Good morning, Aloha and greetings, fellow market wizards

After the biblical downpours here of Storm Ciaran in the last few days and Izzy’s re-emergence, blinking like a mole in the sunlight, from the Arc Forum, there’s a post-diluvian feel to things here this morning,

Especially so since the main focus of markets of this week, is the onehelluva job central banks have on their hands dealing with the problems their excess liquidity operations engendered over the past decade.

To steer us through these turbid, turgid waters, the captain of our lifeboat this morning is Dario, physically seated overlooking the straits of Gibraltar and the Pillars of Hercules, but figuratively he’s in the lifeboat with us, pumping out the bilge as if his life depended on it.

Good morning, Dario

I gather we are riding a little low in our saddle?

Good morning Julian, and yes the day of all saints hit rather hard. As did the copious amounts of Pesquera red and Iberian ‘secret’

good golly, Iberian secret?

It’s the best part of the pork by far. Extremely fatty and dissolves in your mouth. Eaten well-cooked

Ah, not a drink then. so it seems we are taking in turns to be crapulous

His shipmate this morning, Captain Hardy to his Lord Nelson, is feeling considerably perkier than yesterday after an evening spent watching Everton beat Burnley in the Carabao Cup while clearing the backlog of ironing which had built up in the last fortnight.

No drinking took place.

Which meant I was able to stay up late and watch proceedings over the pond

No surprises from the Fed – which with central bankers is a characteristic to be applauded – but two significant developments during yesterday’s activity:

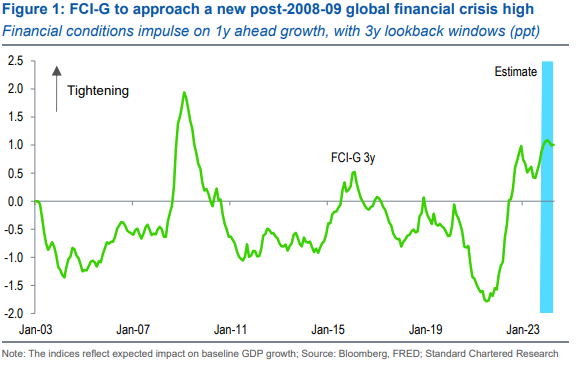

First, for the first time, Powell introduced a reference to the financial conditions and clearly, he hoped these will do the heavy lifting for him and slow economic momentum

Very apt

StanChart: ‘According to our estimate, if current asset prices persist, the baseline FCI-G could rise above the late 2022 peak by end-2023, taking close to 1.1ppt off baseline GDP growth in the year ahead.’

So FCI doing the Fed’s job. And second, and perhaps more importantly, longer-dated bonds rallied yesterday after the Treasury Dept announced its issuance plans for the next quarter

In a nutshell, it’s less than the mkt feared. To boot, ‘the Treasury anticipates that one additional quarter of increases to coupon auction sizes will probably be needed beyond the increases announced today.’

The Treasury released this official picture outlining its plans for issuances:

Can’t tell if that’s Yellen or Ann Widdecombe

Anyway, the treasury probably has one more quarter of outstanding issuance before they start to reduce it.

Darren – my thoughts on that JPM strategy piece’s thoughts on other sectors being good

@darren – some mob down in Florida apparently want to buy Everton but if they live in Miami they are in for one hell of a shock when they drive down Scotty Road in Liverpool and have a bunch of Scallies eye their car up

A subsidiary point on Everton… everyone knows Moshiri is the bag-carrier for Usmanov whose empire is under pressure due to sanctions so I think Moshiri is a forced seller.

Back to markets, though, the conclusion from last night is clear, though, volatility on the long bond is set to remain elevated

Great chart from BAML illustrating how investors are prepared to buy treasury bills and notes but are not comfortable with extending duration.

Why?

The US is running an 8% budget deficit with nominal growth in excess of that and interest payments on $33trn of nat’l debt is now $1trn a year. Risk markets are punishing the govt for its fiscal indiscipline.

The Fed, BoE and the ECB may be on hold but the Chinese are not.

First came the highly-publicised visit from President Xi to the

PBOC last week, the first of its kind since he became Dictator-For-Life.

(every time I think of Xi the tune to ‘All That Xi Wants’ goes through my head)

He didn’t bother to explain his motivations to 1.3bn Chinese but almost certainly it related to the coordination of fiscal stimulus.

A few days later, PBOC announced its biggest adjustment to the national budget in years, along with a plan to issue 1 trillion yuan (~140bn USD) in government

After a spike in interest rates Monday, the PBOC is likely to inject additional liquidity into money markets.

Last week alone, the central bank injected a record net amount 1.96 trillion yuan (equivalent to $268 billion) in short-term cash into the financial system, according to Bloomberg.

@Sarren – safety is in numbers. well, some numbers but not $33Trillion

BOE moment in the spotlight at lunchtime

Andrew Bailey , an alumnus of my college – have I told you this before? I’ve a feeling I’ve said everything before (other notables include Stephen Fry (we shared the same bed but 6 yrs apart – say nothing) Erasmus and erm, Suella Braverman) expected to persist with the Table Mountain approach this morning.

Has anyone ever put Suella and Erasmus in the same sentence before?A brief word on Shell…

Shell

The share price responded alacritously to the results this morning, and the announced share buyback of another $3.5bn. Another reminder that the FTSE may yield 6% in 2024 with a third of that return emanating from divs Stock + 14% ytd as energy sector has driven FTSE performance.

More than enough to drive Greta crazy.

a tiny bit of housekeeping

AAPL results out later, WeWork (a parable about how nominative determinism sometimes operates ironically) and Novo Nordisk surging after 3Q results boosted by its diet and anti-obesity drugs (see Izzy’s recent piece in the Blind Spot re: Ozempic0

and now after I have worked brilliantly in the shallows, we shall turn towards Dario who will not demonstrate Deep Water greatness

we’re back on AI again

(am I already controlled by AI?)

Sink or swim? I prefer to swim and sink

Following on from the discussion about AI yesterday – (I use the word ’discussion’ guardedly because given my physical frailty yesterday I contributed very little apart from a few grunts) much of what was mooted in this parish was echoed in a piece by Deutsche entitled ‘Have markets priced in AI?’

Its conclusions piddled on the sector’s popcorn somewhat by stating unambiguously ‘…several factors suggest that AI optimism has not been the key driver of tech markets across asset classes’

‘Non-AI factors have since driven the performance of tech stocks. In particular, rising real yields have been the narrative since the summer.’

Moves across tech stocks became more synchronized as well. While, early on, ChatGPT propelled semiconductor stocks and left the software industry firms behind, now, various industries across the TMT sector seem to be converging. That points to a waning effect on markets of generative AI and indicates investors are refocusing on non-AI factors in their stock decisions’

I liked that read, and it’s always interesting to see a maybe slightly counter-narrative take on the impact of AI on valuations by Deutsche

But I couldn’t help but notice that it seemed the analysts had focused more on the use of the word “AI”, such as deriving results from transcript analyses in corporate boardrooms, and in disclosures from tech and non-tech companies, rather than investigating the impact of the technology itself

@johndc77 – nefarious crowd

Nothing wrong with that – we’re still in the very early days

Just be wary you can’t really get super deep, intrinsic analysis when sector knowledge of AI (even Inside tech) is neither deep nor intrinsic

DB opines corporates talk about AI and ChatGPT a lot but investors aren’t convinced and share prices don’t really react to the patter.

‘It also appears that credit issuance in the technology sector has not received a substantial boost from AI tailwinds’

Another interesting finding in the report is that companies which discussed AI the most in corporate transcripts tended to underperform the market

Makes sense – AI – and most tech innovations in non-tech corporates – are often seen as quick ‘hail mary’s’ in boardrooms

You only need to look at the story we covered this Monday on the rise and fall of Babylon, the AI app that promised to revolutionise the NHS

This shows that professional investors and even the founders of tech companies have difficulty recognising the reality behind an AI product offering

My own anecdotal evidence makes this ring true.

Some friends of mine run a successful startup valued at a few dozen $mn.

Good mates to have.

They’re lovely people.

In 2021 – the original pitch to VCs after a round of angels, the angels wanted to guarantee a higher valuation and turned to these guys and innocently asked “Hey why don’t you guys do something with AI?”

My friends panicked. As you would, three days before the pitch with 0 AI knowledge

So my friend whipped up a quick algorithm that could track customer sales and pared this info with wider market intelligence gathering. The algo would machine learn – optimising its data output by being fed real-time (and historic) sales data

Quickly labelled an AI that would predict future consumer trends, everyone relaxed.

The AI feature was plopped into the PowerPoint and explained to the VCs

Everyone went uhmmm and ahmmm…

‘Plopped’?

A cute word for saying “dropped in”

That’s onomatopoeic

The feature was promptly dropped a week afterwards.

But it played no small role in their initial success

What this tells me is that companies which underperform, or which feel at risk of underperforming, are more likely to discuss AI than those which aren’t underperforming.

And – hello Shopify.

Venture capital is the best way to gain pure-play exposure to AI.

Graham – like everything in life, the real benefits will be marginal, nuanced, and fit-for-purpose

That doesnt’ mean they can’t be huge. They’ll just be subtle

Last point on AI from DB:

While the overall backdrop for VC remains subdued, a number of deals done over the summer at hefty valuations show that investors were excited about venture opportunities in AI. Nevertheless, a lack of monetisation and big tech’s proactive role is among the headwinds that have started to weigh on VC activity and optimism.’

You may very well point out that ‘Spot Markets Live’ could be written by ChatGPT

(I’m very insecure and assume everyone thinks this)

this is why I always try to write in such a way as to make the next word very difficult to predict.

Beer

belly

bum.

But pure-play AI companies aren’t safe from the overplayed AI hype either

Several startups have reached eye-popping valuations since the rise of ChatGPT

These are the GPT “wrappers”

Not to be confused with rappers

They’re both clothed in gold, however, as these companies that simply ‘wrap’ their features around a core product like ChatGPT have skyrocketed in valuations

They tweak this core product to produce an output not easily extractable from the normal ChatGPT, for instance

For example, ChatGPT could not interact with PDFs. So companies like ChatOCR, which used ChatGPT to read PDFs, scans and handwriting, rose up fast.

@Harvey – if I knew how to access ChatGPT I’d tell you

And what happened now that ChatGPT just integrated PDF functionality? Well, ChatOCR is dead, along with all their investors. That’s what.

I’m starting to feel like I did in the last few years of my time in the City: an analogue broker in a digital world.

And looking at the insane valuations of other AI “wrappers” like Jasper AI – which is valued at ONE POINT FIVE BILLION

And they basically just curate ChatGPT for enterprise marketing teams

So think about it this way Julian

These “wrappers” are essentially User Interface companies.

They are effectively a reception desk for AI users, hosting a very experienced receptionist.

What happens when the AI behind the desk no longer needs the receptionist? Lots of dumb money will be lost.

@darren – I don’t have enough context to determine who Julian Rimmer is either

Lol

We speak a lot about the fragmenting multipolar world these days – as well as the concept of friend-shoring.

But I have another twist on this concept.

The usual idea is that “connector economies” like Vietnam, Poland, Mexico, Morocco and Indonesia, are rising in influence.

There was an excellent piece by Bloomberg on it this week

These are countries that accounted for $4tn in economic output in 2022 owing to their strategic geographic locations, and their ability to facilitate trade.

While only representing 4% of global GDP, they’ve attracted 10% of all greenfield investment since 2017

And the reason is simple

If you’re a Chinese company selling products in the United States, or vice versa, you should be wary of holding your supply chain directly in potential enemy territory – should a war or heightened proxy conflict play out. Instead, you can place your factory in Mexico or Vietnam, for instance.

these were all accelerated beneficiaries of the pandemic and deglobalisation or, more accurately de-Sinofication?

Precisely – and De-Americanisation also

But what’s being lost in this otherwise excellent coverage by Bloomberg is the myopic focus on great powers

(I’m HODLing on for dear life to these topics)

We have to reverse the Henry Kissinger goggles that make everyone turn towards great powers like they’re the most popular high school basketballers

What I see happening is that, if a much too close connection with one or other of the great powers is increasingly burdened with demands, restrictions, and problems, the incentive among non-aligned powers will be to align themselves together.

So essentially, the rise of a new Hanseatic league, hyper globalised edition.

This is high-level geopolitics at play here.

I really believe the traditional idea of open markets and free economies will perhaps live on in a reduced version in this smaller world, as it did during the medieval era

And speaking of connectors, what’s been happening with the global connector (Panama?)

The country has been submerged in protests for two weeks now. I had no idea what was going on. Large numbers of people on my Instagram feed are suddenly Panamanian, and angry about it.

Apparently, it’s Canada’s fault.

What isn’t?

Canada’s First Quantum Minerals operates a local subsidiary called Panana Mining, which employs over 9,000 people in the country and accounts for almost 5% of Panama’s GDP.

Not helping the stock much.

The issue appears to be that the government granted Panama Mining a HUGE concession of 32,000 acres, including a lot of hold on water supplies, for 20 years, with an option to extend another 20.

The deal has raised nationalist and environmentalist anger at a time of significant water scarcity, and over allegations that significant corruption occurred in the obtaining of the deal.

Colour me astonished.

We spoke with a very well-informed local for y’alls benefit

“The problem started with the mining contract but it went deeper. At its core the protests are about the authoritarian nature of the government, which effectively ceded the sovereignty of a large part of Panama over the course of 3 days in a closed room.”

I see what they did there.

Plus, all voting members were of the same party (the governments.) Up to 50% of the country’s land is open to future contracts like this. That’s what’s set this off.”

(Yes they are, Darren – it’s adding fuel to the fire)

So the Panamanian government did what any other government besieged by righteous popular anger did – they called a referendum on the mining concession.

Furthermore, the government has promoted a bill to overrule the law enacting the contract which bans future concessions, and six lawsuits challenging the contract have already been considered by Panama’s top court.

JP Morgan warned that Panama risked losing its investment-grade rating if the contract were revoked.

from one alimentary canal to an elementary canal

this time in Thailand

or

as Donald Tramp referred to it

‘Thighland.’

I saw this story has been doing the rounds again of late

A plan to link the Andaman Sea and the Gulf of Thighland

the plan for a canal might have been adjusted to a land bridge.

Surely that mostly defeats the purpose?

But either way, the Thai govt seems very determined to proceed with a project

yes, the canal makes more sense but I’m no Isambard Kingdom Brunel and have no idea of the difficulties involved in digging a trench across Thighland

if I were I would not be sitting here in my rented suit typing this but would be in the Hotel Whoopee throwing champagne bottles into the swimming pool below

the most obvious opponents of this project would be the Singaporeans…

Whose raison d’etre would be seriously undermined.

Let’s give the globe another spin

And we land on Venezuela!

The United States had decided to be a kind global overlord and relax sanctions on the Venezuelan regime, based on easing tensions between it and its opposition party

Ah… so now Maduro can rest easy and relaxed in his high chair, knowing he somehow made his way out of the imbroglio his predecessor placed Venezuela in

Oh no wait…

Just yesterday, Venezuela’s top court suspended the results of the opposition’s presidential primary election.

Meaning the sanctions could be reimposed. Lol.

Though putting my conspiracist hat on, I would have imagined this move would have been OKAYED by the Americans, tacitly if not explicitly

And remember the Guyana referendum, which Venezuela is conducting and asking its citizens if it should annex the Essequibo region of poor little Guyana, which recently was found to have lots of oil?

The first instance of a rhetorical referendum

Well, Guyana is kicking and spluttering

Calling the referendum “sinister”…

That’s stating the obvious, I think

Euphemism.

“In a statement on Tuesday, the government in Georgetown denounced what it called “Venezuela’s sinister plan for seizing Guyanese territory.”

It said it had sought the ICJ’s “urgent protection” in a request filed Monday for an order for Venezuela “not to proceed” with the plebiscite as is.”

Regardless of this, it’s still looking up for Venezuela.

JPMorgan’s key bond index unit announced yesterday it would put its sovereign bonds and notes of its state oil company PDVSA on an “index watch observation period” for its main emerging market EMBI index until January 31.

That’s quite a remarkable turnaround.

Venezuela currently has like $60bn of international bonds outstanding (both national bonds and PDVSA bonds) which are currently in default

The bank’s investors are split on restoring Venezuela’s market value weight in the index, with some opting for a wait-and-see approach rather than diving straight back in

Considering the ongoing and likely unending conflict between the government and opposition will always be flaring up, I’d say the latter seems wiser (for now)

..and with that, your doughty shipmates on this perilous voyage through the long, dark morning of the soul, strike off with their paddles and an easy rhythm in their canoe and off they go through the backwaters and the bayous of financial waters in search of more adventure.

I’ll be here tomorrow with Izzy, fresh from rubbing shoulder pads with the glitterati and nomenklatura at the Arc Forum…

Tempus tacendi

Bye-bye all!