Izabella Kaminska10:59

Izabella Kaminska10:59Morning!

Morning!

Welcome to nearly the end of the week. And so far no bank collapses. I believe Izzy is joining me today.

Izabella Kaminska11:01I am indeed here spiritually for 30 min and then consciously from 1130 onwards. Multitasking like a crazy person these days.

Should we check in on markets?

Green again:

And the attack on Deutsche seems to have been called off:

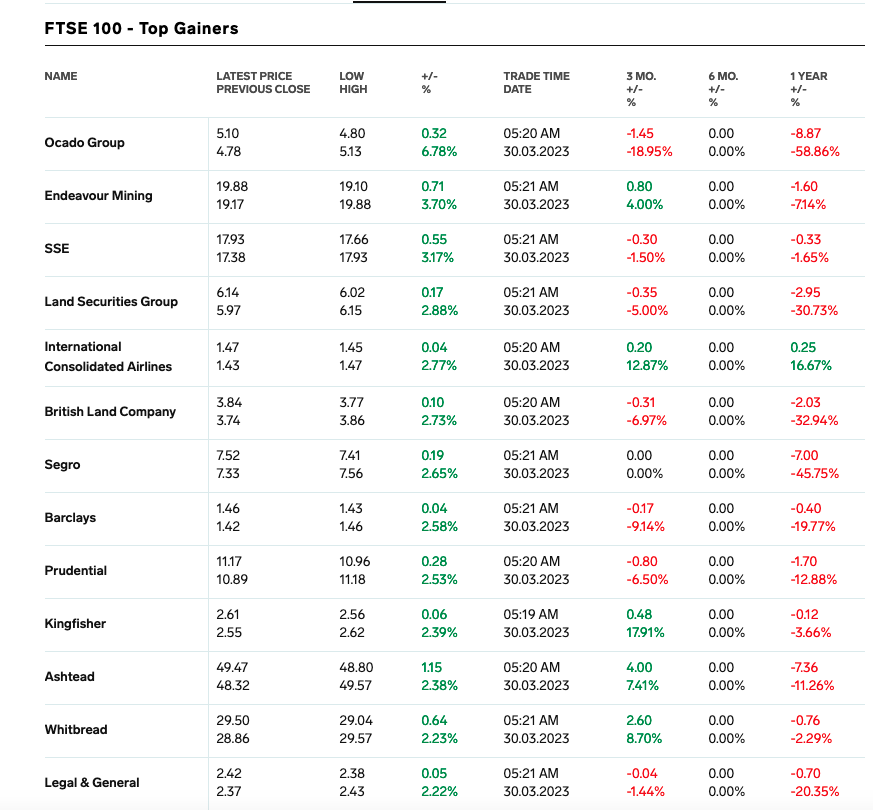

Ocado leading the gainers in London:

Interesting story for Ocado actually. Looks like a possible short squeeze following a crappy sales period.

The retailer’s shares soared during lockdown as consumers turned to online shopping, but now the bite back has begun:

However, last month, the online grocer reported sales fell 3.8% to £2.2bn in what it called a “challenging market” as the benefits of the trend towards online shopping sparked by the pandemic lockdowns wound down and shoppers flocked to discounters amid the rising cost of living.

Independent retail analyst Richard Hyman told This is Money: ‘If you look back before the pandemic then Ocado was often massively shorted – this is a return to form.

Some background:

But I’m going to give way to Frances now for a bit.

So, no more bank dramas as far as we know – yet.

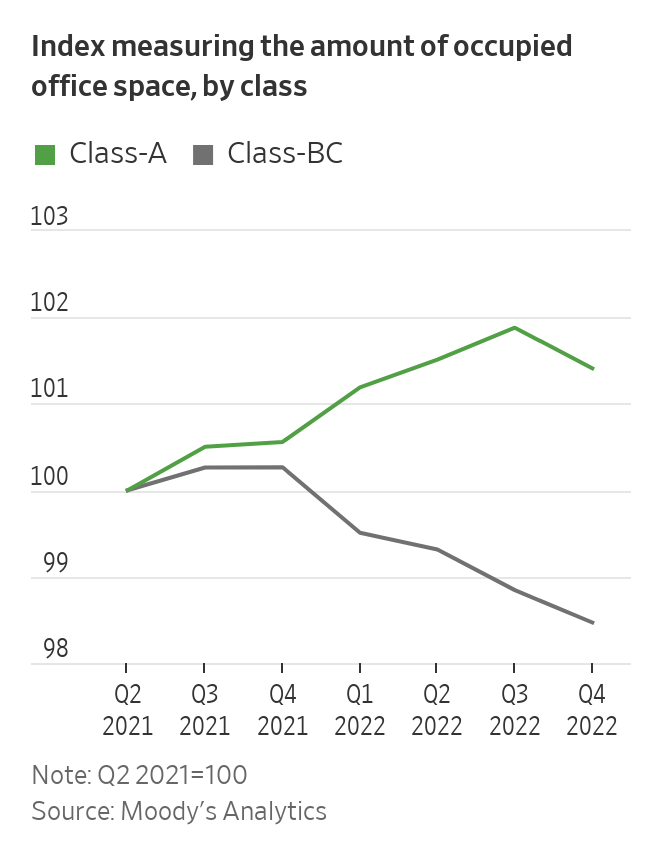

But Commercial Real Estate is waiting in the wings.

WSJ says falling CRE occupancy is now spreading to high-end buildings. Remote work and rising interest rates to blame. https://www.wsj.com/articles/distress-in-office-market-spreads-to-high-end-buildings-c1adad

“Analysts expect office defaults to increase as more mortgages that were signed before the pandemic expire. Around $2.6 trillion in commercial mortgages are set to mature between 2023 and 2027, according to Trepp Inc. Many of these loans are held by smaller banks.”

So we might not have seen the last of the US smaller banks crisis.

Interestingly, Signature Bank NY, which was closed down by regulators on 12th March, had a substantial CRE portfolio – according to Trepp, in 2021 it was the US’s 10th largest CRE lender. https://www.trepp.com/trepptalk/digging-into-new-york-commercial-real-estate-exposure-after-signature-bank-closure

Trepp says SBNY held a 12% share of the New York metro area CRE market. Flagstar has now acquired most of SBNY’s deposits, but it only bought $12.9bn of its loans – at a hefty discount of $2.7bn, which suggests these weren’t exactly of the highest quality. The remaining $60bn are still with FDIC for disposal or run-off. We’ve tended to assume that SBNY’s collateral insufficiency (the cause of its insolvency) was due to unrealised losses on government bonds, as with Signature and SVB, but perhaps it was actually due to impairment of its CRE portfolio?

There’s been lots of talk that SBNY was actually solvent and regulators closed it down because of its crypto business. But in fact it was hit by a massive bank run and couldn’t find the collateral for its discount window borrowing.

Would SBNY have been able to continue if it had opened on Monday? It seems unlikely. SBNY was already critically short of eligible collateral, and reopening on Monday would likely have reignited the bank run. A bank that has insufficient eligible collateral to tap the Fed’s discount window for funding to meet its obligations is insolvent, not merely illiquid. And I don’t mean insolvent in the sense that its assets are worth less than its liabilities, though that was probably also true. I mean that it is unable to meet its obligations as they fall due. That is the textbook definition of insolvency.

That’s from my piece on SBNY posted yesterday. https://www.coppolacomment.com/2023/03/what-really-happened-to-signature-bank.html

Anyway, FDIC has been left with a huge pile of (presumably) significantly impaired loans, the losses on which will eventually be charged to the banks that didn’t fail. There’s been some pushback from community banks on this – they don’t think they should have to pay.

Speaking of real estate, Poland’s financial regulator says the long-running legal dispute over Swiss franc-denominated mortgages could spill over into mortgages denominated in the local currency, zloty. https://www.bloomberg.com/news/articles/2023-03-30/polish-watchdog-warns-zloty-mortgages-may-be-next-flashpoint?

Izabella Kaminska

Ah the tale of swiss franc-denominated mortgages! I have to say I didn’t realise there was a zloty follow-through.

Here’s what Bloomberg says:

Poland’s financial regulator warned that the festering legal controversy over Swiss franc mortgages, which already forced local banks to set aside about 40 billion zloty ($9.3 billion) in provisions, may spillover into zloty-denominated home loans.

Speaking in an interview with PAP newswire, Jacek Jastrzebski said the litigation is creating “a widespread perception that you can find something in the contract that will be an excuse not to repay the loan or to pay it back without interest.”

“A whole legal infrastructure, firms were created and became, in a sense, factories to handle client lawsuits against the banks,” the head of the regulator known as KNF said. “This growing awareness is infecting” zloty mortgages.

To be honest there’s a much bigger issue for Poland, which is now facing extreme inflationary pressures.

Inflation there is in the high-double digits now. As Notes from Poland reported two weeks ago:

Annual inflation accelerated again to reach 18.4% in February, its highest level since 1996 though slightly below forecasts. While inflation has surged in Poland over the two years, economists believe that last month’s figure will mark a peak and that price growth will slow in the coming months.

The new figures from Statistics Poland (GUS), a state body, show that inflation in February surpassed the recent high of 17.9% recorded in October 2022. According to GUS’s data, the prices of food, transport and energy rose fastest in February.

Everyone is hoping it’s the peak, but there’s been some absolutely crazy stuff going on there.

Poland’s banks were ordered to institute mortgage holidays last year, for example. Banks like ING say they are coping, but I have my doubts. Here’s the latest via Reuters:

The Polish government has introduced so-called “credit vacations” to help borrowers deal with higher interest rates. The scheme allows mortgage owners to postpone up to eight loan payments in 2022 and 2023.

“We are analysing the loan portfolio very thoroughly and (…) at the moment there is no direct impact on costs of risks,” said Bozena Graczyk, referring to money banks set aside against risky loans.

![]() FRANCES COPPOLA

FRANCES COPPOLA

I think UK borrowers might be quite keen on mortgage holidays…)

Izabella Kaminska

I can’t see how this won’t obviously have an impact on inflation. And it’s also setting a precedent for negotiation. I feel in Poland, which let’s face is still relatively speaking a very YOUNG mortgage market, this all sets a bad precedent. And a lot of moral hazard.

Remember there were no mortgages during communism, and when communism collapsed there was initially a stigma in using financing to buy your house or flat. I remember my mum being very suspicious of all the people with mortgages. That stigma fell away in the mid noughties and as it did it saw the poles double down with not just mortgages but very exotic mortgages like Swiss franc denominated ones.

![]() FRANCES COPPOLA

FRANCES COPPOLA

I seem to recall Hungary going big on those too. If I recall correctly, they were eventually converted to forint.

@helmholz yes!

Izabella Kaminska

I think the Poles didn’t have the same concrete resolution. Either way, there is no institutional memory in the system of people having to face consequences from bad borrowing decisions.. By which i mean, i wouldn’t be surprised if the population as a whole turns out to be more interested in negotiating its way out of bad debts at any opportunity. T

![]() FRANCES COPPOLA

FRANCES COPPOLA

I think FX mortgages are always a bad idea and especially when there’s an exchange rate peg. In this case, rather than redenominating the mortgages, the Poles seem to be trying to find ways of not paying them. Though redenomination after an exchange rate peg fails is a form of default, really.

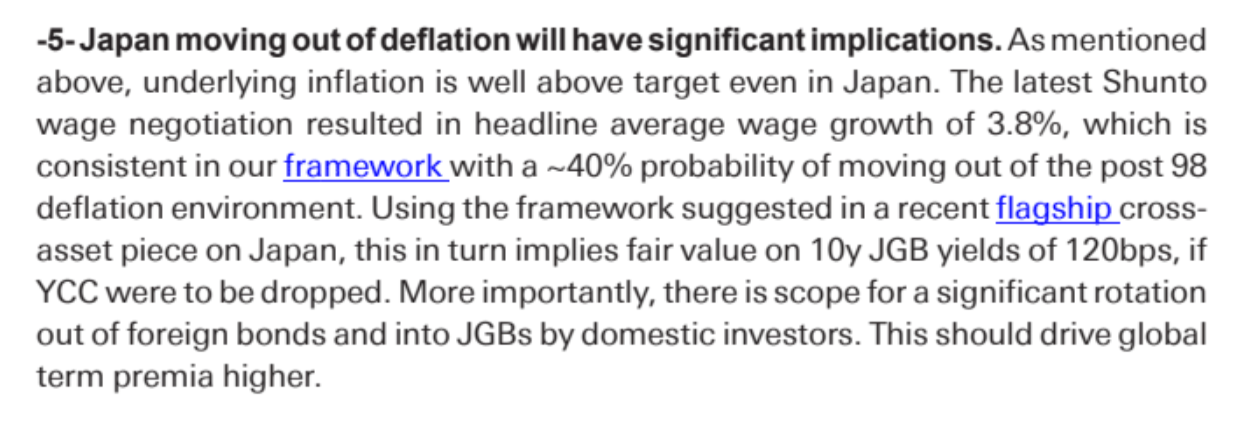

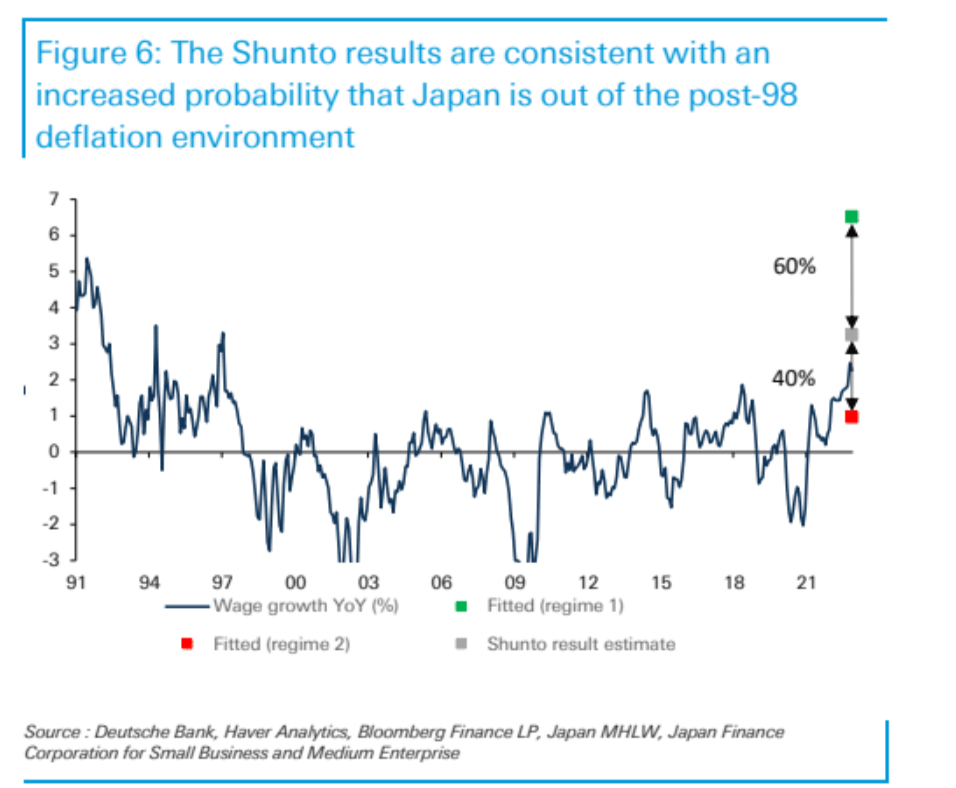

And on the subject of long-running real estate problems, a note from Deutsche Bank’s rates team predicts that Japan is emerging from the deflation that has plagued it since the real estate crash of the 1990s. They think this will be a game changer:

Charles Goodhart and Toby Nangle theorised a while ago that inflation would reappear in Japan as its ageing population retired and drew down their savings. But the Shunto results suggest that the return of inflation is driven more by wage demands among the working-age population.

Izabella Kaminska11:30That Japan paradigm shift could be a massive thing, especially if you consider the impact it might have on Yield Curve Control and the carry trade, which is still providing cheap funding to the Western world.

But finally on Poland, I just think broadly there is an assumption that Eastern European markets are now comparable to and as sophisticated as Western ones.

But i’m not convinced this is the right way to think about it. They haven’t really suffered a crisis yet. It’s all been on the up and up since joining the EU, and as I said before there is no recent memory of populations being left out of pocket because of their own bad decision-making.

There is still a communist legacy mindset that it’s the system’s fault I think. And the judiciary debacle is gonna obviously complicate things. You just need to look at the real-estate restitution cases from the soviet error. A hugely political mine field, and in many cases there is possibly a correct assumption that you can’t get a fair judgment on these things.

(Full disclosure, like most poles, my family also had a claim which got refused for ***Reasons***)

(According to my mother those reasons are a corrupt judiciary)

even in the UK people who lose court cases tend to blame the judiciary…

Izabella Kaminska11:36Exactly. But imagine the scenario when the government agrees with you.

Actually, one thing that is worth mentioning more broadly, is whether the legal situation is going to have a bigger role in market confidence moving forward.

Not just because of the AT1 debt fiasco, but I think with respect to asset confiscations etc.

And if it does, how this plays into the whole multipolarity situation.

11:38George Magnus has been saying that there is no threat to the dollar, and i am a huge fan of his (and his commitment to going to Glastonbury every year especially) but i think maybe his “blind spot” (pun intended) is the assumption that the other currencies will never ascend to our status.

11:39Perhaps the better way to think of it is that we descend to their status, and I see that happening in terms of the confidence in our rule of law waning a bit, but also in terms of capital controls.

We always hear nobody wants to use the yuan because it’s not freely floated, but surely we are on our way to undermining the free float of our own currencies as well?

What do you think?

I think Helmholtz’s point is on the money. Erosion of legal certainty as property rights are watered down in reserve currency issuing countries erodes confidence.

That’s why what Kathleen Tyson called “this outbreak of lawlessness” matters so much

Izabella Kaminska11:42exactly

if investors can’t trust Western rule of law, why would they trust Western assets and currencies?

Izabella Kaminska11:42Speaking of Swiss law i was directed to this today.

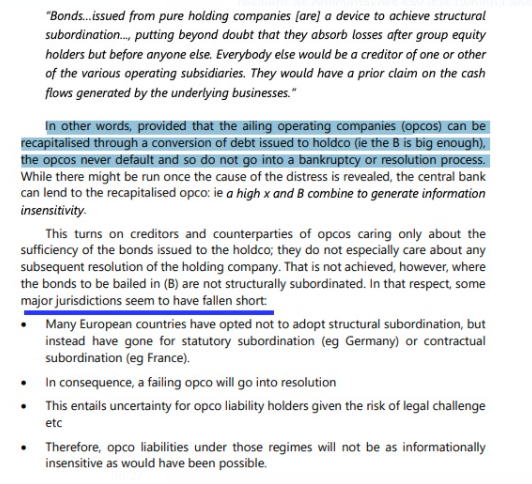

It’s an old Paul Tucker piece from 2019, and it’s interesting because of what he says about bank resolution

11:44it’s pretty prescient

“This essay amounts to a plea to policymakers to work with researchers to re-examine

whether enough has been done to make the financial system resilient.

We start from a position where the financial system is much more resilient than

before the crisis but, for the reasons I have set out, is less resilient than claimed by

policymakers. This is partly due to shifts in the macroeconomic environment. While

much post-crisis debate has centred on how best to protect the real economy from

financial system pathologies, regulatory policy now needs to respond to unexpected

constraints on monetary policy. Specifically, until and unless monetary (or fiscal)

frameworks are adapted to create more room for stabilization policy in a world of

subdued underlying growth, regulatory policymakers need to increase equity

requirements in order to deliver the degree of system resilience that was implicit in

the G20’s Basel 3 reforms.”

And then this bit

The essay gives that issue two twists. One is to ask whether the system is as

resilient as policymakers say it is (which I answer in the negative). The other is to

explore what it would mean to operationalize, within a Money-Credit Constitution,

recent theoretical discussions of “informationally insensitive” safe assets.2

But generally also see section 5

The problem with assuming that law confers certainty is that law is language, and language is open to interpretation. Hence lawyers. And courts.

Izabella Kaminska11:46Yep

Where i am going with the Tucker piece, which everyone should really read, is that he basically says that even 100% LCR is not enough.

Is it fair to call 100% LCR full-reserve banking? I think so, no?

No

LCR only reserves expected outflows, not 100% of deposits

Izabella Kaminska11:48ah, right.

But 100% is on its way right?

I don’t think full-reserve banking is the security blanket people think it is

Izabella Kaminska11:49Anyway what I thought was interesting in that piece is the idea that 100% LCR covering short-term liabilities is not enough. Tucker says the strength of a bank in such an environment is a function of how much over collateralisation it has vis-a-vis its LCR

If longer- term and so uncovered debt liabilities (L, B and R) were banned, the amount of

tangible common equity (tangible net worth) a bank had to carry would be equal to

the value of the excess collateral required by central banks plus the value of any assets

that were not eligible at the Window (UA). 27 In other words, central banks’ haircut

policy plus the value of a licence to hold ineligible assets would determine the level

of equity.

(as far as i understand)

Which kind of is the way Tether is operating organically no?

It’s shortening the duration of its liabilities, yes

this is what bank regulators need to look at – HQLA need to be T-Bills and reserves, not 10-year USTs!

Izabella Kaminska11:50Here’s the relevant bit:

“It is easy to fall into the trap of thinking that making x=100% renders insolvency

irrelevant. In fact, a policy of completely covering short-term labilities with central

bank-eligible assets would leave uninsured short-term liabilities safe only when a

bank was sound. They would not be safe when a bank was fundamentally unsound.

That is because central banks should not (and in many jurisdictions cannot

legally) lend to banks that have negative net assets (since LOLR assistance would

allow some short-term creditors to escape whole at the expense of equally ranked

longer-term creditors). This is the MCC’s financial-stability counterpart to the “no

monetary financing” precept for price stability.Since only insured-deposit liabilities, not covered but uninsured liabilities, are

then safe ex post, uninsured liability holders have incentives to run before the shutters

come down, making their claims information sensitive after all.More generally, the lower E, the more frequently banks will fail when the central

bank is, perforce, on the sidelines. This would appear to take us back, then, to the

regulation and supervision of capital adequacy, but in a way that helps to keep our

minds on delivering safety ex post and so information insensitivity ex ante.”

11:52Anyway, the point I guess is that for QE to be unwound, it seems very likely we have to compartmentalize short-term liabilities from longer-term ones in new ways that ensure full liquidity coverage. And I think, this is where CBDCs come in. Because they will end up compartmentalizing the central bank balance sheet in exactly this way. Ensuring that all short-term liabilities – ie. sums used for current accounts and day-to-day payments, become de facto fully covered CBDCs?

So in short I think CBDCs are part of the exit strategy from QE.

And the nationalisation of the payments system

Izabella Kaminska11:53Certainly, the coordination is now very hard to ignore.

This came out two days ago, for example:

TOKYO, March 28 (Reuters) – The Bank of Japan must be ready to issue central bank digital currencies (CBDC) that coexist with various other forms of money to offer the public a safe digital payment system, its governor Haruhiko Kuroda said on Tuesday.

The central bank will start a pilot programme in April to test the use of a digital yen, joining a growing number of countries seeking to catch up with front-runner China in launching a CBDC.

I think it makes total sense though. Because how else can you unwind QE in a controlled way?

And that’s where we enter into the return of capital controls, or rather FX controls.

Because one of the big concerns cbankers have is that if inflation continues to grip and confidence issues ensue with domestic currencies, that the likes of China might be able to flood our system with their e-yuan CBDCs.

To counter that we would have to revert to a type of digital FX control.

(@helmholz I’d argue that an institution whose liabilities are longer duration than its assets is not a bank)

Nationalisation of the payments system implies FX controls, I think

because no-one will want someone else’s CBDC competing with their own

Izabella Kaminska11:58So the concern really is when local Chinese businesses start accepting eyuan via wechat in their shops.

Because then the entire supply chain even in within the UK becomes funded via yuan. And if it doesn’t touch sterling/euro/dollar markets at all, then it can potentially skirt the taxman too.

Perhaps that’s the other fundamental concern with huawei?

How do you enforce FX controls on apps? You have to control the service provider presumably?

I don’t know enough about IT, but it seems reasonable to assume that a Chinese telecoms provider might be able to bypass such controls – or at least that would be the concern?

So ban Chinese telecoms. We’re already going there.

Izabella Kaminska12:00Ban them, but as a form of FX control. Not just as a form of spy control.

Both, really

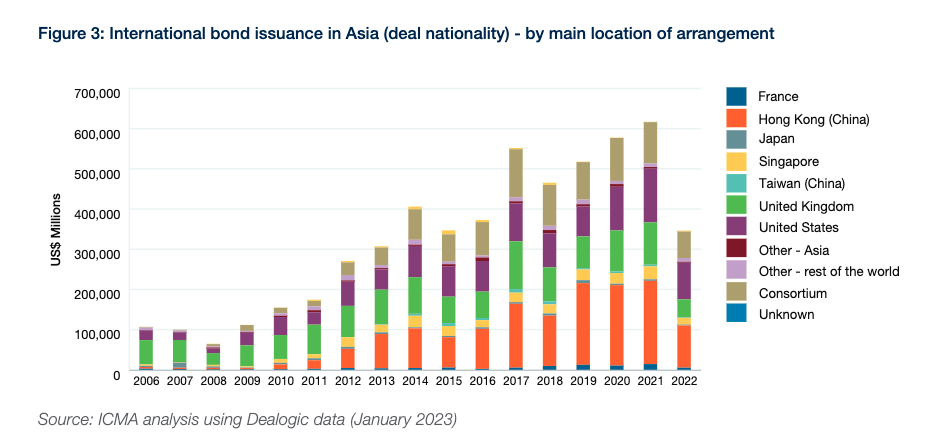

Izabella Kaminska12:01Other than that, it’s worth noting that the Asian bond market has not been flourishing

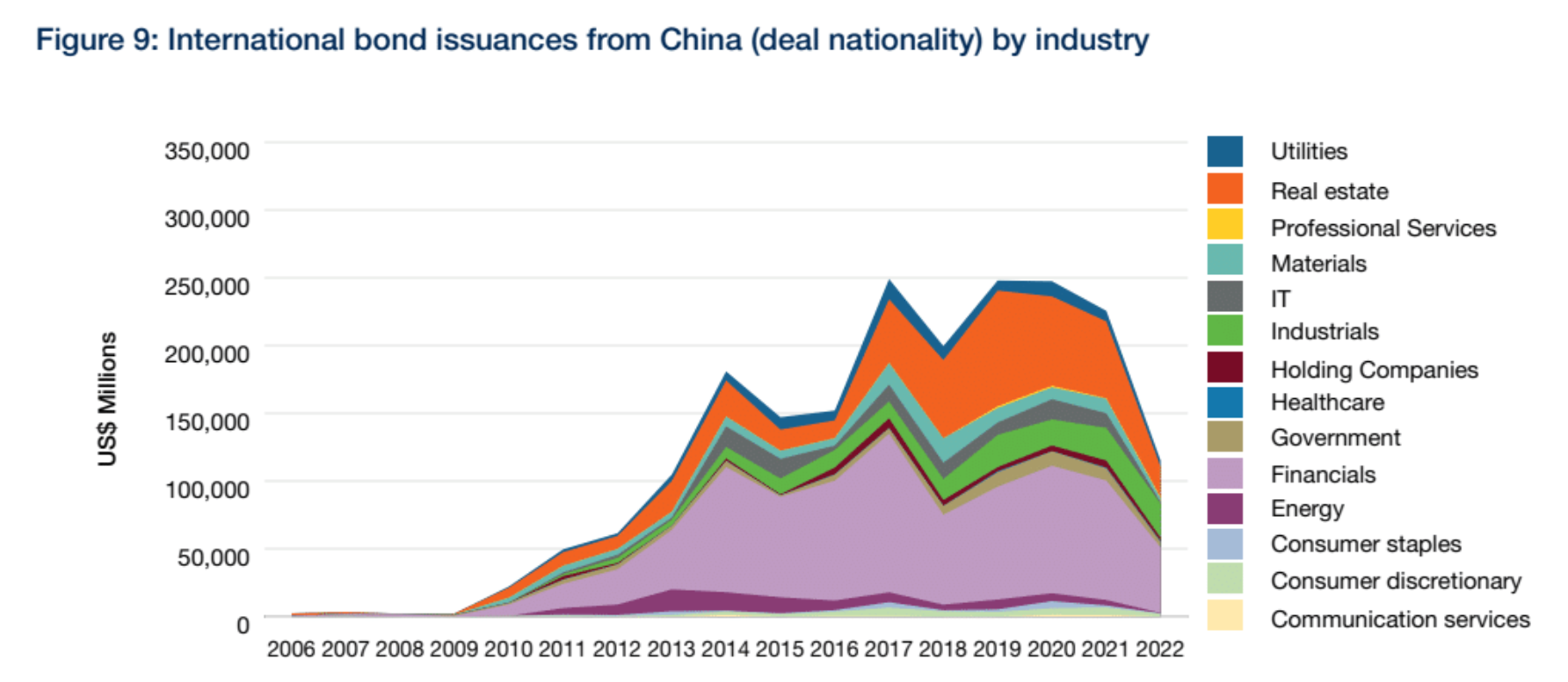

This is from the latest ICMA survey

47The Asian International Bond Markets: Development and Trends – March 2023

As with bond markets globally, 2022 was a challenging year for the Asian international bond market, with total issuances

44% lower compared with 2021. This was mainly due to uncertainty being caused by rising interest rates and geopolitical

conflicts, but also the impact of significant credit events in the Chinese real estate sector. In 2022, issuance from Chinese

issuers declined by 49% year-on-year, although this remained the largest source of Asian international issuance by deal

nationality (33%). Other trends, prompted by higher rates, include a move from G3 issuance into other sources of finance,

including domestic bond issuance and bank loans, as well as a shortening of tenors. With respect to listing location,

Luxembourg has gained a string foothold, although Singapore and Hong Kong remain the centre of choice

The charts are quite striking actually

Wonder what the rabble think about that?

Funny how it always seems to come back to real estate and financials.

Izabella Kaminska12:02And hong Kong seems to have been utterly choked off.

But is it a demand thing, or a supply thing?

The fall in real estate issuance could be due to the dead weight of Evergrande’s debt problems

12:04Evergrande announced a debt restructuring a week ago, but it wasn’t well received by markets. There are still big questions over whether the firm will survive and what the ramifications for the Chinese real estate market and for its banks would be.

FT has a good piece on this. https://www.ft.com/content/9e8b0e71-dc12-4c07-b1f0-a203f32d9166

Izabella Kaminska12:04Also this was quite interesting in the report:

One of the factors contributing to this significant growth is the increasing overseas operational and financial activities

of Chinese entities. Raising funds in USD or Euro offshore to meet their acquisition or expansion plans was especially

advantageous from 2010 to 2014 with continued appreciation of RMB and low interest rates in USD funding markets.

Interest rate hikes introduced by the Fed and the devaluation of RMB in 2015-2016, as well as the filing requirement

introduced in 20159 for all offshore issuances longer than one-year, led to a temporary decline in fund raising activities

of Chinese entities offshore. The upward trend in issuance resumed in 2016. In 2018, the National Development and

Reform Commission introduced stricter standards to manage the scale of foreign debt financings by onshore enterprises.

These new stipulations, aimed at reducing levels of corporate and institutional leverage, contributed to the decline of new

issuances from China in 2018.

For some Chinese issuers, going into the offshore market is a means to diversify their financing structure by providing

an additional funding channel. The international bonds do not replace but rather supplement their existing bank loan or

onshore capital raising.10 Issuers compare the cost of offshore funding after hedging with the market yield onshore, as

well as considering where the funds raised will be used. Some interviewees pointed out that the offshore market allowed

cheaper funding for IG issuers after hedging in 2020, but the case was reversed in 2021. As a result, more high-rated

issuers turned to onshore issuances, contributing to the decline in the international bond issuance volume by Chinese

issuers

Interesting no?

On that note, we are way past the hour.

So thank you for joining us again.

We will be back with Monday-only sessions from now (but not on Easter Monday!) — at least until the markets fall apart again.

Let me know how the daily sessions went. Are they worth it?

Might happen sooner than we think. Repo rates are wild. But I’m going away next week, so I’d rather things didn’t fall apart for a week or two.

Happy Easter, everyone.

Izabella Kaminska12:06We did have some repo charts but we have run out of time!

Happy Easter

and happy Smingus Dyngus (which is my favourite holiday)