Truss, announcing that the Lady is Definitely For Turning

Quick housekeeping note, I am away for a LBMA gold conference on Monday and Anjuli has half-term duties, so we are moving the session to Wednesday.

On that note, I think we will shut up shop 5 mins early, as I have to go meet another liquidity expert for my Leaked Lunch podcast. It should be a good one.

A mutual acquaintance of mine and Helmholtz

Wish me luck.

Helmholtz 12:56Enjoy !

Izabella Kaminska 12:56Thanks Helmholtz

Everyone have a nice weekend

Bye all!

To sign up click here, though you will have to be a subscriber.