Julian Rimmer 10:30

Julian Rimmer 10:30Good morning, aloha and greetings, fellow market wizards

and welcome back our founder, mentor, guide, spiritual guru, wellness adviser etc etc, Izzy Kaminska

Izabella Kaminska 10:31

Izabella Kaminska 10:31Howdy. How’s your week been?

Have you been engaging in any funghi retrieval?

Julian Rimmer 10:31my personal hygiene standards are very high, so no

Izabella Kaminska 10:32Because I have, somewhat unsuccessfully. Terrible pickings at the moment, but hoping for something better than this later today:

Julian Rimmer 10:32actually, we have a few on our back lawn so you are welcome here anytime

Izabella Kaminska 10:32

Apparently (i was told yesterday) in france you can take your pickings to the chemist, and they will tell you which ones are safe and which ones are not.

I just depend on my dad.

Julian Rimmer 10:33unless he hates you in which case

Izabella Kaminska 10:33curtains

Julian Rimmer 10:33It’s been very busy here because there’s so much going on in mkts to discuss, but less so in my other walk of life, the wine shop.

I’m watching a consumer slowdown in real time. I’m the living embodiment of ‘death of the high street’

death ON the high st

Izabella Kaminska 10:34Too many mead inquiries? Tho given by the location of your shop I do think that gives some substance to the claim that this is a “Richsession”, with middle classes and up being hit most of all.

(Mead is very popular in Poland btw)

Julian Rimmer 10:34it’s not popular with me but let’s not go there again

people ask for the strangest things… Himalayan malbec

(long and tortuous investigation, revealed the person had misheard the name of a brand)

it was Amalayan malbec

butterscotch schnapps, a woman with a picture of some obscure local bellywash she’d had on holiday in Benidorm 5 yrs ago. Where could I find it? Answer: probably Benidorm is your best bet

as i said, they ask for the strangest things

you’d be a good wine merchant, Izzy

Izabella Kaminska 10:36Well don;t know about that. Anyway. Looks like market wise we can all relax because….because Uncle Sam will save the day. US GDP has put in a stunner of a show in the third quarter. Here’s ING on yesterday’s number:

Right after an uneventful ECB announcement, US GDP figures beat estimates and confirmed the growth differential between the US and its key developed peers is significantly wide – and widening. As discussed in this analysis by our US economist, the GDP surge to an annualised 4.9% in 3Q was primarily due to consumer and government spending. We don’t expect such strong performance to be repeated in the fourth quarter, where we’re forecasting 1.5% growth. For now, the evidence of the strong growth momentum into the last part of the year is adding fuel to the higher-for-longer rate narrative.

The dollar’s reaction was quite muted: we don’t think this was due to any impact from the ECB, but rather to the 3Q US PCE figures, which came in lower than expected at 2.4%, and potentially jobless claims climbing back to 210k. There is also a building trend for the dollar to find less and less upward momentum after some strong releases. That is consistent with the overbought condition of the greenback and the notion that we might be close to the peak in US activity data optimism. In this sense, we could see data outside of the US (i.e. in the eurozone or in China) having a greater impact on global market dynamics as they have done in the past few weeks.

Julian Rimmer 10:37@johnk – Kew Gardens

wine merchant to the bourgeoisie

Izabella Kaminska 10:38But back to US GDP. Janet Yellen for one made an astounding comment vis a vis this yesterday. Bloomberg had the headline as

Yellen Says Yield Surge Is Due to Strong Economy, Not Deficits

The actual quotes were:

“I don’t think much of that is connected” to the US budget deficit, Yellen said at an event in Bloomberg’s Washington office Thursday. “We’re seeing yields go up in most advanced countries.”

The increase in yields — which has taken benchmark Treasury rates to the highest levels since before the global financial crisis — is instead “largely a reflection of the resilience people are seeing in the economy,” she said.

“The economy is continuing to show tremendous robustness and that suggests that interest rates are likely to stay higher for longer,” she said.

So what do you reckon Julian? Stunning success show? Or Potemkin Village?

Julian Rimmer 10:39Janet Yellen attributing the rise in US yields of late to an economy that is “doing very well” ? Well

as Mandy Rice Davies once pointed out, ‘She would say that, wouldn’t she?’

The death of the US consumer has been predicted many times before. The resilience is astonishing.

The economy’s main growth engine — personal spending — jumped 4%, also the most since 2021.

Izabella Kaminska 10:40But I bet none of them have the raw survival skills that come with mushroom foraging expertise

Julian Rimmer 10:40sometimes, my day job feels like that, rummaging about in the mud for not very much

It’s not just the consumer, though, in the US, 78% of companies reporting beat 3Q consensus, compared with 57% in Europe.

Pasquariello, my GS guy, (although I doubt he describes himself as such) wrote this week about how govt data seemed to be a lot better than corporate data but 3Q results from the S&P have given the latter some impetus and the overall performance of Big Tech largely justified the higher valuations. The crowded trade was crowded for a reason.

big tech delivered

Izabella Kaminska 10:42So is the argument that high yields are a function of high growth potentially accurate here? The problem, I personally think, is that the bang from all the IRA spending is about to knock straight into the reality that the green transition doesn’t gel with ever higher rates.

Julian Rimmer 10:42higher yields are, I suspect, more a function of market trepidation about the extent of issuance next year, (remember that $1.78 TRN figure?) as well as intl buyers

(I’m thinking the Chinese and Russians here) looking to diversify. When DXY turns lower, I expect gold to rip because that’s the direction in whicch they are diversifying

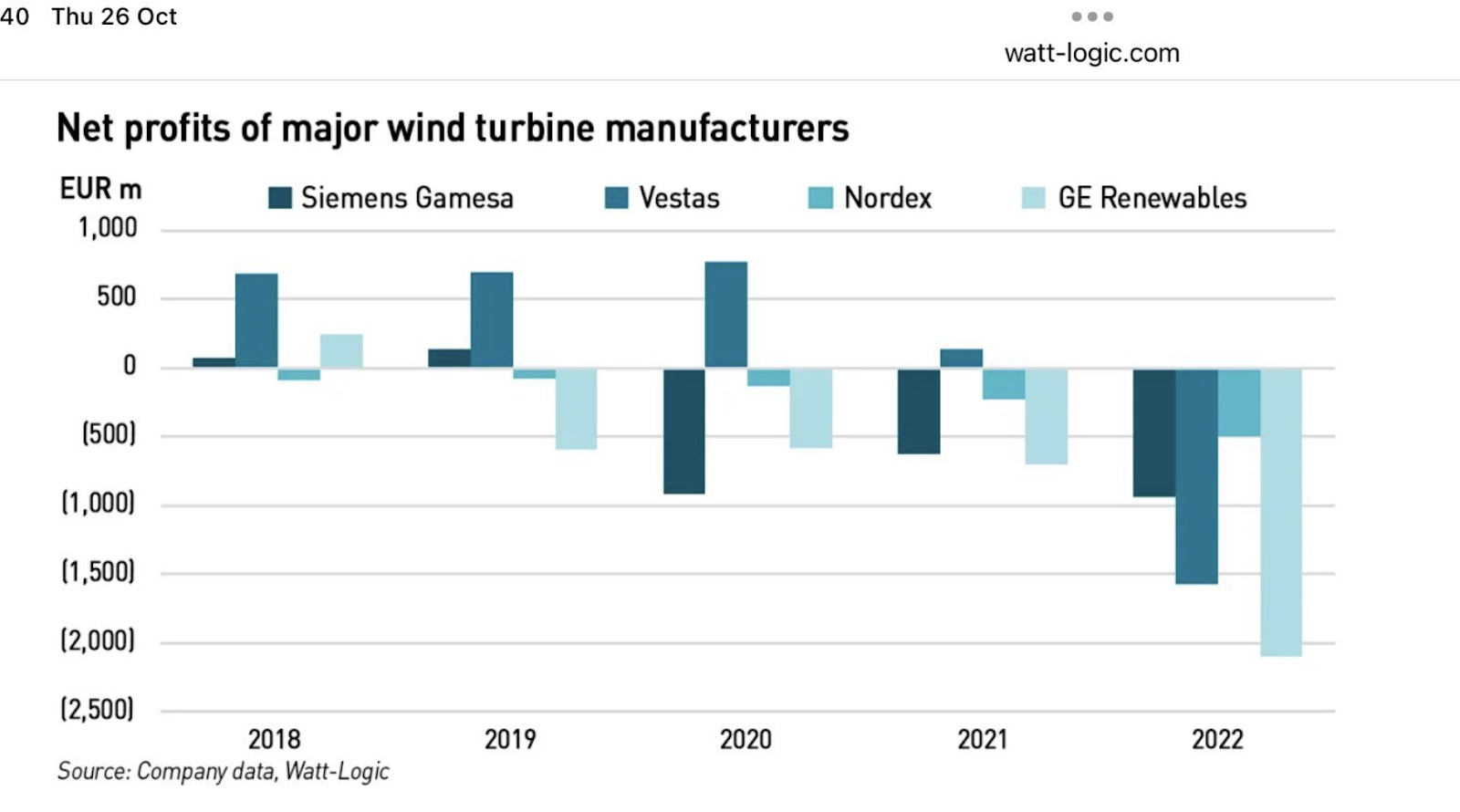

Izabella Kaminska 10:43Did you see Siemens Energy yesterday?

Julian Rimmer 10:43I saw the share price move but lacked the sufficient intellectual curiosity to explore why.

i was searching online for mead

Izabella Kaminska 10:43You’d think Europe’s biggest windfarm producer would have seen its shares perk up in light of all this business from the green transition, but no:

It was down about 35 percent yesterday on news it was now negotiating with the German government for guarantees for its long-term projects.

Julian Rimmer 10:44

Julian Rimmer 10:44that’s not very phlegmatic

Izabella Kaminska 10:44Here’s an interesting chart someone posted in the Blind Spot Discord group about it:

So, I suspect, somebody told some porky pies when they argued that renewable energy was cost-competitive with fossil fuels. If it was, the above shouldn’t be happening.

In reality, many of these long term projects aren’t viable at 5% interest rates. (Which is why some are calling for central banks to introduce a two-tier rate market, with the idea that green projects get cheaper funding on the basis that they will ease supply-side constraints more quickly.)

(Tho JR would know all about this I understand since he has the paperwork to prove his expertise in ESG)

Julian Rimmer 10:45well, while floundering about my career, I started studying for a CFA in ESG

I got 3 modules in, realised the answer to every question is ‘what would Greta say?’

and lost the will to live

I gave up

Izabella Kaminska10:46Apparently, it’s becoming understood that the “S” is now going to stand for “Security”

Julian Rimmer 10:46Wang Yi in the US meeting Blinken, presumably to argue about what Biden and Xi will argue about next month.

The summit next month is very important for both presidents.

botyh of them need to look, well, erm, presidential and successful n stuff

Fentanyl is high on the agenda, apparently. The drug behind the opioid epidemic mostly comes from Mexico which I knew but I didnt realise most of it originates in China.

Izabella Kaminska 10:47Ah, that’s because you don’t read the Blind Spot! Because we’ve been talking about the fentanyl triangle for a long time 🙂

Julian Rimmer 10:48lacking a subscription clearly informs my all-round ignorance all these years

Izabella Kaminska 10:48Here’s just one of a few posts about it ????

(eek, that didn’t link very well)

Julian Rimmer 10:48it wasn’t so much a blind spot as full-on blinkers

Izabella Kaminska 10:49Anyway, let’s expand on that equity point you raised earlier.

I’m going to enforce better compartmentalization for the purposes of a streamlined transcript: DIVIDER

Julian Rimmer 10:49(delete everything I type?)

Izabella Kaminska 10:49No – just an intro to segue into Treasury talk

Julian Rimmer 10:49(ive been streamlined that before)

Izabella Kaminska 10:49so… looks like the equity markets aren’t buying the US growth story. S&P 500 is continuing its downward trend, as is the NASDAQ and the DJIA.

Here’s a good little round up from UBS on the earnings performance to date:

A combination of disappointing mega-cap tech earnings, weaker guidance,

and elevated bond yields has weighted on equities. The decline has been

fairly broad-based with nearly 64% of S&P 500 constituents falling since

last Friday. Since last Friday’s US equity market close, the S&P 500 has fallen

2.1% and the tech-heavy Nasdaq has declined 2.9%. The S&P 500 index

has now dropped by almost 9% since its July peak.

• The average week-to-date move for the “Magnificent Seven”

was –4.9% since last Friday. The “Magnificent Seven” account for

some of the heaviest-weighted constituents within the S&P 500 index,

and their earnings announcements this week have been mixed. Among

these seven constituents, Alphabet posted the largest drop in the S&P

500 (–9.7% week-to-date), as markets responded to its management’s

comments about unpredictable customer spending intentions. Concerns

over similar pressures flowing through to other companies weighed

on many S&P 500 stocks. Meanwhile, reaction to Microsoft’s earnings

release was strong, making it among the top 10 gainers on Wednesday

(+3.1%) following its quarterly report, which showed solid beats, led by

upside to revenues and margins, expense control, market share gains

in its cloud business, and strong bookings. Meta’s earnings were better

than analysts’ expectations, but the stock declined Thursday (–3.7%)

after management guided below analysts’ expectations for 2024. Post

Thursday’s close, Amazon reported an earnings beat, but questions

were raised about the outlook for corporate spending on cloud services,

as well as consumer spending within online stores (–0.5% in after-hours

trading).

On the yield discussion I thought this comment from Mark Haefele and team in the same note was bang on, note the bit I’m emphasizing:

In our view, the outlook for Treasury yields will ultimately depend on the

growth trajectory of the US economy. Much of the momentum behind

the rapid increase in Treasury yields has been due to technical factors that

should abate. Notably, the Federal Reserve’s shift from quantitative easing

to quantitative tightening has removed a significant source of buying,

while issuance is trending higher due to the increasing US budget deficit.

However, if this trend were to persist, we would expect action from the

Fed to preserve financial stability by ensuring the proper functioning of the

Treasury market. As a result, we expect economic fundamentals to reassert

themselves. Regardless of whether the landing is ultimately hard or soft, we

think US and global economic activity will slow and inflation will moderate

over the next year—boosting demand for high-quality bonds.

“Proper functioning of the Treasury market” – clock that?

Julian Rimmer 10:51It’s a great idea. But it will never catch on. Whatever will they think of next?

Markets are still adjusting to higher yields. That’s a process and not an event. After fifteen years of financial repression, it’s no surprise the recalibration of mkts to the repricing of money is a lengthy and turbulent procedure

or chaos

Izabella Kaminska 10:52And yet, looks like markets are also beginning to anticipate the return of the plunge protection team.

Julian Rimmer 10:52@johndc77 – there’s a lot of ignoble rot in my shop

Izabella Kaminska10:53Now, bear with us. Because it’s going to get a little WONKY.

Julian Rimmer 10:53going to? it already was

Izabella Kaminska 10:54The UBS ref seems to me a mind meld with what cbankers are already talking about. And what I would say was already flagged by Standford’s Darrell Duffie at Jackson Hole in August.

The paper of note is this one:

Julian Rimmer 10:54is that the same piece I referenced the other day?

it gets a lot of traffic that piece

Izabella Kaminska 10:54Does it?

oh right our traffic. Lol

Julian Rimmer 10:55twice in 2 days – what are the chances?

Izabella Kaminska 10:55The IT geeks at the KansasFed are probably having palpittations about an incoming denial of service attack. ????

But back to the point. Yes, I’ve talked about this on the Blind Spot a number of times already, but it is in my opinion the first step towards normalising the idea of what will soon become U.S. yield curve control under the guise of a Fed “market-function purchase program”.

Julian Rimmer 10:55denial opf plausibility

Izabella Kaminska10:56For the avoidance of any doubt. I’m going to repeat this very loudly and to the point.

Julian Rimmer 10:56type slowly because i cant read fast

Izabella Kaminska 10:57What we are looking at here is the likely initiation of US YIELD CURVE CONTROL policy.

Got it?

Here’s the key passage:

After investigating these implications, I discuss improvements in Treasury market structure and other measures that could increase the market’s intermediation capacity under stress. These include broader central clearing, all-to-all trade, post-trade transaction reporting, substituting the Supplementary Leverage Ratio rule with higher risk-based capital requirements, and official-sector market-function purchase programs.

It’s worth noting that Sweden’s Riksbank this week announced its intention to provide greater overnight liquidity access to CCPs. (kind of related, as they are having a really tought time at the moment.)

Julian Rimmer 10:57CCPs?

chinese communist parties?

Izabella Kaminska10:58Not the chinese variety

Central Counterparties

Julian Rimmer10:58ah so

Izabella Kaminska 10:59(And RIksbank also has announced this week that it will need some ridiculous amount of taxpayer money to plug its balance sheet hoel. But that’s another story)

But going back to the “market-function purchase program” specifically, Duffie cites a lot of other relevant work to support the argument that sometimes you have to do de facto QE even when rates are supposed to be going up.

And there is a precedent from 2020 as the below Fed paper points out (while admitting this turned in QE):

The most striking aspects of the market functioning purchases were their innovativeness

and their unprecedented speed and scale. In terms of speed and scale, the purchases quickly

reached over $100 billion per day and totaled over $2 trillion between March 13 and April 30 alone.

In terms of innovativeness, the Fed varied the pace and distribution of purchases based on

observable measures of market functioning, reflecting the particular motivation for the purchases.

It also adjusted the settlement timing of some MBS operations, allowing market participants to

quickly obtain cash for their MBS sales, reducing funding pressures in the market. The Fed also for

the first time purchased agency commercial mortgage-backed securities (CMBS) to support the

smooth functioning of this important market (Park, Gouny, and Liu, 2020).

Julian Rimmer 10:59that will go viral, for sure

Izabella Kaminska 11:00Here’s hoping!

There’s also Duffie’s original paper on it all here where he introduces the idea of fiscal buybacks:

Talk about quasi fiscal operating norms being established!

Julian Rimmer 11:00you speak fluent banker

Izabella Kaminska 11:01It’s a curse. Trust me.

Anyway here he explains why “Market-function purchases” aren’t the same as QE. (Got it, DEFINITELY NOT QE)

Julian Rimmer 11:01roger

nothing like it at all

Izabella Kaminska 11:01While highly over-simplified for illustrative purposes, this example motivates the role

of market-function purchases, as distinct from quantitative easing. Even if dealers have

the capacity to keep markets relatively liquid, the market for government securities can

nevertheless be destabilized by fire sales.11 Many ultimate buyers may be unable or

reluctant to commit large amounts of capital on short notice. Price impacts could be

large enough to cause a further unwinding of levered positions, potentially leading to

an adverse feedback loop. As we have discussed, this seems to be roughly what

happened in the UK gilt market in late September 2022, when the Bank of England’s gilt

purchases stabilized the market.

And:

Julian Rimmer 11:01oh, yes, it’s exactly the same

Izabella Kaminska 11:02“An expectation of official-sector support for government securities markets under stress

could induce some investors to take additional leverage in normal times or could

reduce the impetus to improve the structural resilience of the market for government

securities.

And here’s how it connects to YCC:

Julian Rimmer 11:02ycc? young chinese communissts?

Izabella Kaminska 11:02Yield curve control Julian!

Julian Rimmer 11:02ok, i’ve got this

Izabella Kaminska 11:02When in doubt, always assume it’s a communist acronym 🙂

To implement open-market purchase operations, many central banks and fiscal

authorities conduct reverse auctions of a specified total quantity of a given security or

some specified sector of securities. In some jurisdictions, trades are negotiated

bilaterally with dealers. For example, with the ECB’s Pandemic Purchase Program, most

purchases were conducted bilaterally with dealers. In a reverse auction, purchases are

awarded to those bidders offering to sell at the highest yields (lowest prices). This

quantity-based auction approach has been used in the Fed’s Large-Scale Asset Purchase

(LSAP) programs and in its purchases of Treasuries in response to the situation in

March-April 2020. In an alternative price-based approach, a yield is announced and

designated market participants are given the right to sell at that yield. This can be done

on a full-allotment basis, as with “yield curve control,” which is the approach taken in

March 2020 by the Reserve Bank of Australia “to address market dislocations. The

Bank of Japan has conducted yield-curve control on a routine basis.

Which is another way of saying we will buy the securities from the dealers willing to accept the lowest bid first and fill the trade upwards from there. Or, we will announce our target yield and give everyone the chance to be filled at that rate

Julian Rimmer 11:03and what about the fiscal dimension?

Izabella Kaminska 11:04And here’s the fiscal argument. Basically, Duffie argues in some circumstances it makes more sense for these sorts of “market-function” purchases to be conducted on the fiscal account rather than the central bank balance sheet, to help preserve the notion of central bank independence. A fiscal authority could alternatively indemnify the purchases against potential losses:

Julian Rimmer 11:04not the physical dimension

Izabella Kaminska 11:04(no Olivia Newton John here!)

Related to the approach of having market-function purchases conducted directly on the fiscal account, a central bank can be indemnified by the fiscal authorities for the associated gains and losses. For example, when the Bank of England purchased gilts to

address severe market disruptions in September 2022,42 it was explicitly indemnified in advance by the UK government for the associated gains and losses, with the stated intent of supporting the independence of the central bank.

Indemnification, however, implies a degree of coordination between the fiscal and monetary authorities that could,

in some jurisdictions, cut against independence of the central bank. In the end, it may be difficult to avoid some degree of coordination. Whether or not indemnification by a

fiscal authority of market-function purchases by the central bank is useful or reliable may vary across jurisdictions. Tucker (2018) writes that “a degree of explicit cooperation and coordination is unavoidable if overall policy is to be coherent,” and

“Suspicions are more readily assuaged if the need for coordination with government has been countenanced and telegraphed in advance.” In some jurisdictions, indemnification related to asset purchases is implicit because profits and losses from central bank operations are remunerated to the fiscal account.”

Sorry for all the block quotes but they’re important for the sake of historical archive!

@helmholtz – yeah i suspect so

Heavy stuff right? But it all comes down to potato potataho type logic. When is QE not QE, and when is a cbank really independent and when is it not? There’s way more i can say about this, but i will leave it for blind spot newsletter. Or maybe do some sort of voice note.

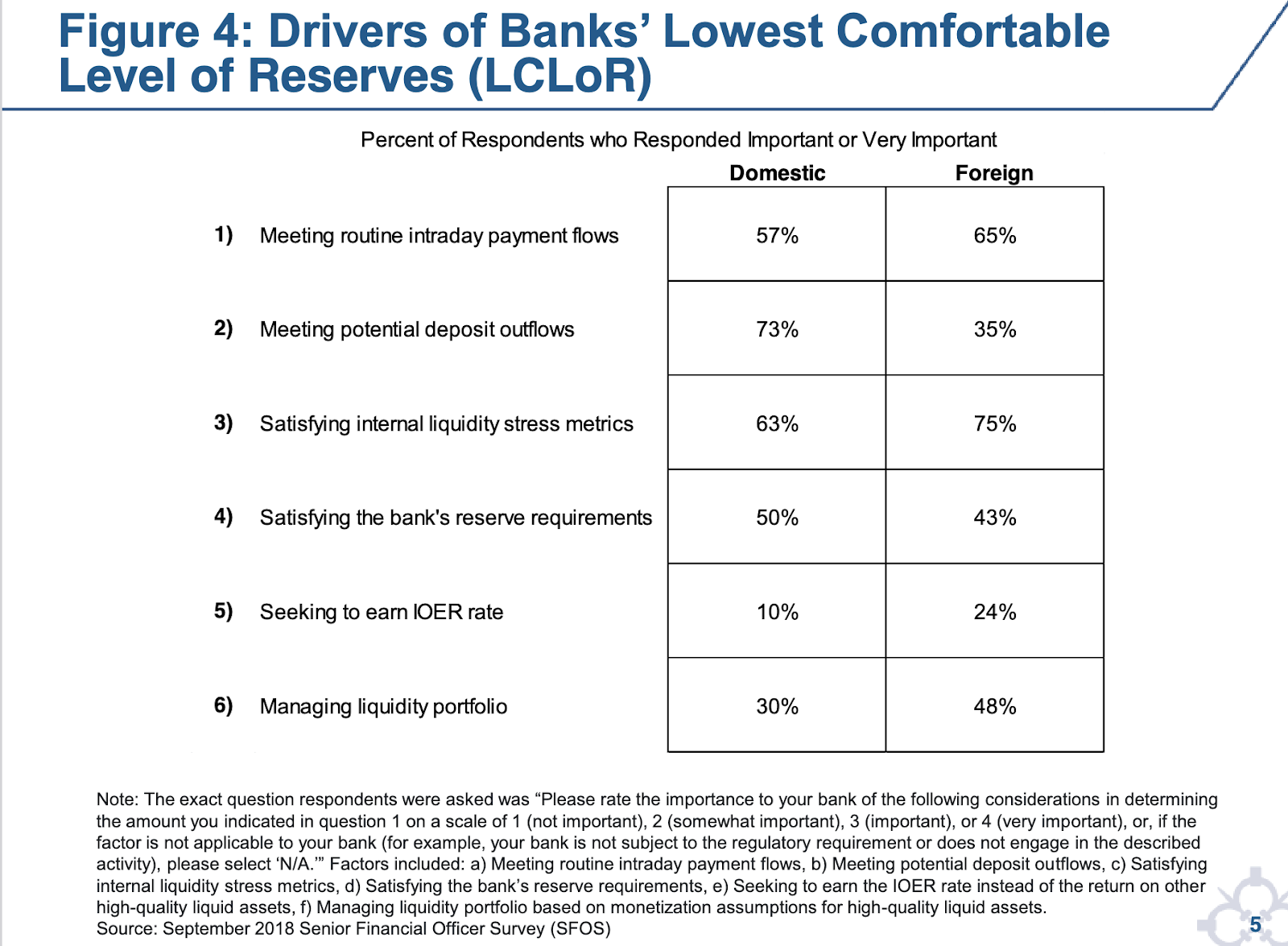

There are at least three other key connected themes that are worth signposting (but which we won’t have time to go into today). The first is the question of LCLoR and have we reached it yet.

Julian Rimmer 11:05What’s LCLoR? Sounds like a zoomer acronym for some kind of comedic response

(am i with dario or Izzy here?)

Izabella Kaminska 11:05Lowest Comfortable Level of Reserves which was the threshold that was penetrated in September 2019 and which caused the successive repo market flip out.

Julian Rimmer 11:06ah yes, we sort of mentioned this yesterday

Izabella Kaminska 11:06(yes, cough cough)

Anyway there’s a good chance we’re approaching it now. And this, by the way, is why Im so obsessed with intraday liquidity and payments gridlocks and the return of Herstatt Risk. You can read about the Fed’s conclusions about what happened here:

As you can see here, intraday liquidity for managing payments is today a major driver of demand for a Lowest Comfortable Level of Reserves:

Which is a good point to bring in the ECB. Which has arguably been performing “Market-function purchase programs” since at least 2011.

Julian Rimmer 11:07Herstatt Risk? Plays left back for Dortmund?

ECB yesterday… holding borrowing costs at this level for long enough will make a “substantial contribution” to bringing consumer-price gains back to the 2% target.

Christine Lagarde said any discussion of when to cut interest rates is “totally premature.” As we wrote earlier on this week, I don’t think central banks really ever plan to get inflation back down to 2, something around 4% makes more sense in terms of inflating away the debt

but prepping the mkt for this is fraught with peril and misinterpretation and will be the most gradual and painstaking of policy shifts imaginable

Izabella Kaminska 11:09Though inflation only works at inflating away the debt if it’s “surprise inflation”. Or as Helmholtz said, negative real rates are set by policy, which is controversial in an inflationary environment.

That said the argument to lift the target is now becoming very compelling. And it’s not just Jason Furman arguing this anymore.

Mohammed El Erian made a similar point at his book launch a couple of weeks ago, but he also stressed cbankers would be very unkeen to go ahead with it out of fear it looked like a desperate move.

Though what Lagarde also said, which made me raise my eyebrows a lot, when responding to the FT’s Martin Arnold question about central bank losses at the Riksbank:

“As a Eurosystem and as ECB we have one mission which is price stability. We do not have as a purpose to show profits or to cover losses. It will be actually wrong if our decisions were guided by our P&L accounts rather than MP purposes.”

Which i found quite extraordinary. And goes towards all teh jedi mindtricks about how “cbanks are different”

No time for details on that, but check out the latest Blind Spot newsletter as to why i think she’s wrong. And why we are in the domain of quasi fiscal operations and that means greater not lesser coordination with the fiscal authority. As per above.

Julian Rimmer 11:10I note ‘The Bank of Japan has conducted yield-curve control on a routine basis’

which explians why the yen is where it is – ie through 150

Izabella Kaminska 11:11100%

Julian Rimmer 11:11something we’ve discussed in this parish a few times of late

one outcome of the blowout US GDP number was further dollar strength… with delightful consequences for the top third of Japan’s 30 biggest companies who now reap an extra $10bn in aggregate revs from yen weakness.

A lot of Japan’s biggest companies are exporters and making hay from yield curve control

or ycc

if i can mix my metaphors

The biggest beneficiary is Toyota, deriving Y45 billion of operating profit for every yen decrement against the dollar

Izabella Kaminska 11:12Wow. That’s quite a stat.

Is Toyota btw still the preferred vehicle for initiating militant insurgencies?

Julian Rimmer 11:14yes, it;’s also the preferred mode of transport for Taliban executioners when they drive off to the local sports stadium to decapitate or lapidate someone to death for adultery

Izabella Kaminska 11:14You can’t buy PR like that.

Julian Rimmer 11:14it would be a very interesting ad

would work on Kabul cable tv

something we’ve been discussing of late…

mead…

only jokingh

has been the relatively phlegmatic approach of global mkts to the execrescence of violence in the ME

i saw this superb piece by Clocktower group

Izabella Kaminska 11:17Who are clocktower?

Julian Rimmer 11:17an alternative asset management platform in public and private mkts

they explain very cogently why

While the Hamas terrorist attack is unprecedented in scale, it pales in comparison to the existential risk that Israel faced from the 1948 Arab-Israel War, the Six-Day War in 1967, and the 1973 Yom Kippur War. As such, the two macro legends running for the hills – Jones and Dalio – have fallen into the trap of trading off of headlines. We would remind both that Israelis and Palestinians have been fighting the same fight for centuries.’

(they’re not right about everything because israel hasn’t existed for centuries)

one thing Clocktower are very good at articulating is how financial markets are totally amoral

they remind investors that they are operating – now – in a multipolar geopolitical environment.

Julian Rimmer 11:20‘As predicted by political science theory and historical record, multipolarity is indeed a fertile ground for military conflict, but for investors, a higher threat environment is not synonymous with a bear market in risk assets. In fact, the two multipolar environments of the past two centuries led to both significant bull markets in risk assets and technological breakouts on an unparalleled scale’

and here is the salient line

geopolitical risk premium is the derivative of actual geopolitical risk.

What that means is that the stabilization of conflict, even if at a high rate of casualties and military conflict, causes geopolitical risk premium embedded in related assets to collapse. The market becomes desensitized to the conflict and moves on.

my emphasis

Izabella Kaminska 11:21WAR IS GOOD FOR THE STOCK MARKET

Julian Rimmer 11:22yes, that’s great publicity for the Blind Spot

advertisers will be flocking like swans to associate with that headline

Izabella Kaminska 11:23Though, have you seen all those videos of zoomers worrying about the draft being reinstituted and saying there’s no way in hell they can fight as they’re all overweight or on meds?

Julian Rimmer 11:23and the buzz cuts

Izabella Kaminska 11:23so i suspect that creates a market for the Terminator series

Julian Rimmer 11:24Clocktower’s view view is quite heretical. They believe that Israel is targeting north Gaza in order to show that it is doing “something.

Israel is reacting with domestic politics on its mind

Izabella Kaminska 11:25Second, Israel does not have sufficient intelligence on which to act against regional enemies, namely Hezbollah and Iran. In fact, the operation in Gaza is designed to be dramatic precisely so that Israel can avoid taking any action against anyone else. It satisfies the domestic political desire for revenge without putting Israel at risk of a wider conflagration. The bottom line here is that the logic of a ground incursion into Gaza is so severely lacking, other than from the PR/political perspective, that we could even see Israel chose not to undertake it, as a military spokesperson recently suggested.

Julian Rimmer 11:25Iran and Hezbollah are unlikely to escalate – both too frightened to do so owing to retaliation from US and IDF respectively

The reality here is that neither Iran nor Hezbollah really care about the fate of Palestinians. If they cared, they would have done something about the plight of Palestinians over the past seventy years

Hamas is hoping that Israeli brutality will lead to widespread protest against governments in the region that have largely ignored the situation in Palestine. While Hamas would love to see such protest in Gulf states and Saudi Arabia, that is highly unlikely to happen given strong government satisfaction in these countries.

Hezbollah and Iran are likely to retaliate directly in one way or another, although Clocktower expect their retaliations to be largely designed for popular consumption at home, not for effect (sort of like Tehran’s reaction to Soleimani’s assassination).

The question for investors, however, is whether any of these would change the balance of power in the Middle East. We suspect the answer is no, for the time being. As such, most geopolitical risk premium is to be faded.

boom in*

Izabella Kaminska 11:28That sounds super interesting, and i will have to properly give it a read.

I think we are nearly out of time.

Just to say, more on the importance of cbank losses in my newsletter this week. But also, don’t forget to come back on Monday at 1030 am. And do spread the word. these sessions are always best when they’re interactive. And don’t be frightened to push back with comments.

Next monday I’m at a weird conference all day in Greenwich called the ARC forum.

I might send some sneaky pics your way

Julian Rimmer 11:30another weird conference. they seem to proliferate in your life

Izabella Kaminska 11:30

Julian Rimmer 11:30As the doting mother of a 6yr-old, how is Halloween prep going?

Izabella Kaminska 11:31ah, very good! Trick or treating is big in my house.

Tho we live next door to some nuns, so i worry about upsetting them.

Julian Rimmer 11:31As the anti-Christ I’d be delighted to rub the nuns’ noses in it

so to speak

on that diabolistic note, bon weekend

Izabella Kaminska 11:31Bon weekend, and happy mushroom picking 🙂