In the first edition ofThe Blind Spot’s “spotlight” on noble gases I looked at the significant role these rare gases play in a number of critical manufacturing processes, among them in the production of semiconductors and the launching of rockets. I also provided a detailed account of how already tight fundamentals in the markets for helium and neon had been further exacerbated by Russia’s invasion of Ukraine.

In this next instalment of the spotlight series, I follow on from a Bloomberg opinion piece I wrote in May by taking a closer look at the noble gas market structure. This is currently dominated by a handful of clubby players who supply customers on very long-term contract deals.

A rough breakdown of the argument expressed in the Bloomberg piece is that for as long as the market remains opaque, the true state of supply and demand for these gases will be obscured. This will undermine the broader market’s ability to counter or substitute for any unexpected shortfalls smoothly and efficiently, which will in turn increase the global economy’s sensitivity to supply or demand shocks emerging out of this sector.

One way to help build system resilience, however, is to encourage more market transparency through the formation of an active spot market. Given that both Russia and China are key producers of noble gases, it’s arguable that there has never been a better or more urgent time to attempt this.

For now the main tier-one suppliers, companies like Air Liquide, Air Products and Linde, mostly use noble gases as a hook for much wider supplier contracts.

As I noted in the Bloomberg piece:

Would-be competitors and buyers claim that, in many cases, they make agreements on loss-leading terms to capture broader gas supply business, preventing price discovery. What little uncontracted supply exists is currently being quoted at five times the usual rate, says Edelgas’s Cain — a figure confirmed to me by Stefano Marani, the CEO of South Africa-based Renergen, an independent helium and natural gas producer.

In more peaceful and globalised times this sort of practice might at best be considered shrewd business. At worst it might be considered a form of market abuse. In the current environment, however, it also poses a national security risk since the West is more dependent on semiconductors, space access and other impacted industries than ever before.

The good news for those gunning for more transparency is that spot markets often emerge out of exactly such highly charged circumstances.

As I noted in my Bloomberg column:

It was market tightness following the 1979 Iranian revolution that finally skewered the grip of the Seven Sisters cartel — the group of Western oil producers that dominated long-term contracting in the market — and allowed an active oil spot market to emerge.

More recently, the liquefied natural gas (LNG) market opened in the wake of market tightness caused by the 2011 Fukushima disaster and the post-Arab Spring decline in Egyptian gas production. The market has moved gracefully from a “take or pay” type system indexed to oil prices to one in which spot cargoes now dominate, encouraging better price visibility and understanding of supply-side dynamics.

The noble gas market would be wise to follow suit.

A good first step would be for Western governments to call for more transparency from the big companies about how much supply has been hurt by the war, and how much is still being sourced from either disputed territories or those that pose a risk of being sanctioned.

Market participants should also support the development of new platforms that allow them to post bids to woo supply and cover shortages, or urge existing exchanges to support noble gas quotes. The crypto market, for one, is already looking at opportunities in this space. It has convinced Renergen, which is bringing new supply to market from this year onwards, to sell its volumes in tokenized form.

Whatever the path to a spot market, it’s becoming increasingly clear that gases such as neon and helium are too important to be under the thumb of only a few big players. Noble gases should be allowed to float freely on the market.

There are finally inklings of something similar happening in noble gases.

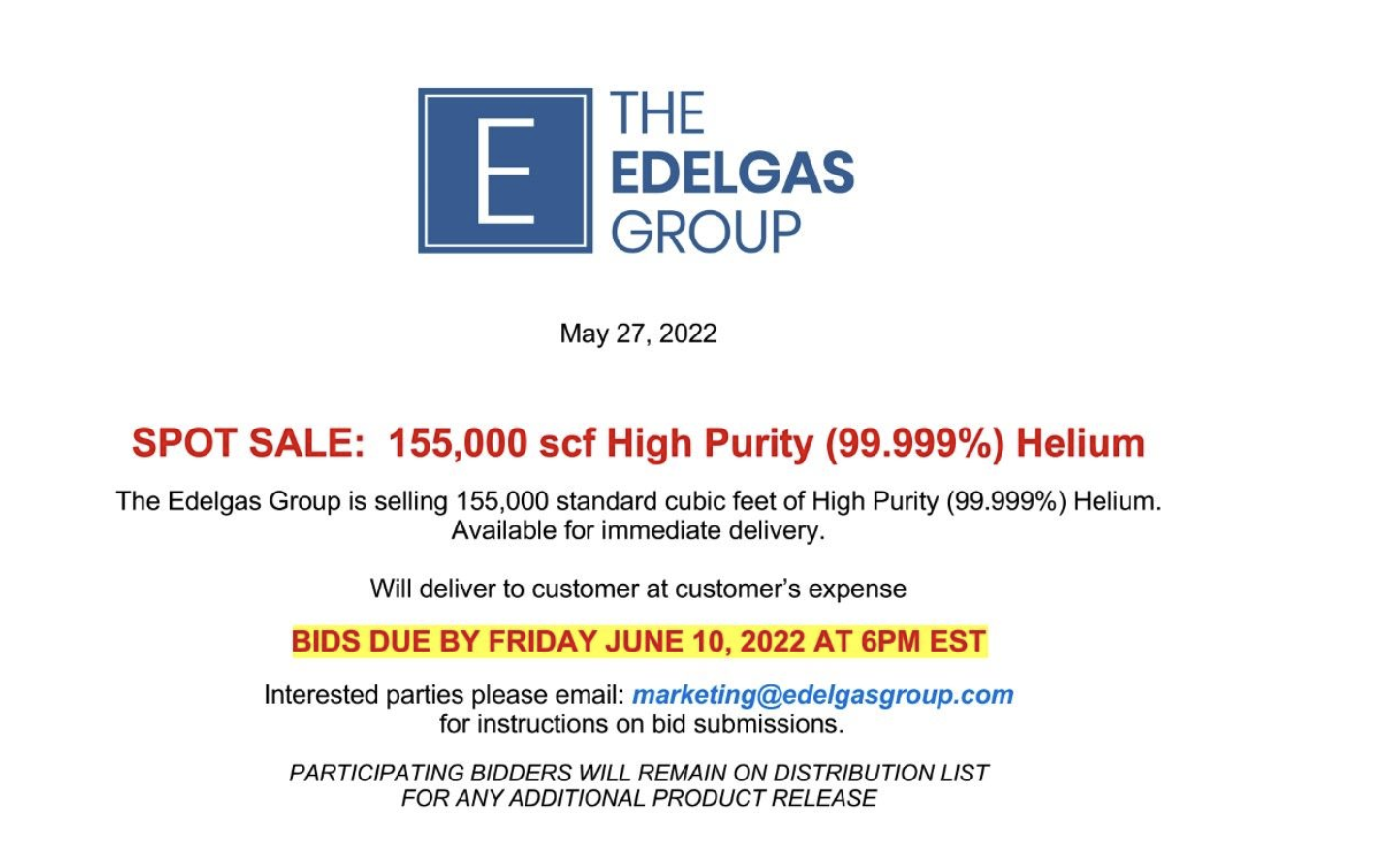

Last week Edelgas, one of the key consultancies in the area that is committed trying to break the market open posted this:

The above is the second offer of its sort, Edelgas’ Cliff Cain tells me. It constitutes a resale of gas from a second-tier intermediary where Edelgas is playing the role of a broker matching the deal.

If the market really is as tight as the buyside claims it is, such offers should become more commonplace. After all, if you are a low-need consumer, or a consumer in a more substitutable sector such as lifting, you might benefit more from reselling your contracted supplies at a higher price to a third party than in utilising them.

In recent weeks, anecdotal evidence that helium is already being substituted for more plentiful gases in the leisure lifting sector (i.e. in the entertainment balloon sector) has also begun to emerge.

As the Daily Mail reported on May 25:

A worried mother has revealed how having floating balloons at a children’s birthday party can lead to disaster – with some decorators allegedly filling them with ‘explosive’ hydrogen to cut costs on helium.

At a quarter of the price of helium, hydrogen appears to be a budget-friendly option for operators looking to improve profit margins or keep costs low for customers.

But it isn’t a safe alternative, and not an industry-wide practice as it is an extremely volatile gas.

It is not clear, of course, if the Daily Mail story truly evokes a wider trend for switching to hydrogen from helium in the balloon sector. The recounted incident could be the result of a single wayward seller. But high prices are certainly bound to be having some sort of influence.

I intend to a make some further inquiries to see just how big a deal this really is. What is certain is that if prices remain at historic highs, it will be the balloon market which will be one of the first to consider substitution or resale.

For now, the tier-one suppliers are talking down the idea of any imminent crisis. Many, nonetheless, are quietly striking deals to develop new facilities, especially in the neon sector. Critics such as Cain say the chances of these plants coming on line within a year are very low. With helium, the situation is more complicated as supply as is dependent on pre-existing LNG facilities and/or natural deposits.

Either way, it’s unlikely the situation is going to get better before it gets worse.

As Reuters reported this week, Russia has now formally decided to initiate sanctions of its own in the sector. From Reuters:

Sanctions-hit Russia has limited exports of noble gases such as neon, a key ingredient for making chips, until the end of 2022 to strengthen its market position, its trade ministry said on Thursday.

Russia’s export curbs could worsen the supply crunch in the global chips market. Ukraine was one of the world’s largest suppliers of noble gases until it suspended production at its plants in the cities of Mariupol and Odesa in March.

As the story continued (TBS emphasis):

The move will provide an opportunity to “rearrange those chains that have now been broken and build new ones,” Deputy Trade Minister Vasily Shpak told Reuters via the ministry’s press service on Thursday.

Russia accounts for 30% of the global supply of three noble gases – neon, krypton and xenon, according to the ministry’s estimate.

Taiwan, the world’s leading producer of chips, imposed curbs on exports of this product to Russia after Moscow sent thousands of troops to Ukraine on Feb. 24.

“We plan to increase our production capacity (of noble gases) in the near future. We believe that we will have an opportunity to be heard in this global chain, and this will give us some competitive advantage if it is necessary to build mutually beneficial negotiations with our colleagues,” Shpak said.

The story strangely fails to mention helium.

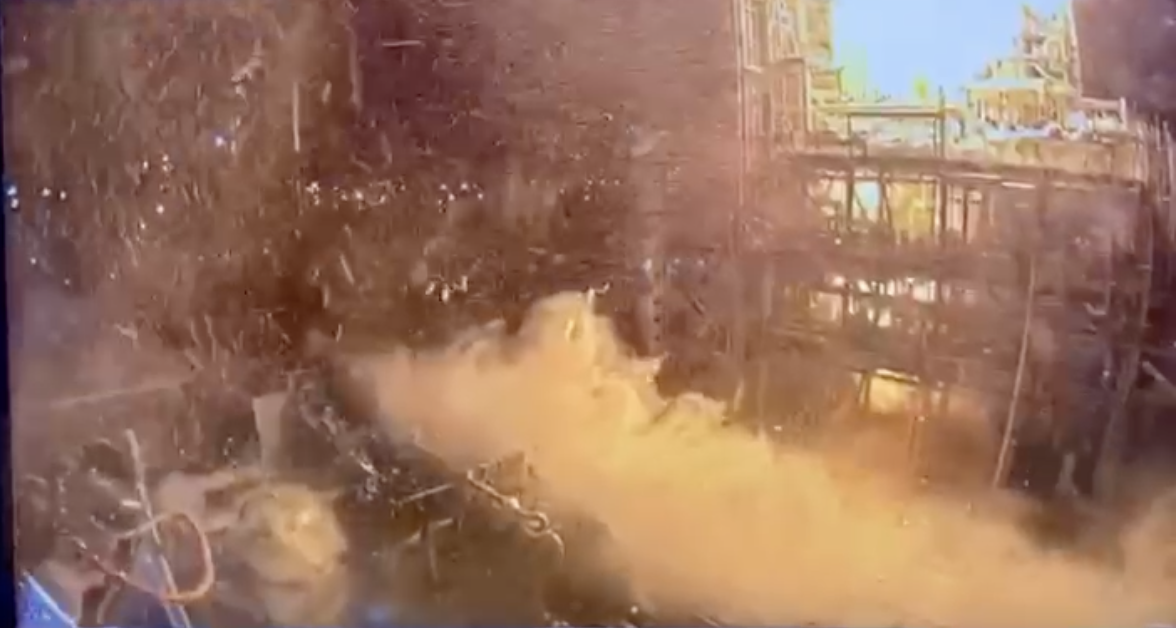

And yet, Russia’s Amur LNG project, being developed by Gazprom, was supposed to be one of the big new source points for the helium market this year. Not only is there now a risk these supplies could be impacted by sanctions, the project itself has been hit by a number of unexpected fires the past year. These, for the most part, have been framed as marginal in nature. But footage shown to us of the January 5 incident (not verified by Gazprom) suggests the incidents were far from marginal. Here are some screenshots of the footage.

What we do know is that Linde, one of the specialist technical suppliers to the project, has since confirmed that it will be exiting Russia and suspending “all business development for new projects in Russia”.

How easy it will be for Gazprom to repair the damage without Linde’s help is anyone’s guess.

A similarly strange fire, however, broke out in Qatar’s LNG facilities that also produce helium a few weeks after the Amur explosion. Qatargas never officially confirmed the fire, but rumours began to circulate around February 18 that a couple of LNG trains had been down for a couple of weeks. Qatargas attributed this down time to scheduled maintenance. But I myself have seen satellite footage showing significant damage to one of its key liquefaction facilities, and the source that showed me the footage was adamant this was evidence of a major incident having occurred at the plant.

Were these fires merely accidents? Industrial sabotage? Or, perhaps, something more strategic?

Had transparent spot markets been in play we might have more insight into the situation. For now we don’t have such transparency. But in current conditions, even small players with marginal barrels can help influence market developments.

This is why some, like Stefano Marani of Renergen, an independent South African natural gas supplier that is bringing its own helium production on line from this year onwards, are betting they can use new market structures, such as those provided by public blockchains, to make a difference.

Renergen is now the backbone of the Argonon token system, currently in pre-sale, which plans to back tokens with freely tradable helium. Marani told The Blind Spot this is why he is investing not just in helium development but in the container systems that can allow helium to be freely transported around the world.

“The purpose of the ArgHe token is to provide democratized access to accessible redemption rights, and thus accessible ownership, of helium through blockchain technology,” reads the white paper.

There’s no doubt that the presence of uncontracted spot supplies available for sale can make a difference here. Whether or not they require a blockchain to be freely traded is another matter.

Blockchain or no blockchain, tier one players will still be able to dominate the market if there aren’t enough marginal barrels or resales coming into the system. They will also continue to dominate if the buyside proves reluctant to give up the security of long-term contracting in exchange for exposure to spot market volatility. Given that legacy contracts* are currently structured in such a way as to encourage incumbent suppliers to match all price improvements from competitors, that may prove a hard habit to break for many purchasers.

At the same time, if the current Ukrainian crisis doesn’t help to open up the market, it’s hard to imagine what will.

*A typical boiler plate contract structure can be found here, courtesy of Edelgas.